Non-Residential Accommodation Market Outlook 2026–2034: Flexible Stay Demand, Digital Booking Growth, Leading Companies, and Future Opportunities

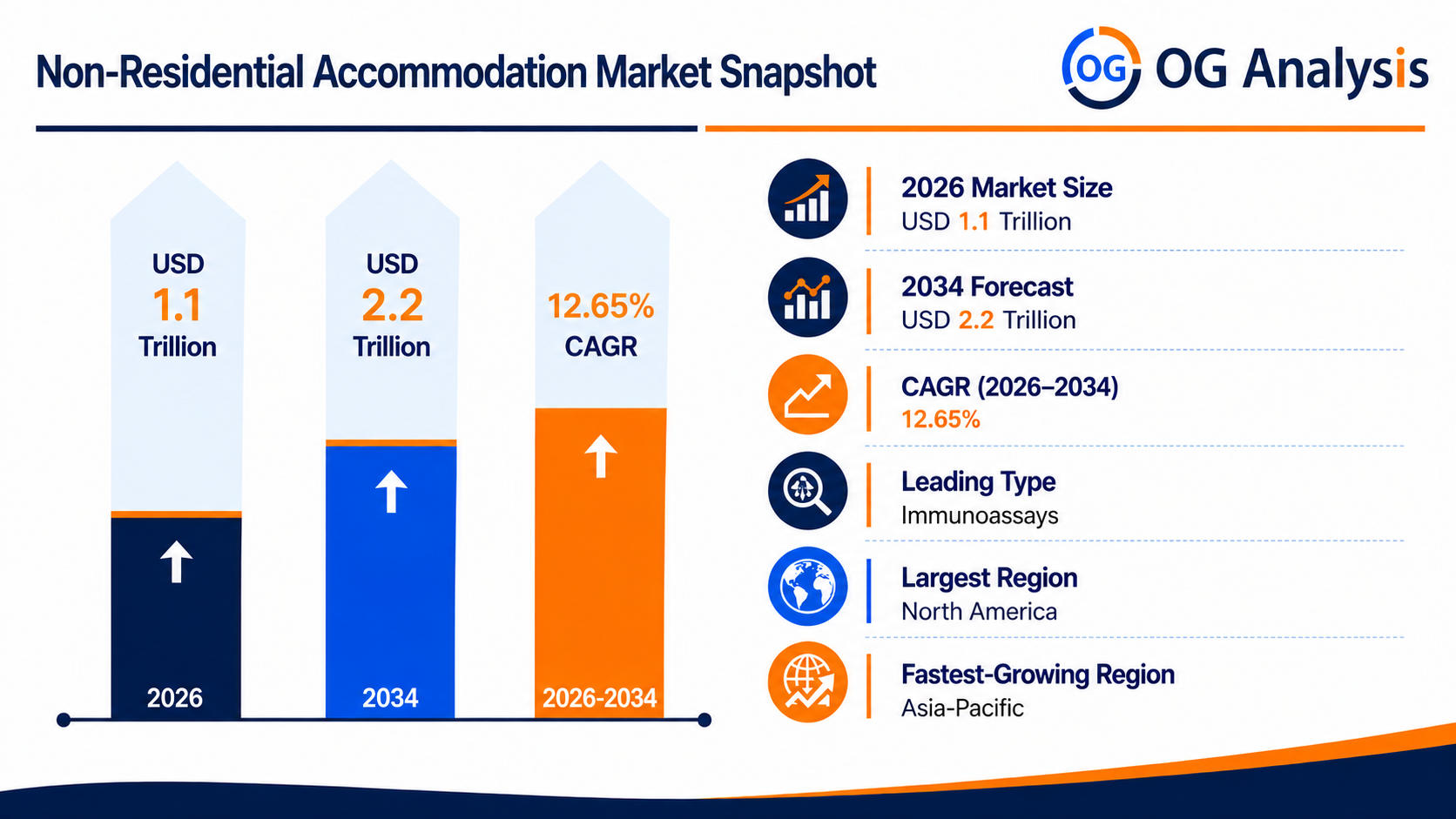

The Non-Residential Accommodation Market was valued at $ 1.1 trillion in 2026 and is projected to reach $ 2.2 trillion by 2034, growing at a CAGR of 12.65%.

Non-residential accommodation includes hotels, motels, resorts, serviced apartments, hostels, guest houses, vacation rentals, corporate housing, extended-stay accommodation, and short-term rental properties used by leisure travelers, business travelers, students, workers, tourists, and relocating professionals. Market growth is supported by rising domestic and international travel, recovery in corporate travel, digital booking platforms, flexible work trends, urban tourism, events, hospitality investment, and demand for affordable and premium stay options. Operators are focusing on digital check-in, dynamic pricing, loyalty programs, branded residences, serviced apartments, sustainability, safety, and experience-led hospitality to improve occupancy, revenue per available room, and guest retention.

Get Your Free Sample Report for In-Depth Market Insights :

https://www.oganalysis.com/industry-reports/nonresidential-accommodation-market/free-sample

1. What is the latest trend in the Non-Residential Accommodation Market?

The latest trend is the growth of flexible, experience-led, and digitally managed accommodation formats.

Travelers are increasingly choosing serviced apartments, extended-stay hotels, vacation rentals, boutique hotels, and hybrid work-friendly stays.

Online booking platforms, mobile check-in, AI-based pricing, and personalized guest experiences are reshaping operations.

Sustainability, wellness-focused stays, local experiences, and long-stay packages are also becoming important market trends.

2. What are the key challenges in the Non-Residential Accommodation Market?

Key challenges include high operating costs, labor shortages, property maintenance expenses, seasonal demand variation, and intense price competition.

Operators must manage occupancy fluctuations, energy costs, food and service costs, regulatory compliance, and safety standards.

Short-term rental regulations, taxation rules, zoning limits, and local community concerns can affect growth in major cities.

Economic uncertainty, geopolitical disruption, and changing travel budgets may also influence booking patterns.

3. What is the major driving factor for the Non-Residential Accommodation Market?

The major driving factor is the expansion of leisure travel, business travel, domestic tourism, and flexible stay demand.

Rising disposable income, urbanization, meetings and events, digital travel booking, and improved transport connectivity are increasing accommodation demand.

Remote work and “bleisure” travel are encouraging longer stays and alternative lodging formats.

Hospitality brands are also expanding across budget, midscale, premium, and extended-stay categories to capture wider customer segments.

4. What is the major segment in the Non-Residential Accommodation Market and why?

Hotels and serviced accommodation represent major segments because they serve both leisure and business travelers across price categories.

Hotels benefit from brand trust, standardized service, loyalty programs, event facilities, and strong distribution networks.

Serviced apartments and extended-stay properties are growing quickly because they combine hotel services with residential comfort.

Vacation rentals and short-term rentals are also expanding due to demand for flexible, private, and family-oriented stays.

5. Which application or end-user is driving more demand?

Leisure travelers, business travelers, corporate clients, event participants, tourists, relocating employees, and long-stay guests are driving demand.

Leisure travel supports hotels, resorts, vacation rentals, hostels, and boutique accommodation.

Corporate travel, meetings, project assignments, and employee relocation support demand for hotels, serviced apartments, and corporate housing.

Students, healthcare travelers, digital nomads, and temporary workers are also increasing demand for flexible accommodation formats.

6. Which region offers the highest growth potential and why?

Asia Pacific offers strong growth potential due to rising tourism, expanding middle-class travel, urbanization, and hospitality infrastructure development.

China, India, Japan, South Korea, Southeast Asia, and Australia are important demand centers for hotels, serviced apartments, and short-stay rentals.

North America remains a leading market because of business travel, domestic tourism, branded hotel chains, and strong online booking penetration.

Europe also remains significant due to international tourism, heritage destinations, city breaks, events, and serviced apartment adoption.

7. What strategies are major companies adopting in the market?

Major companies are expanding brand portfolios across luxury, premium, midscale, economy, lifestyle, and extended-stay formats.

Operators are investing in digital booking systems, loyalty programs, revenue management, mobile check-in, and guest data analytics.

Hotel groups are using asset-light franchise and management models to scale faster across regions.

Sustainability programs, energy efficiency, local experiences, wellness amenities, and flexible cancellation policies are also key strategies.

8. What are the leading companies in the Non-Residential Accommodation Market?

Leading companies include Marriott International, Hilton Worldwide, Hyatt Hotels Corporation, Accor, InterContinental Hotels Group, Wyndham Hotels & Resorts, Choice Hotels International, BWH Hotel Group, Radisson Hotel Group, Minor Hotels, Airbnb, Booking Holdings, Expedia Group, Sonder, The Ascott Limited, and Extended Stay America.

These companies compete through brand reach, room inventory, digital distribution, loyalty programs, pricing strategy, customer experience, and property partnerships.

Global hotel chains benefit from strong franchise networks and corporate customer relationships.

Online platforms and short-stay operators compete through convenience, inventory variety, flexible booking, and localized accommodation options.

9. Why is non-residential accommodation strategically important?

Non-residential accommodation is strategically important because it supports tourism, business mobility, events, trade, education, healthcare travel, and urban economic activity.

Hotels, serviced apartments, and short-term rentals create demand for food services, transport, retail, entertainment, and local employment.

For investors, accommodation assets provide exposure to travel recovery, urban growth, and hospitality consumption.

For operators, diversified formats help serve different customer budgets, stay durations, and travel purposes.

10. What is the future outlook for the Non-Residential Accommodation Market?

The market outlook remains positive as global travel, business mobility, digital booking, and flexible stay demand continue to expand.

Future growth will be shaped by serviced apartments, extended-stay hotels, branded residences, short-term rentals, and technology-enabled hospitality.

Operators that combine strong location strategy, digital distribution, dynamic pricing, sustainability, and guest experience will be better positioned.

Companies offering flexible, safe, affordable, and experience-rich accommodation options are expected to gain market share.

Browse Related Reports

https://www.oganalysis.com/industry-reports/marinas-market

https://www.oganalysis.com/industry-reports/casino-management-system-market

https://www.oganalysis.com/industry-reports/expense-management-software-market

https://www.oganalysis.com/industry-reports/exterior-insulation-finish-system-market

https://www.oganalysis.com/industry-reports/pa-fire-alarm-system-market

Stay Connected With Us