The battery recycling market is witnessing significant growth as governments, industries, and environmental bodies prioritize sustainable management of end-of-life batteries amid rising adoption of electric vehicles (EVs), portable electronics, and renewable energy storage systems. Battery recycling involves the collection, disassembly, and processing of spent batteries to recover valuable metals such as lithium, cobalt, nickel, and lead, which can be reused in new battery manufacturing or other industrial applications. This not only mitigates environmental hazards associated with improper battery disposal but also reduces reliance on virgin raw material mining, addressing critical supply chain constraints for strategic battery materials. The market includes lead-acid battery recycling, which remains dominant due to its established infrastructure and high recyclability, and the rapidly growing lithium-ion battery recycling segment driven by EV proliferation, industrial energy storage, and electronics waste management initiatives globally.

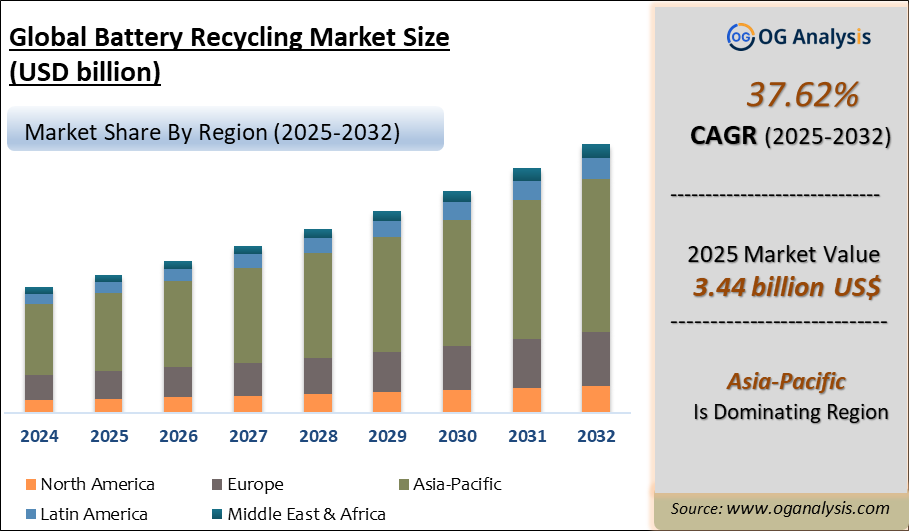

Regionally, Asia Pacific leads the battery recycling market, supported by strong battery manufacturing ecosystems in China, South Korea, and Japan, coupled with growing EV adoption and stringent environmental regulations for battery disposal. Europe follows closely with its advanced circular economy policies, battery directive revisions, and automotive OEM partnerships focusing on closed-loop recycling to achieve sustainability targets. North America is also expanding rapidly, driven by increasing EV sales, state-level recycling mandates, and investments in domestic battery material recovery facilities to reduce dependency on imported critical minerals. Challenges faced by the market include technological complexity in lithium-ion battery recycling, safety hazards in handling and transportation, and economic feasibility concerns. However, ongoing innovations in hydrometallurgical, pyrometallurgical, and direct recycling processes, along with strategic collaborations between battery manufacturers, recyclers, and governments, are expected to strengthen battery recycling infrastructure and market growth in the coming years.

Lead-acid batteries are the largest segment by battery chemistry in the battery recycling market due to their extensive use in automotive and industrial applications and the presence of established, cost-effective recycling systems worldwide. Lithium-based batteries are the fastest-growing segment, driven by rapid electric vehicle adoption and increasing demand for sustainable lithium-ion battery material recovery.

Pyrometallurgy is the largest process segment as it remains widely used for metal recovery from lead-acid and lithium-ion batteries through smelting. Hydrometallurgy is the fastest-growing process segment because of its higher recovery efficiency, lower environmental impact, and growing application in recycling lithium-ion batteries for critical metal extraction.

Key Insights

- The battery recycling market is driven by rising adoption of electric vehicles and renewable energy storage systems, creating substantial volumes of end-of-life lithium-ion and lead-acid batteries that require safe and sustainable disposal and material recovery solutions.

- Lead-acid batteries remain the largest segment due to their widespread use in automotive, industrial, and backup power applications, coupled with mature recycling infrastructure achieving recovery rates of over 95% for lead and polypropylene components.

- Lithium-ion battery recycling is the fastest-growing segment, fueled by increasing EV production and electronic device consumption, alongside growing regulatory pressures to recover critical materials such as lithium, cobalt, and nickel for new battery manufacturing.

- Asia Pacific is the largest regional market, supported by high battery manufacturing capacity in China, Japan, and South Korea, rising EV sales, and stringent environmental regulations mandating proper battery collection and recycling practices.

- Europe is advancing rapidly in battery recycling driven by revised EU battery directives, circular economy targets, and OEM commitments to integrate recycled materials into new EV battery supply chains to achieve sustainability goals.

- North America is witnessing significant investments in domestic lithium-ion battery recycling facilities to reduce reliance on imported critical minerals, enhance supply chain resilience, and support regional EV manufacturing growth under clean energy policies.

- Hydrometallurgical processes are gaining prominence for lithium-ion battery recycling, offering higher material recovery rates, lower energy consumption, and reduced environmental impact compared to traditional pyrometallurgical smelting methods.

- Technological challenges remain in safe disassembly, collection logistics, and economic viability of recycling low-cobalt chemistries, prompting companies to invest in automation, fire-suppression packaging, and direct recycling innovations to improve profitability.

- Strategic partnerships between battery manufacturers, recyclers, and mining companies are emerging to establish closed-loop recycling systems, securing critical material supply while enhancing ESG credentials and reducing carbon footprints.

- Government policies, such as extended producer responsibility (EPR) mandates, subsidies for recycling infrastructure, and research funding for advanced recovery technologies, are key enablers shaping future market expansion and competitiveness.

Reort Scope

| Parameter | Detail |

|---|---|

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Battery Chemistry,By Source, By State, By Processes By Material |

| Countries Covered | North America (USA, Canada, Mexico) Europe (Germany, UK, France, Spain, Italy, Rest of Europe) Asia-Pacific (China, India, Japan, Australia, Rest of APAC) The Middle East and Africa (Middle East, Africa) South and Central America (Brazil, Argentina, Rest of SCA) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10 % free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Datafile |

Market Segmentation

By Battery Chemistry:

Lead-Acid

Lithium-Based

Nickel-Based

Others

By Source:

Automotive Batteries

Industrial Batteries

Consumer & Electronic Appliance Batteries

By State:

Extraction of Material

Reuse, Repackaging, & Second Life

Disposal

By Process:

Hydrometallurgy

Pyro metallurgy

Mechanical Processes

Direct Recycling

By Material

Metals

Electrolytes

Plastics

Others

By Geography:

North America (USA, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

Asia-Pacific (China, India, Japan, Australia, South Korea, Rest of APAC)

The Middle East and Africa (Saudi Arabia,

UAE, Iran, South Africa, Rest of MEA)

South and Central America (Brazil, Argentina, Rest of SCA)

List Of Companies

Umicore (Belgium)

Glencore (Switzerland)

Li-Cycle Holdings Corp. (Canada)

Redwood Materials (USA)

American Battery Technology Company (ABTC) (USA)

Eco-Bat Technologies (UK)

Exide Technologies (USA)

EnerSys (USA)

Accurec Recycling GmbH (Germany)

Aqua Metals (USA)

Call2Recycle Inc. (USA)

Gravita India Limited (India)

Gopher Resource (USA)

RecycLiCo Battery Materials Inc. (Canada)

Aurubis AG (Germany)

What You Receive

• Global Battery Recycling market size and growth projections (CAGR), 2024- 2034• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Battery Recycling.

• Battery Recycling market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Battery Recycling market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Battery Recycling market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Battery Recycling market, Battery Recycling supply chain analysis.

• Battery Recycling trade analysis, Battery Recycling market price analysis, Battery Recycling Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Battery Recycling market news and developments.

The Battery Recycling Market international scenario is well established in the report with separate chapters on North America Battery Recycling Market, Europe Battery Recycling Market, Asia-Pacific Battery Recycling Market, Middle East and Africa Battery Recycling Market, and South and Central America Battery Recycling Markets. These sections further fragment the regional Battery Recycling market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways1. The report provides 2024 Battery Recycling market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Battery Recycling market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Battery Recycling market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Battery Recycling business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Battery Recycling Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Battery Recycling Pricing and Margins Across the Supply Chain, Battery Recycling Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Battery Recycling market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

1. Table of Contents

1.1 List of Tables

1.2 List of Figures

2. Global Battery Recycling Market Review, 2024

2.1 Battery Recycling Industry Overview

2.2 Research Methodology

3. Battery Recycling Market Insights

3.1 Battery Recycling Market Trends to 2034

3.2 Future Opportunities in Battery Recycling Market

3.3 Dominant Applications of Battery Recycling, 2024 Vs 2034

3.4 Key Types of Battery Recycling, 2024 Vs 2034

3.5 Leading End Uses of Battery Recycling Market, 2024 Vs 2034

3.6 High Prospect Countries for Battery Recycling Market, 2024 Vs 2034

4. Battery Recycling Market Trends, Drivers, and Restraints

4.1 Latest Trends and Recent Developments in Battery Recycling Market

4.2 Key Factors Driving the Battery Recycling Market Growth

4.2 Major Challenges to the Battery Recycling industry, 2025- 2034

4.3 Impact of Wars and geo-political tensions on Battery Recycling supply chain

5 Five Forces Analysis for Global Battery Recycling Market

5.1 Battery Recycling Industry Attractiveness Index, 2024

5.2 Battery Recycling Market Threat of New Entrants

5.3 Battery Recycling Market Bargaining Power of Suppliers

5.4 Battery Recycling Market Bargaining Power of Buyers

5.5 Battery Recycling Market Intensity of Competitive Rivalry

5.6 Battery Recycling Market Threat of Substitutes

6. Global Battery Recycling Market Data – Industry Size, Share, and Outlook

6.1 Battery Recycling Market Annual Sales Outlook, 2025- 2034 ($ Million)

6.1 Global Battery Recycling Market Annual Sales Outlook by Type, 2025- 2034 ($ Million)

6.2 Global Battery Recycling Market Annual Sales Outlook by Application, 2025- 2034 ($ Million)

6.3 Global Battery Recycling Market Annual Sales Outlook by End-User, 2025- 2034 ($ Million)

6.4 Global Battery Recycling Market Annual Sales Outlook by Region, 2025- 2034 ($ Million)

7. Asia Pacific Battery Recycling Industry Statistics – Market Size, Share, Competition and Outlook

7.1 Asia Pacific Market Insights, 2024

7.2 Asia Pacific Battery Recycling Market Revenue Forecast by Type, 2025- 2034 (USD Million)

7.3 Asia Pacific Battery Recycling Market Revenue Forecast by Application, 2025- 2034(USD Million)

7.4 Asia Pacific Battery Recycling Market Revenue Forecast by End-User, 2025- 2034 (USD Million)

7.5 Asia Pacific Battery Recycling Market Revenue Forecast by Country, 2025- 2034 (USD Million)

7.5.1 China Battery Recycling Analysis and Forecast to 2034

7.5.2 Japan Battery Recycling Analysis and Forecast to 2034

7.5.3 India Battery Recycling Analysis and Forecast to 2034

7.5.4 South Korea Battery Recycling Analysis and Forecast to 2034

7.5.5 Australia Battery Recycling Analysis and Forecast to 2034

7.5.6 Indonesia Battery Recycling Analysis and Forecast to 2034

7.5.7 Malaysia Battery Recycling Analysis and Forecast to 2034

7.5.8 Vietnam Battery Recycling Analysis and Forecast to 2034

7.6 Leading Companies in Asia Pacific Battery Recycling Industry

8. Europe Battery Recycling Market Historical Trends, Outlook, and Business Prospects

8.1 Europe Key Findings, 2024

8.2 Europe Battery Recycling Market Size and Percentage Breakdown by Type, 2025- 2034 (USD Million)

8.3 Europe Battery Recycling Market Size and Percentage Breakdown by Application, 2025- 2034 (USD Million)

8.4 Europe Battery Recycling Market Size and Percentage Breakdown by End-User, 2025- 2034 (USD Million)

8.5 Europe Battery Recycling Market Size and Percentage Breakdown by Country, 2025- 2034 (USD Million)

8.5.1 2024 Germany Battery Recycling Market Size and Outlook to 2034

8.5.2 2024 United Kingdom Battery Recycling Market Size and Outlook to 2034

8.5.3 2024 France Battery Recycling Market Size and Outlook to 2034

8.5.4 2024 Italy Battery Recycling Market Size and Outlook to 2034

8.5.5 2024 Spain Battery Recycling Market Size and Outlook to 2034

8.5.6 2024 BeNeLux Battery Recycling Market Size and Outlook to 2034

8.5.7 2024 Russia Battery Recycling Market Size and Outlook to 2034

8.6 Leading Companies in Europe Battery Recycling Industry

9. North America Battery Recycling Market Trends, Outlook, and Growth Prospects

9.1 North America Snapshot, 2024

9.2 North America Battery Recycling Market Analysis and Outlook by Type, 2025- 2034($ Million)

9.3 North America Battery Recycling Market Analysis and Outlook by Application, 2025- 2034($ Million)

9.4 North America Battery Recycling Market Analysis and Outlook by End-User, 2025- 2034($ Million)

9.5 North America Battery Recycling Market Analysis and Outlook by Country, 2025- 2034($ Million)

9.5.1 United States Battery Recycling Market Analysis and Outlook

9.5.2 Canada Battery Recycling Market Analysis and Outlook

9.5.3 Mexico Battery Recycling Market Analysis and Outlook

9.6 Leading Companies in North America Battery Recycling Business

10. Latin America Battery Recycling Market Drivers, Challenges, and Growth Prospects

10.1 Latin America Snapshot, 2024

10.2 Latin America Battery Recycling Market Future by Type, 2025- 2034($ Million)

10.3 Latin America Battery Recycling Market Future by Application, 2025- 2034($ Million)

10.4 Latin America Battery Recycling Market Future by End-User, 2025- 2034($ Million)

10.5 Latin America Battery Recycling Market Future by Country, 2025- 2034($ Million)

10.5.1 Brazil Battery Recycling Market Analysis and Outlook to 2034

10.5.2 Argentina Battery Recycling Market Analysis and Outlook to 2034

10.5.3 Chile Battery Recycling Market Analysis and Outlook to 2034

10.6 Leading Companies in Latin America Battery Recycling Industry

11. Middle East Africa Battery Recycling Market Outlook and Growth Prospects

11.1 Middle East Africa Overview, 2024

11.2 Middle East Africa Battery Recycling Market Statistics by Type, 2025- 2034 (USD Million)

11.3 Middle East Africa Battery Recycling Market Statistics by Application, 2025- 2034 (USD Million)

11.4 Middle East Africa Battery Recycling Market Statistics by End-User, 2025- 2034 (USD Million)

11.5 Middle East Africa Battery Recycling Market Statistics by Country, 2025- 2034 (USD Million)

11.5.1 South Africa Battery Recycling Market Outlook

11.5.2 Egypt Battery Recycling Market Outlook

11.5.3 Saudi Arabia Battery Recycling Market Outlook

11.5.4 Iran Battery Recycling Market Outlook

11.5.5 UAE Battery Recycling Market Outlook

11.6 Leading Companies in Middle East Africa Battery Recycling Business

12. Battery Recycling Market Structure and Competitive Landscape

12.1 Key Companies in Battery Recycling Business

12.2 Battery Recycling Key Player Benchmarking

12.3 Battery Recycling Product Portfolio

12.4 Financial Analysis

12.5 SWOT and Financial Analysis Review

14. Latest News, Deals, and Developments in Battery Recycling Market

14.1 Battery Recycling trade export, import value and price analysis

15 Appendix

15.1 Publisher Expertise

15.2 Battery Recycling Industry Report Sources and Methodology

Get Free Sample

At OG Analysis, we understand the importance of informed decision-making in today's dynamic business landscape. To help you experience the depth and quality of our market research reports, we offer complimentary samples tailored to your specific needs.

Start Now! Please fill the form below for your free sample.

Why Request a Free Sample?

Evaluate Our Expertise: Our reports are crafted by industry experts and seasoned analysts. Requesting a sample allows you to assess the depth of research and the caliber of insights we provide.

Tailored to Your Needs: Let us know your industry, market segment, or specific topic of interest. Our free samples are customized to ensure relevance to your business objectives.

Witness Actionable Insights: See firsthand how our reports go beyond data, offering actionable insights and strategic recommendations that can drive your business forward.

Embark on your journey towards strategic decision-making by requesting a free sample from OG Analysis. Experience the caliber of insights that can transform the way you approach your business challenges.

FAQ's

The Global Battery Recycling Market is estimated to generate USD 3.4 billion in revenue in 2025

The Global Battery Recycling Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 37.62% during the forecast period from 2025 to 2034.

The Battery Recycling Market is estimated to reach USD 62.7 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!