Ultra-Thin Glass Market Outlook 2026–2034: Foldable Displays, Advanced Electronics, Leading Companies, and Growth Opportunities

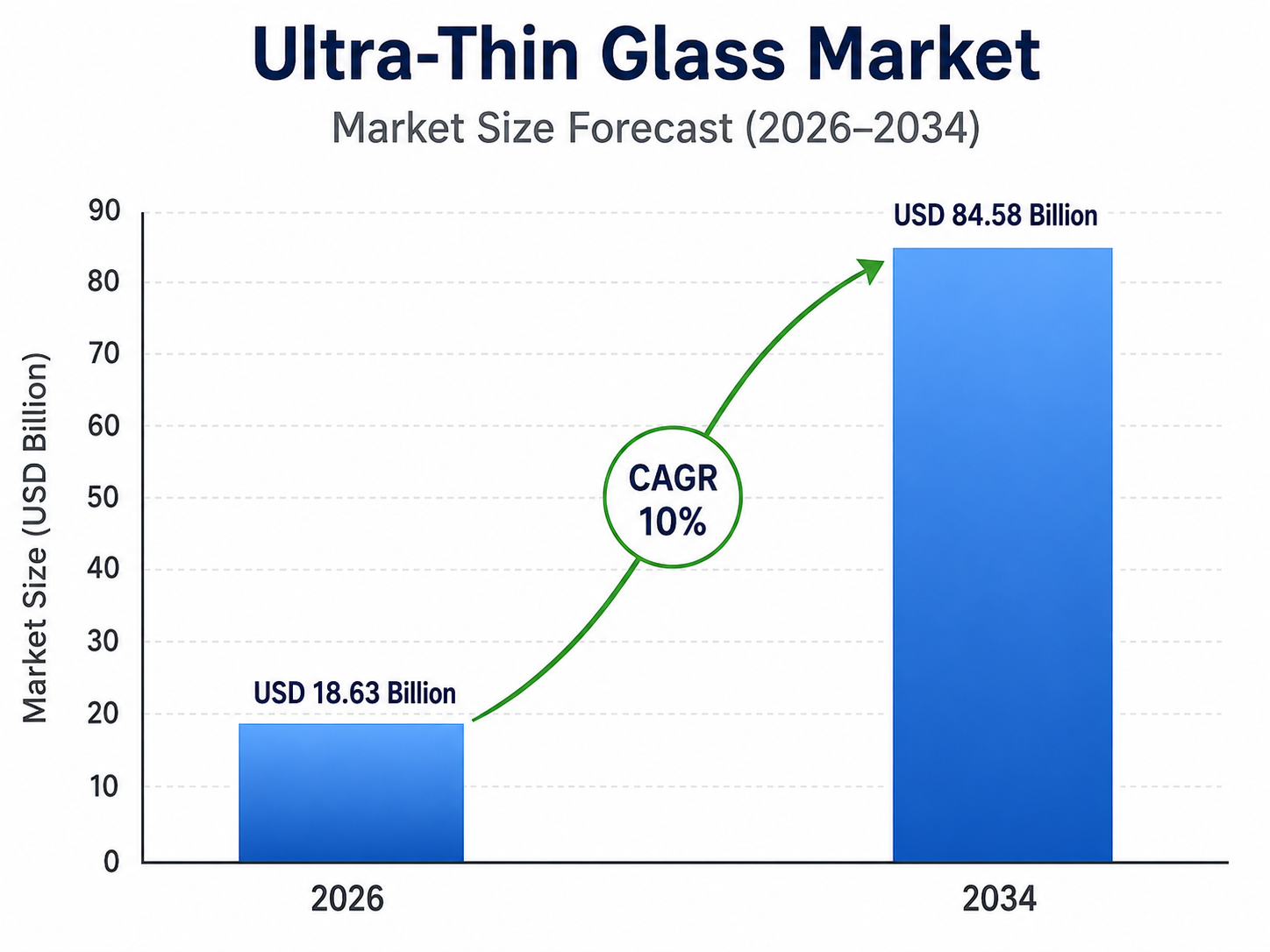

The Ultra-Thin Glass Market is estimated to be valued at $ 18.63 billion in 2026 and is projected to reach $ 40.1 billion by 2034, expanding at a CAGR of 10% from 2026 to 2034.

Ultra-thin glass generally refers to precision glass produced at sub-millimeter thicknesses for displays, touch panels, semiconductors, sensors, batteries, automotive electronics, medical devices, photovoltaics, and flexible products. It offers high optical clarity, dimensional stability, heat resistance, chemical resistance, and superior barrier performance compared with many polymer alternatives. Market growth is supported by foldable smartphones, wearable devices, advanced vehicle displays, miniaturized electronics, AR/VR systems, and high-performance semiconductor packaging. Manufacturers are investing in fusion, float, and down-draw production methods, chemical strengthening, precision cutting, surface coating, and roll-to-roll processing. As devices become thinner, lighter, and more flexible, ultra-thin glass is becoming an important functional material across electronics and mobility applications.

1. What is the latest trend in the Ultra-Thin Glass Market?

The latest trend is the development of chemically strengthened and bendable glass for foldable displays, wearables, and next-generation electronic devices.

Manufacturers are improving bending radius, scratch resistance, surface coatings, and resistance to repeated folding cycles.

Demand is also increasing for ultra-thin glass in AR waveguides, automotive displays, and advanced semiconductor packaging.

Roll-to-roll handling and precision laser processing are supporting higher-volume production.

2. What are the key challenges in the Ultra-Thin Glass Market?

Key challenges include brittleness, edge cracking, difficult handling, low production yields, and high precision-processing costs.

Extremely thin glass can be damaged during cutting, transport, coating, lamination, or device assembly.

Manufacturers must balance flexibility with scratch resistance, impact strength, optical quality, and dimensional stability.

Competition from flexible polymers and composite cover materials can also limit adoption in cost-sensitive applications.

3. What is the major driving factor for the Ultra-Thin Glass Market?

The major driving factor is rising demand for thinner, lighter, flexible, and high-resolution electronic products.

Smartphones, tablets, wearable devices, televisions, automotive displays, and foldable products require durable and optically clear substrates.

Ultra-thin glass also provides strong moisture, gas, heat, and chemical barriers for sensitive electronic components.

Continued device miniaturization and display-area expansion are strengthening long-term demand.

4. What is the major segment in the Ultra-Thin Glass Market and why?

Flat-panel and touch displays represent a major application segment because ultra-thin glass is widely used as a substrate, cover, and protective layer.

Its optical clarity, smooth surface, dimensional stability, and heat resistance support high-resolution display manufacturing.

Foldable phones, tablets, smartwatches, televisions, and automotive touchscreens are expanding the addressable market.

Higher display content per device further supports material consumption.

5. Which application or end-user is driving more demand?

Consumer electronics is driving the strongest demand through smartphones, laptops, tablets, televisions, wearables, and foldable devices.

Automotive manufacturers are also increasing adoption in digital cockpits, infotainment systems, instrument clusters, and head-up displays.

Semiconductor, medical-device, sensor, and biotechnology applications generate additional specialized demand.

The strongest opportunities occur where low thickness, optical quality, and material stability are essential.

6. Which region offers the highest growth potential and why?

Asia Pacific offers the highest growth potential due to its concentration of display, semiconductor, smartphone, automotive, and glass manufacturing capacity.

China, Japan, South Korea, Taiwan, and India are important production and consumption markets.

The region benefits from integrated electronics supply chains and continued investment in foldable and advanced display technologies.

Europe and North America remain important for specialized glass, semiconductor, automotive, and medical applications.

7. What strategies are major companies adopting in the market?

Major companies are focusing on chemical strengthening, thinner glass grades, improved flexibility, surface coating, and higher production yields.

They are partnering with display-panel manufacturers, semiconductor companies, automakers, and device brands for application-specific development.

Capacity expansion and investment in fusion, down-draw, precision cutting, and roll-based processing are strengthening competitiveness.

Companies are also pursuing patents and customized compositions for foldable and high-performance applications.

8. What are the leading companies in the Ultra-Thin Glass Market?

Leading companies include Corning, AGC, SCHOTT, Nippon Electric Glass, Nippon Sheet Glass, Central Glass, CSG Holding, Xinyi Glass, Luoyang Glass, and Changzhou Almaden.

These companies compete through glass thickness, optical quality, flexibility, surface strength, manufacturing yield, and customer qualification.

Corning, AGC, SCHOTT, and Nippon Electric Glass benefit from advanced glass-forming expertise and global electronics relationships.

Regional suppliers compete through capacity, pricing, processing services, and proximity to display manufacturers.

9. Why is ultra-thin glass strategically important for manufacturers?

Ultra-thin glass enables manufacturers to reduce device weight and thickness without sacrificing transparency, thermal stability, or barrier performance.

It supports premium product designs, larger displays, foldable formats, advanced sensors, and miniaturized electronic assemblies.

For glass producers, it creates higher-value opportunities beyond conventional architectural and container glass.

For electronics brands, material performance can directly influence durability, appearance, and user experience.

10. What is the future outlook for the Ultra-Thin Glass Market?

The market outlook remains positive as foldable electronics, smart vehicles, AR/VR devices, semiconductors, and wearable technologies expand.

Future growth will depend on improved bending durability, lower processing costs, higher manufacturing yields, and stronger surface protection.

Ultra-thin glass is expected to gain wider use in displays, sensors, batteries, medical devices, and flexible electronic substrates.

Companies offering scalable, defect-free, and application-specific products are likely to strengthen their market position.

Browse Related Reports

https://www.oganalysis.com/industry-reports/residential-real-estate-market-

https://www.oganalysis.com/industry-reports/round-hoop-houses-market

https://www.oganalysis.com/industry-reports/plastering-mortars-market

https://www.oganalysis.com/industry-reports/roof-insulation-market

https://www.oganalysis.com/industry-reports/hard-surface-flooring-market