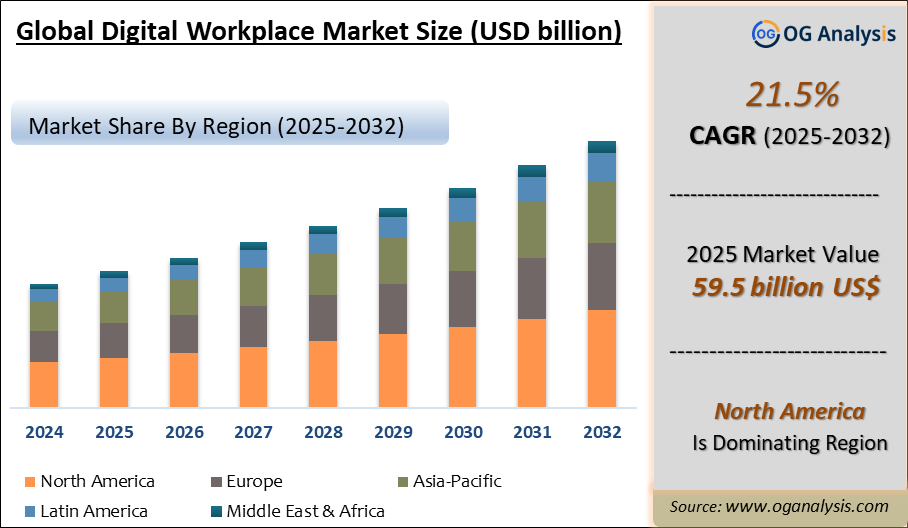

"The Global Digital Workplace Market Size was valued at USD 50.2 billion in 2024 and is projected to reach USD 59.5 billion in 2025. Worldwide sales of Digital Workplace are expected to grow at a significant CAGR of 21.5%, reaching USD 355.7 billion by the end of the forecast period in 2034."

Digital Workplace Market Overview

The digital workplace market has seen rapid growth and transformation in recent years, driven by the increasing adoption of digital technologies and the shift towards remote and hybrid work models. A digital workplace encompasses a range of tools and solutions that enable employees to work from anywhere, at any time, using any device. These solutions include collaboration tools, cloud-based applications, mobile solutions, and advanced communication platforms. The global digital workplace market was valued at approximately USD 22.7 billion in 2023 and is projected to reach USD 72.2 billion by 2030, growing at a compound annual growth rate (CAGR) of 15.4% during the forecast period. This growth is fueled by the rising demand for enhanced productivity, flexibility, and employee engagement in the modern workforce.

The COVID-19 pandemic has significantly accelerated the adoption of digital workplace solutions as organizations worldwide have had to adapt to new ways of working. Remote work, once a necessity, has now become a standard practice for many businesses. This shift has highlighted the importance of robust digital infrastructure and tools that support seamless collaboration and communication. Companies are increasingly investing in digital workplace solutions to ensure business continuity, improve operational efficiency, and enhance the employee experience. As the workforce becomes more dispersed and mobile, the digital workplace market is expected to continue its upward trajectory, offering innovative solutions to meet the evolving needs of organizations.

Digital Workplace Market: Latest Trends, Drivers, Challenges

Several key trends are shaping the digital workplace market. One of the most prominent trends is the integration of artificial intelligence (AI) and machine learning (ML) into workplace tools. AI and ML are being used to automate routine tasks, provide data-driven insights, and enhance decision-making processes. For instance, AI-powered chatbots and virtual assistants are becoming common in digital workplaces, helping employees with tasks such as scheduling, information retrieval, and customer service. Another significant trend is the rise of unified communication and collaboration (UC&C) platforms. These platforms integrate various communication tools, such as video conferencing, instant messaging, and email, into a single interface, facilitating seamless collaboration among remote teams.

The digital workplace market is driven by several key factors. The increasing need for employee flexibility and remote work options is a major driver. As more companies adopt remote and hybrid work models, the demand for digital tools that support remote work is growing. Additionally, the need to enhance employee productivity and engagement is driving the adoption of digital workplace solutions. These tools enable employees to collaborate effectively, access information easily, and stay connected with their teams, regardless of their location. The rapid advancements in cloud computing and mobile technologies are also contributing to the market's growth. Cloud-based solutions provide the scalability, flexibility, and accessibility needed to support a digital workplace, while mobile technologies enable employees to work from anywhere, using any device.

Despite the positive growth outlook, the digital workplace market faces several challenges. One of the primary challenges is ensuring data security and privacy. As more data is stored and accessed digitally, the risk of cyber threats and data breaches increases. Organizations need to implement robust security measures to protect sensitive information and maintain compliance with data protection regulations. Another challenge is the integration of digital workplace tools with existing IT infrastructure. Organizations often face difficulties in integrating new solutions with legacy systems, leading to inefficiencies and increased costs. Additionally, the rapid pace of technological change requires continuous investment in new tools and solutions, which can be a financial burden for some organizations. Addressing these challenges is crucial for the sustained growth and success of the digital workplace market.

Major Players in the Digital Workplace Market

1. Microsoft Corporation

2. Google LLC

3. IBM Corporation

4. Cisco Systems, Inc.

5. Citrix Systems, Inc.

6. VMware, Inc.

7. Accenture plc

8. Hewlett Packard Enterprise Development LP

9. Atos SE

10. Capgemini SE

11. DXC Technology Company

12. Unisys Corporation

13. ServiceNow, Inc.

14. T-Systems International GmbH

15. Infosys Limited

Market Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD Billion |

| Market Splits Covered | By Component, By Deployment Mode, By Organization Size, and By Industry Vertical |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

- By Component:

- Solutions

- Services

- By Deployment Mode:

- On-Premise

- Cloud

- By Organization Size:

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- By Industry Vertical:

- IT & Telecommunications

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare

- Retail

- Manufacturing

- Government

- Others

- By Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Get Free Sample

At OG Analysis, we understand the importance of informed decision-making in today's dynamic business landscape. To help you experience the depth and quality of our market research reports, we offer complimentary samples tailored to your specific needs.

Start Now! Please fill the form below for your free sample.

Why Request a Free Sample?

Evaluate Our Expertise: Our reports are crafted by industry experts and seasoned analysts. Requesting a sample allows you to assess the depth of research and the caliber of insights we provide.

Tailored to Your Needs: Let us know your industry, market segment, or specific topic of interest. Our free samples are customized to ensure relevance to your business objectives.

Witness Actionable Insights: See firsthand how our reports go beyond data, offering actionable insights and strategic recommendations that can drive your business forward.

Embark on your journey towards strategic decision-making by requesting a free sample from OG Analysis. Experience the caliber of insights that can transform the way you approach your business challenges.

FAQ's

The Digital Workplace Market is estimated to reach USD 238.4 billion by 2032.

The Global Digital Workplace Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% during the forecast period from 2025 to 2032.

The Global Digital Workplace Market is estimated to generate USD 50.2 billion in revenue in 2024.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!