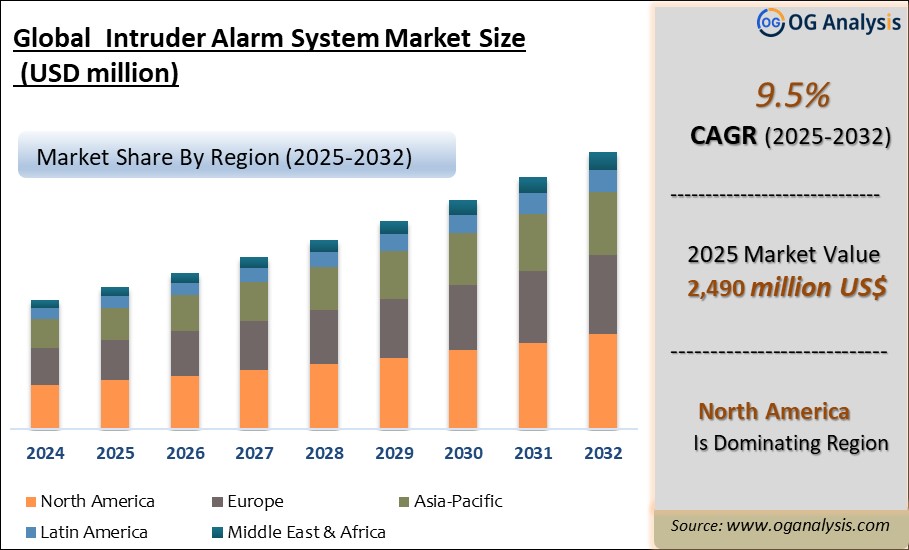

"The Global Intruder Alarm System Market Size was valued at USD 2,301 million in 2024 and is projected to reach USD 2,490 million in 2025. Worldwide sales of Intruder Alarm System are expected to grow at a significant CAGR of 9.5%, reaching USD 5,781 million by the end of the forecast period in 2034."

Intruder Alarm System Market Overview

The intruder alarm system market has experienced significant growth due to the increasing need for security and the protection of assets and lives. Intruder alarm systems are designed to detect unauthorized entry into a building or area and alert the owner or authorities. These systems are widely used in residential, commercial, and industrial applications. The global market for intruder alarm systems is driven by rising crime rates, increasing urbanization, and the growing adoption of smart home technologies. In 2023, the market was valued at approximately USD 4.7 billion and is projected to grow at a compound annual growth rate (CAGR) of around 6.2% over the forecast period, reaching USD 7.1 billion by 2030.

Geographically, North America dominates the intruder alarm system market, attributed to high awareness about security, advanced technological infrastructure, and the presence of major market players. Europe follows closely, driven by stringent regulations and standards for security systems. The Asia-Pacific region is expected to witness the highest growth rate, fueled by rapid urbanization, rising disposable incomes, and increasing awareness about the importance of security systems in countries like China, India, and Japan. This market overview delves into the current trends, drivers, and challenges impacting the intruder alarm system market, providing insights into future growth opportunities.

Intruder Alarm System Market: Latest Trends, Drivers, and Challenges

One of the significant trends in the intruder alarm system market is the integration of advanced technologies such as artificial intelligence (AI) and the Internet of Things (IoT). AI-enabled intruder alarm systems can analyze patterns and behaviors to differentiate between actual threats and false alarms, thereby improving accuracy and reliability. IoT integration allows these systems to be part of a connected home ecosystem, enabling remote monitoring and control through smartphones and other devices. Another trend is the growing preference for wireless alarm systems over traditional wired systems. Wireless systems offer easier installation, flexibility in placement, and integration with other wireless devices, making them a popular choice among consumers and businesses alike.

The primary drivers of the intruder alarm system market include the increasing crime rates and the growing need for effective security solutions. Urbanization and the expansion of smart cities are also driving the demand for advanced security systems. Moreover, the rising adoption of smart home technologies is boosting the market for intruder alarm systems. Homeowners and businesses are increasingly investing in smart security solutions that offer convenience, real-time monitoring, and enhanced protection. Additionally, government regulations and initiatives promoting the installation of security systems in residential and commercial buildings are further propelling market growth. Technological advancements, such as the development of AI and IoT-enabled security systems, are also driving innovation and adoption in the market.

Despite the positive growth outlook, the intruder alarm system market faces several challenges. One of the main challenges is the high cost of advanced security systems, which can be prohibitive for small and medium-sized enterprises (SMEs) and residential users. Additionally, the installation and maintenance of these systems require skilled professionals, and a shortage of such expertise can limit market growth. False alarms are another significant issue, leading to unnecessary emergency responses and a lack of trust in the system's reliability. Privacy concerns related to surveillance and data collection by security systems can also pose challenges, as users become more aware of data security and privacy issues. Furthermore, the rapid pace of technological advancements requires continuous updates and innovations, posing a challenge for companies to keep their offerings current and effective.

Major Players in the Intruder Alarm System Market

1. Honeywell International Inc.

2. Johnson Controls International plc

3. Siemens AG

4. Robert Bosch GmbH

5. ADT Inc.

6. United Technologies Corporation (Carrier Global Corporation)

7. Securitas AB

8. Tyco Security Products

9. ABB Ltd.

10. Assa Abloy Group

11. Hikvision Digital Technology Co., Ltd.

12. FLIR Systems, Inc.

13. Nortek Security & Control LLC

14. RISCO Group

15. Ingersoll Rand Plc

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD million |

| Market Splits Covered | By product Type, and By End-User |

| Countries Covered | North America (USA, Canada, Mexico) Europe (Germany, UK, France, Spain, Italy, Rest of Europe) Asia-Pacific (China, India, Japan, Australia, Rest of APAC) The Middle East and Africa (Middle East, Africa) South and Central America (Brazil, Argentina, Rest of SCA) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Datafile |

Market Segmentation

- By Product Type:

- Control Panels

- Motion Detectors

- Glass Break Detectors

- Door/Window Sensors

- Others

- By End User:

- Residential

- Commercial

- Industrial

- Government

- By Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Get Free Sample

At OG Analysis, we understand the importance of informed decision-making in today's dynamic business landscape. To help you experience the depth and quality of our market research reports, we offer complimentary samples tailored to your specific needs.

Start Now! Please fill the form below for your free sample.

Why Request a Free Sample?

Evaluate Our Expertise: Our reports are crafted by industry experts and seasoned analysts. Requesting a sample allows you to assess the depth of research and the caliber of insights we provide.

Tailored to Your Needs: Let us know your industry, market segment, or specific topic of interest. Our free samples are customized to ensure relevance to your business objectives.

Witness Actionable Insights: See firsthand how our reports go beyond data, offering actionable insights and strategic recommendations that can drive your business forward.

Embark on your journey towards strategic decision-making by requesting a free sample from OG Analysis. Experience the caliber of insights that can transform the way you approach your business challenges.

FAQ's

The Global Intruder Alarm System Market is estimated to generate USD 2301 million in revenue in 2024.

The Global Intruder Alarm System Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% during the forecast period from 2025 to 2032.

The Intruder Alarm System Market is estimated to reach USD 4755.9 million by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!