Dried Peas Market Outlook 2026–2034: Plant-Based Protein Demand, Pulse Processing Growth, Leading Companies, and Future Opportunities

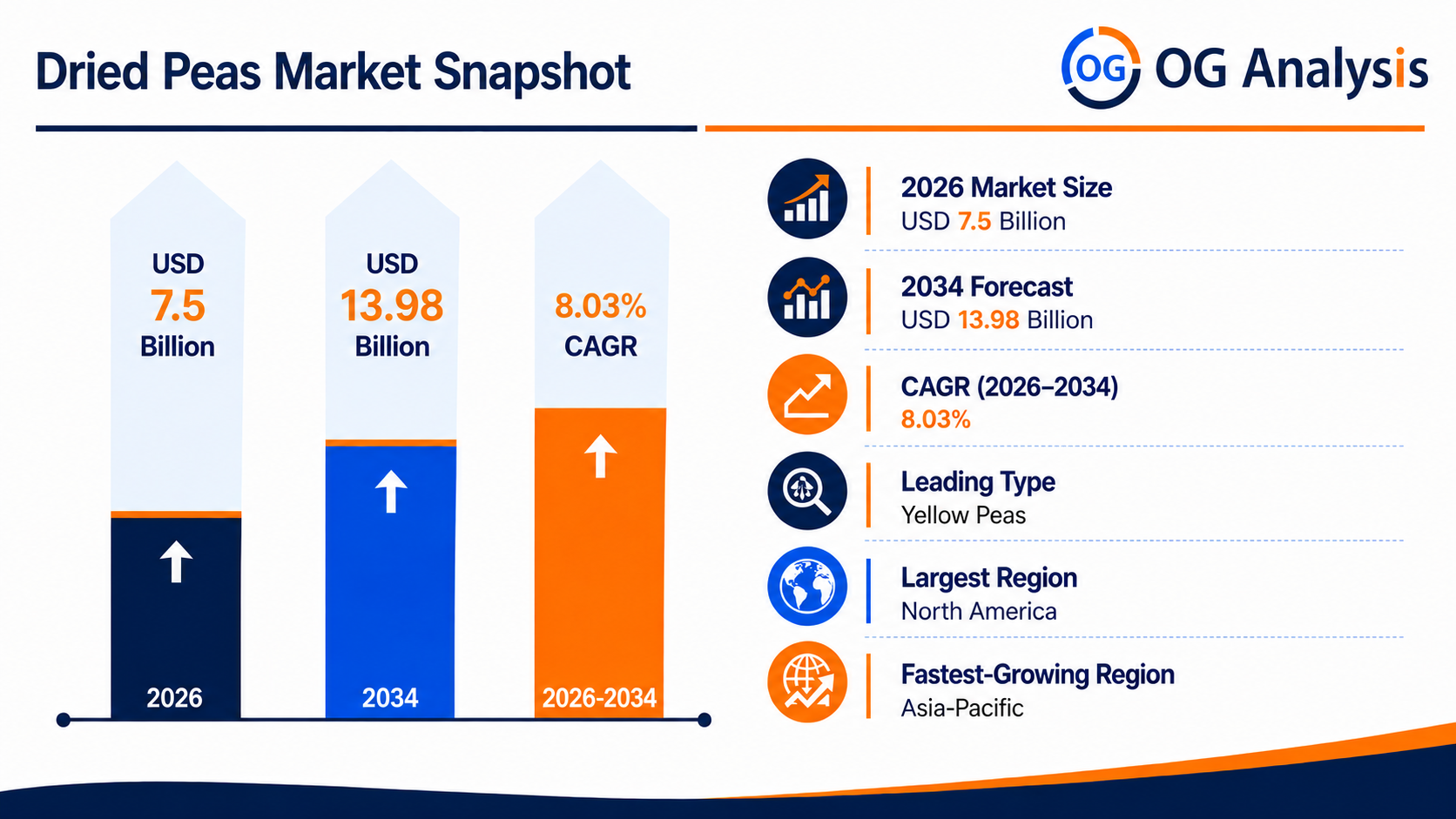

The Dried Peas Market was valued at $ 7.5 billion in 2026 and is projected to reach $ 13.98 billion by 2034, growing at a CAGR of 8.03%.

Dried peas include whole dried peas, split peas, yellow peas, green peas, pea flour, pea protein inputs, and food-grade or feed-grade dried pea products used across food processing, retail pulses, animal feed, plant-based foods, soups, snacks, bakery, ready meals, and protein ingredients. Demand is increasing as consumers seek affordable protein, high-fiber foods, plant-based nutrition, clean-label ingredients, and sustainable food sources. Market growth is also supported by pea protein manufacturing, pulse-based snacks, gluten-free formulations, vegan diets, and rising use of dried peas in both human food and livestock feed applications.

Get Your Free Sample Report for In-Depth Market Insights :

https://www.oganalysis.com/industry-reports/dried-peas-market/free-sample

1. What is the latest trend in the Dried Peas Market?

The latest trend is the rising use of dried peas in plant-based protein, pulse flour, snacks, soups, and clean-label food formulations.

Yellow peas are gaining strong demand because they are widely used for pea protein concentrates, isolates, starch, and fiber ingredients.

Food companies are using dried peas in vegan foods, meat alternatives, protein bars, bakery products, noodles, and ready meals.

Consumers are also shifting toward affordable, shelf-stable, high-protein, and high-fiber pantry foods.

2. What are the key challenges in the Dried Peas Market?

Key challenges include crop yield variation, weather dependency, price volatility, export restrictions, and quality differences across origins.

Processors must manage moisture content, splitting quality, protein levels, pesticide residues, storage stability, and contamination risks.

Supply chains can be affected by freight costs, trade policy, currency movements, and changing import demand from major buyers.

Competition from lentils, chickpeas, soy, fava beans, and other plant protein crops can also pressure market growth.

3. What is the major driving factor for the Dried Peas Market?

The major driving factor is increasing demand for plant-based protein, affordable nutrition, and sustainable food ingredients.

Dried peas are rich in protein and fiber, making them attractive for both traditional diets and modern food formulations.

The growth of pea protein processing is creating additional demand for high-quality yellow peas.

Rising consumer interest in healthy, clean-label, vegan, and gluten-free food products is further supporting market expansion.

4. What is the major segment in the Dried Peas Market and why?

Yellow dried peas represent a major segment because they are widely used in food processing, pea protein extraction, starch production, and animal feed.

They offer strong functional value for protein isolates, concentrates, flours, textured proteins, and extruded products.

Split peas are also an important segment because they are widely consumed in soups, dals, stews, packaged pulses, and institutional foodservice.

Food-grade dried peas generate strong value where quality, color, purity, and protein content are critical.

5. Which application or end-user is driving more demand?

Food processing and plant-based ingredient manufacturers are driving strong demand for dried peas.

Pea protein producers use dried peas to manufacture protein concentrates and isolates for meat alternatives, dairy alternatives, sports nutrition, and bakery products.

Retail consumers and foodservice operators continue to support demand for split peas, whole peas, soups, snacks, and traditional pulse-based meals.

Animal feed and pet food manufacturers also use dried peas as a protein, starch, and fiber source.

6. Which region offers the highest growth potential and why?

Asia Pacific offers strong growth potential due to rising demand for affordable protein, traditional pulse consumption, processed foods, and pea protein ingredients.

China is an important buyer of imported peas for food processing and pea protein production.

India, Southeast Asia, and other Asian markets support demand through pulse-based diets, snacks, and foodservice consumption.

North America and Europe remain important due to pea production, plant-based food innovation, and ingredient processing capacity.

7. What strategies are major companies adopting in the market?

Major companies are investing in pea protein processing, cleaning and splitting facilities, traceable sourcing, and value-added pulse ingredients.

Suppliers are focusing on protein-rich varieties, food-grade quality, residue compliance, storage efficiency, and export reliability.

Ingredient companies are developing pea flour, pea protein, pea starch, and pea fiber for clean-label and plant-based food applications.

Traders and processors are also diversifying sourcing across Canada, Russia, the United States, Europe, and Asia to reduce supply risk.

8. What are the leading companies in the Dried Peas Market?

Leading companies include AGT Food and Ingredients, Roquette Frères, Ingredion, Cargill, Archer Daniels Midland Company, Bunge, Louis Dreyfus Company, Viterra, The Scoular Company, Emsland Group, Vestkorn Milling, Parrish & Heimbecker, Columbia Grain International, Anchor Ingredients, and Dakota Dry Bean.

These companies compete through sourcing networks, processing capacity, ingredient innovation, export capabilities, and food-grade quality assurance.

Large ingredient companies are strong in pea protein, starch, fiber, and flour applications.

Pulse processors and grain traders remain important in cleaning, splitting, packaging, and global distribution.

9. Why are dried peas strategically important for food and ingredient manufacturers?

Dried peas are strategically important because they provide a scalable, affordable, and sustainable source of plant-based protein and fiber.

They support both traditional pulse consumption and modern food innovation in plant-based meat, snacks, bakery, and nutrition products.

For ingredient manufacturers, dried peas provide multiple revenue streams through protein, starch, fiber, and flour extraction.

For food brands, they support clean-label, vegan, gluten-free, high-protein, and high-fiber product positioning.

10. What is the future outlook for the Dried Peas Market?

The future outlook remains positive as demand rises for plant-based protein, pulse-based foods, affordable nutrition, and sustainable crops.

Growth will be supported by pea protein manufacturing, convenience foods, snacks, soups, pet food, animal feed, and retail pulse consumption.

Supply-chain resilience, quality control, crop productivity, and trade access will remain key success factors.

Companies offering reliable sourcing, high-protein varieties, value-added processing, and clean-label ingredient solutions are expected to gain market share.

Browse Related Reports

https://www.oganalysis.com/industry-reports/faba-beans-market

https://www.oganalysis.com/industry-reports/soybean-derivatives-market

https://www.oganalysis.com/industry-reports/plantbased-feed-enzyme-market

https://www.oganalysis.com/industry-reports/customized-premixes-market

https://www.oganalysis.com/industry-reports/cold-water-swelling-starch-market

Stay Connected With Us