Paper-based Copper Clad Laminate Market Outlook 2026–2034: Cost-Efficient PCB Materials, Electronics Demand, Growth Drivers, Leading Companies, and Future Opportunities

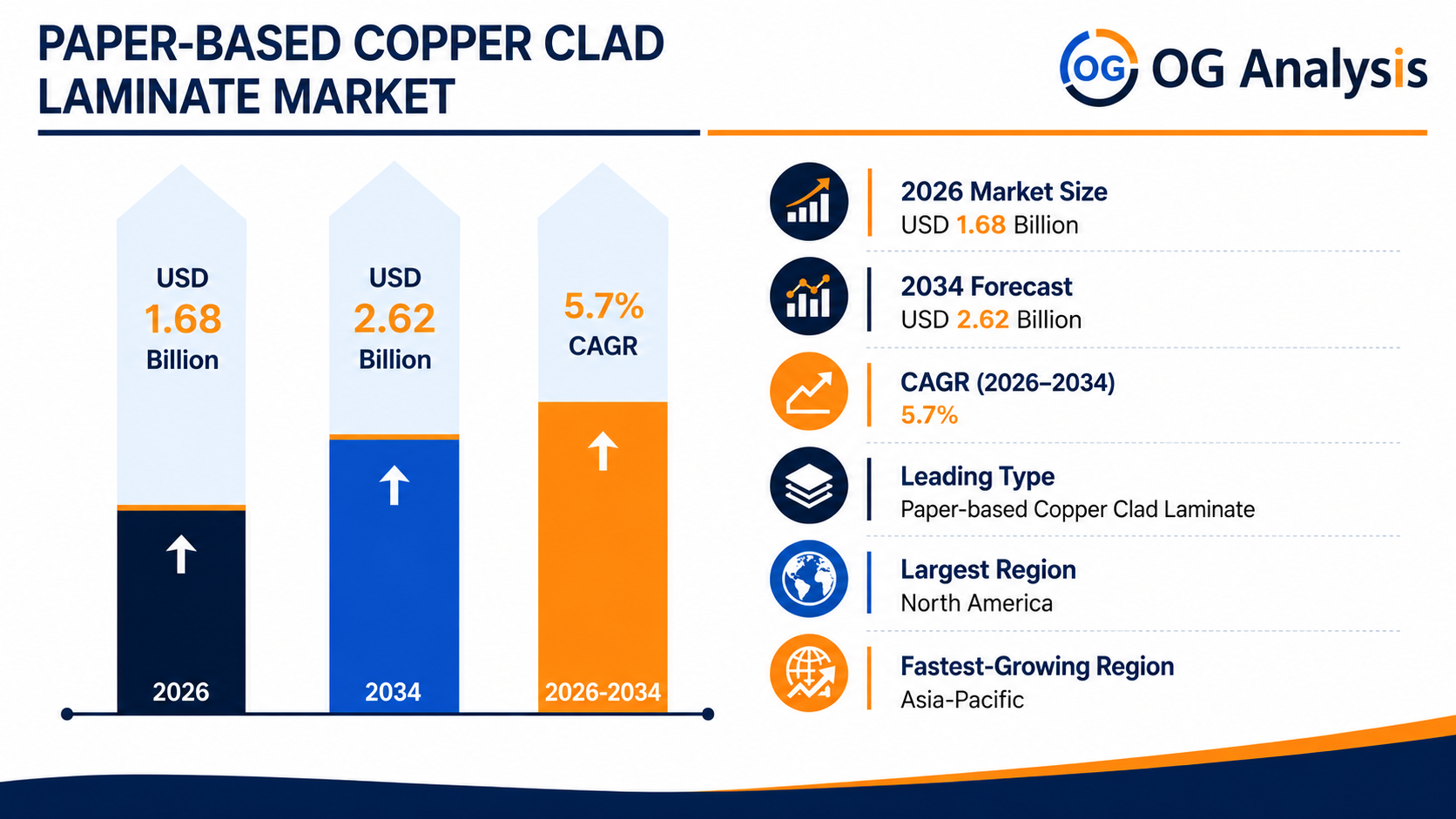

The Paper-based Copper Clad Laminate Market is valued at $ 1.68 billion in 2026 and is projected to grow at a CAGR of 5.7% to reach $ 2.62 billion by 2034.

Paper-based copper clad laminate is a PCB base material made using paper reinforcement impregnated with resin and bonded with copper foil on one or both sides. It is widely used in cost-sensitive printed circuit boards where mechanical strength, insulation performance, punching properties, and reliable copper adhesion are required. Major applications include consumer electronics, home appliances, LED lighting, power supplies, chargers, toys, remote controls, audio equipment, industrial controls, and low-frequency electronic assemblies. Market growth is supported by steady PCB demand, electronics miniaturization, appliance production, LED adoption, and demand for economical laminate materials. Manufacturers are focusing on better dimensional stability, flame resistance, punching performance, thermal reliability, copper peel strength, and stable quality for high-volume PCB fabrication.

Get Your Free Sample Report for In-Depth Market Insights :

https://www.oganalysis.com/industry-reports/paperbased-copper-clad-laminate-market/free-sample

1. What is the latest trend in the Paper-based Copper Clad Laminate Market?

The latest trend is the development of improved paper phenolic laminates with better flame resistance, punching quality, and dimensional stability.

PCB manufacturers are demanding materials that reduce cracking, warping, delamination, and processing defects during high-volume fabrication.

Cost-efficient grades for LED lighting, home appliances, and basic consumer electronics continue to gain attention.

Suppliers are also improving resin systems and copper foil bonding to support consistent PCB performance.

2. What are the key challenges in the Paper-based Copper Clad Laminate Market?

Key challenges include competition from FR-4, composite laminates, flexible substrates, and higher-performance PCB materials.

Paper-based CCL is generally preferred for low-cost and low-frequency applications, limiting its use in advanced electronics.

Raw material price volatility in copper foil, resin, kraft paper, and energy can pressure producer margins.

Manufacturers must also meet stricter flame-retardant, environmental, quality, and reliability requirements from electronics customers.

3. What is the major driving factor for the Paper-based Copper Clad Laminate Market?

The major driving factor is steady demand for low-cost PCB substrates in consumer electronics and electrical appliances.

Paper-based CCL offers an economical solution for simple circuits that do not require advanced high-frequency or high-temperature performance.

Growth in LED lighting, small appliances, chargers, audio devices, and basic control boards supports continued consumption.

Electronics manufacturers value its processability, punching performance, insulation capability, and cost advantage.

4. What is the major segment in the Paper-based Copper Clad Laminate Market and why?

Paper phenolic copper clad laminate represents a major segment because it combines low cost, electrical insulation, and good punching properties.

It is widely used in single-sided printed circuit boards for household appliances, lighting, power supplies, and simple electronics.

The material is attractive where high-volume production and cost control are more important than advanced signal performance.

Paper epoxy grades also serve selected applications requiring improved strength and electrical performance.

5. Which application or end-user is driving more demand?

Consumer electronics and home appliances are driving strong demand due to their large requirement for economical PCB materials.

LED lighting, chargers, fans, washing machines, kitchen appliances, remote controls, and audio products use simple PCB assemblies.

Industrial control devices and power supply boards also create stable demand for paper-based laminates.

PCB fabricators serving cost-sensitive electronics manufacturers are the key purchasing group.

6. Which region offers the highest growth potential and why?

Asia Pacific offers the highest growth potential due to its large electronics manufacturing base, PCB production capacity, and appliance output.

China, Taiwan, South Korea, Japan, India, and Southeast Asia are important demand centers for laminate and PCB materials.

The region benefits from integrated copper foil, resin, laminate, PCB, and electronics assembly supply chains.

North America and Europe remain important for specialized applications, replacement demand, and quality-driven electronics production.

7. What strategies are major companies adopting in the market?

Major companies are focusing on cost optimization, stable supply, product consistency, and application-specific laminate grades.

Suppliers are improving flame retardancy, dimensional stability, copper adhesion, punching performance, and heat resistance.

Companies are also strengthening relationships with PCB fabricators, appliance manufacturers, and electronics assemblers.

Regional capacity expansion, quality certification, and raw material sourcing control are important competitive strategies.

8. What are the leading companies in the Paper-based Copper Clad Laminate Market?

Leading companies include Kingboard Laminates, Shengyi Technology, Nan Ya Plastics, Panasonic, Taiwan Union Technology, Chang Chun Group, Eternal Materials, Sumitomo Bakelite, RISHO KOGYO, Isola Group, ITEQ, Ventec International, Doosan, GDM International Technology, and Guangdong Goworld Lamination Plant.

These companies compete through product quality, laminate performance, production scale, cost efficiency, copper foil sourcing, and PCB customer relationships.

Asian suppliers hold strong positions because of proximity to electronics and PCB manufacturing hubs.

Specialized suppliers compete through reliable paper phenolic grades, technical support, and custom laminate solutions.

9. Why is paper-based copper clad laminate strategically important for PCB manufacturers?

Paper-based copper clad laminate is strategically important because it provides a cost-effective base material for high-volume, simple PCB production.

It helps PCB manufacturers serve price-sensitive electronics where advanced laminate performance is not required.

Good punching properties, insulation performance, and copper adhesion support efficient board fabrication.

For appliance and consumer electronics manufacturers, it helps control material cost while maintaining acceptable electrical reliability.

10. What is the future outlook for the Paper-based Copper Clad Laminate Market?

The market outlook remains stable and positive as demand continues from low-cost electronics, appliances, LED lighting, and power supply applications.

Future growth will depend on cost competitiveness, improved material reliability, environmental compliance, and stable copper foil supply.

Paper-based CCL will remain important in applications where affordability and processability outweigh advanced performance needs.

Companies offering consistent quality, reliable delivery, and optimized grades for high-volume PCB production are expected to gain market share.

Browse Related Reports

https://www.oganalysis.com/industry-reports/conformal-coatings-market

https://www.oganalysis.com/industry-reports/semiconductor-gases-market

https://www.oganalysis.com/industry-reports/uv-cut-tape-market

https://www.oganalysis.com/industry-reports/unpatterned-wafer-defect-inspection-system-market

https://www.oganalysis.com/industry-reports/outdoor-led-lighting-market