"The 155Mm Ammunition Market was valued at $ 4.8 billion in 2026 and is projected to reach $ 6.3 billion by 2034, growing at a CAGR of 3.6%."

The 155Mm Ammunition Market has become a strategically important segment within the broader defense and artillery ecosystem, driven by the renewed relevance of tube artillery in conventional warfare, border security, deterrence planning, and sustained stockpile modernization. This caliber remains the standard for many NATO and allied artillery systems, making it central to how armed forces approach long-range firepower, operational readiness, and ammunition interoperability. Core end uses include self-propelled howitzers, towed artillery systems, and advanced precision-enabled artillery platforms deployed by land forces for battlefield support, counter-battery missions, suppression operations, and high-intensity combat scenarios. The market is also supported by demand for training rounds, extended-range variants, modular propelling charges, and specialized shell types tailored to different operational doctrines.

Recent trends show a strong shift toward production expansion, supply-chain localization, and greater emphasis on sovereign ammunition capacity across Europe and allied markets. Companies are increasingly focusing on scalable manufacturing, automation in shell and propellant production, and improved compatibility with modern artillery systems. Market growth is being driven by replenishment of depleted inventories, rising defense preparedness, alliance-led standardization, and the need for resilient supply lines for critical munitions. The competitive landscape includes major defense manufacturers, state-backed ammunition producers, explosives and propellant specialists, and cross-border industrial partnerships aimed at expanding large-caliber output. Overall, the market outlook remains highly active, with procurement, co-production agreements, and industrial capacity build-out shaping the next phase of competition and development.

Regional Analysis

North America 155Mm Ammunition Market

North America 155Mm Ammunition Market is characterized by strong defense industrial mobilization, stockpile replenishment priorities, and sustained investment in artillery ammunition manufacturing resilience. Market dynamics are being shaped by production expansion programs, modernization of legacy ammunition plants, and closer alignment between ammunition output and land-force readiness requirements. Lucrative opportunities for companies are emerging in shell body manufacturing, energetics, propellants, modular charge systems, automation, and supply-chain support services. The latest trend in the region is the move toward higher-volume, more automated, and more secure production ecosystems, while the forecast remains positive as defense agencies continue to prioritize scalable output, interoperability, and dependable long-term supply.

Asia Pacific 155Mm Ammunition Market

Asia Pacific 155Mm Ammunition Market is gaining momentum as regional governments strengthen artillery preparedness, expand domestic defense production, and deepen cross-border industrial cooperation. Market dynamics are influenced by strategic security concerns, artillery fleet modernization, and growing interest in reducing dependence on imported ammunition through local manufacturing and technology partnerships. Companies can find attractive opportunities in licensed production, filling and finishing capabilities, component supply, explosives integration, and modernization support for compatible artillery platforms. A major recent trend is the increasing willingness of regional players to enter joint manufacturing arrangements with foreign defense firms, and the forecast points to continued demand supported by national self-reliance goals and broader military modernization programs.

Europe 155Mm Ammunition Market

Europe 155Mm Ammunition Market remains the most active regional center for industrial expansion, driven by urgent replenishment needs, defense readiness concerns, and strong political support for sovereign ammunition capacity. Market dynamics are centered on new factory development, joint ventures, long-term procurement contracts, and broader efforts to strengthen the full ammunition supply chain from propellants to completed rounds. Lucrative opportunities are especially strong for manufacturers of shells, fuzes, charges, explosives, and production equipment, as well as companies able to offer rapid scale-up and reliable delivery. Recent developments across the region show accelerating collaboration between local and international defense firms, and the forecast remains highly favorable as Europe continues building a deeper, faster, and more resilient 155Mm ammunition ecosystem.

Middle East & Africa 155Mm Ammunition Market

Middle East & Africa 155Mm Ammunition Market is developing through a combination of defense modernization, strategic stockpiling, and interest in strengthening local ammunition manufacturing capacity. Market dynamics are shaped by regional security requirements, procurement of artillery-capable land systems, and growing recognition of the importance of assured munitions access during prolonged operational scenarios. Companies have promising opportunities in localized assembly, ammunition component supply, explosives processing, and government-linked industrial partnerships that support national defense goals. The latest trend is a gradual shift from pure import dependence toward selective domestic capability building, while the forecast remains constructive as countries continue to prioritize supply security, operational readiness, and industrial diversification.

South & Central America 155Mm Ammunition Market

South & Central America 155Mm Ammunition Market is progressing at a measured pace, supported by selective artillery modernization, defense manufacturing ambitions, and the need to maintain credible ammunition reserves for national security requirements. Market dynamics are influenced by budget-conscious procurement strategies, interest in domestic defense production, and efforts to upgrade existing artillery support capabilities without overextending procurement cycles. Lucrative opportunities for companies lie in technology transfer, localized manufacturing support, ammunition refurbishment, component production, and long-term maintenance-linked supply arrangements. The latest trend is a gradual move toward practical, partnership-led industrial strengthening, and the forecast suggests steady growth as regional defense organizations place greater emphasis on readiness, stock sustainability, and more reliable ammunition sourcing.

Key Insights

- Demand for 155Mm ammunition has shifted from cyclical procurement to sustained strategic priority, especially as governments rebuild stockpiles and strengthen artillery readiness. This change has made the segment less dependent on short-term orders and more linked to long-term defense planning. It is now treated as a core element of combat endurance and allied interoperability.

- Standardization around NATO-compatible artillery systems continues to support the dominance of this caliber across multiple armed forces. That standardization improves logistical coordination, joint-force compatibility, and procurement efficiency across allied users. It also helps manufacturers compete through common-specification production and export-aligned platforms.

- High-explosive and general-purpose artillery rounds remain the most influential product types because they serve core battlefield, suppression, and support roles. At the same time, interest is rising in extended-range and specialized munitions that improve tactical flexibility. This is widening the product mix within the market.

- Production capacity expansion has become one of the most important market drivers, with manufacturers and governments investing in new plants, joint ventures, and localized manufacturing programs. Supply resilience is now a competitive differentiator for producers. Companies with faster scale-up capability are better positioned to win contracts.

- Propellants, modular charge systems, explosives, and energetic materials are becoming critical supporting segments in overall market development. Ammunition output is no longer viewed only at the shell level, but across the full industrial chain. This is increasing the strategic role of upstream chemical and component suppliers.

- Europe remains a leading center of market momentum because of urgent replenishment programs, cross-border industrial cooperation, and growing emphasis on sovereign defense manufacturing. Partnerships between global primes and regional producers are accelerating technology transfer and output growth. This trend is likely to continue shaping competitive dynamics.

- Land-force modernization is reinforcing the role of advanced artillery systems, which in turn is sustaining demand for compatible 155Mm ammunition families. As self-propelled and networked artillery platforms spread, ammunition requirements are becoming more performance-driven. This favors suppliers that can support both volume and modern system compatibility.

- Future market development will increasingly depend on industrial agility, export licensing strength, and the ability to integrate into allied procurement ecosystems. Companies that offer dependable output, modular production models, and long-term supply assurance will gain advantage. The market is evolving toward scale, security of supply, and strategic manufacturing depth.

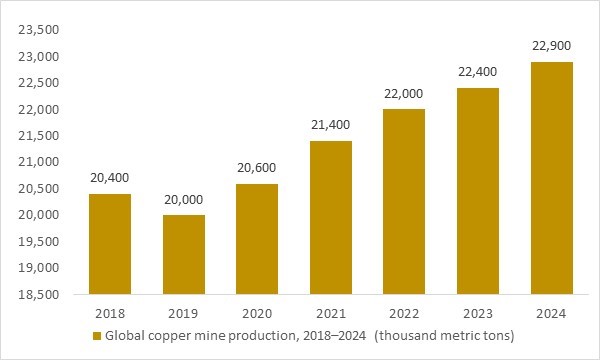

Global copper mine production, 2018–2024 (thousand metric tons, copper content)

Figure: Global copper mine production has increased from just over 20 million tonnes in 2018 to almost 23 million tonnes in 2024, expanding the supply base for high-purity copper used in 155mm projectile rotating bands, fuzes and guidance electronics. OG Analysis estimates, derived from USGS and ICSG data, show how this gradual rise in copper output underpins the ability of defense manufacturers to scale 155mm ammunition production and also supports copper-intensive radiation-detection, monitoring and security systems.

Global copper mine production has risen steadily from around 20.4 million tonnes in 2018 to nearly 23 million tonnes in 2024, highlighting a gradually expanding supply of this strategic non-ferrous metal. This growth underpins the availability of copper strip, bar and wire used in 155mm projectile rotating bands, fuzes, guidance electronics and cabling, enabling sustained ramp-up in artillery shell manufacturing. At the same time, the same copper supply base is critical for high-reliability wiring, connectors and electronics in radiation-detection, monitoring and security systems deployed at borders, ports and critical infrastructure. As defense and security spending intensifies, the combination of rising demand and a still-tight copper market frames raw-material pricing and availability as a key structural factor shaping both the 155mm ammunition market and the wider radiation-detection-monitoring-and-security market.

Market Scope

| Parameter | 155Mm Ammunition Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Technology, By Application, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

155Mm Ammunition Market Segmentation

By Technology

- Guided

- Unguided

By Application

- Projectiles

- Propellants

- Tanks

- Other Applications

By End User

- Naval Forces

- Ground Forces

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Analysed

Raytheon Technologies Inc., General Dynamics Corporation, Northrop Grumman Corporation, BAE Systems PLC, China North Industries Corporation, Thales Group, Leonardo S.p.A., Olin Corporation, Rheinmetall AG, Elbit Systems Ltd., Saab AB, Norma Precision AB, Remington Arms Company LLC, Nammo AS, Denel SOC Ltd., Nexter Group, Fiocchi Munizioni SPA, Ammo Inc., RUAG Holding AG, Munitions India Ltd., Savage Arms, Hornady Manufacturing Company, MSM Group s.r.o., Federal Premium Ammunition, Winchester Ammunition Inc., Magtech Ammunition Company Inc., Poongsan Corporation, JSC Arsenal AD.

Recent Industry Developments

February 2026 - BAE Systems and Polska Grupa Zbrojeniowa signed an agreement to establish a new 155mm artillery ammunition manufacturing facility in Poland. The move expands local production capability and strengthens Poland’s role in European ammunition supply chains.

February 2026 - Rheinmetall announced a seven-year framework agreement with Denmark covering multiple ammunition types, including 155mm artillery rounds. The contract reinforces Rheinmetall’s position in long-term NATO ammunition supply and supports sustained artillery replenishment demand.

December 2025 - Rheinmetall announced the acquisition of ammunition specialist Muni Berka, adding major storage and logistics capacity for large-calibre ammunition. The deal enhances Rheinmetall’s ability to support larger-scale handling and supply of 155mm projectiles and complete shots.

December 2025 - ZVS holding, part of Czechoslovak Group, launched a new automated large-calibre ammunition filling line in Slovakia. The new line significantly strengthens its 155mm artillery ammunition production capacity and supports rising European demand.

November 2025 - Rheinmetall held the groundbreaking for a new 155mm artillery ammunition plant in Lithuania through its local joint venture. The project is designed to expand regional production and is paired with plans for a propellant charges centre of excellence.

October 2025 - Czechoslovak Group announced the launch of licensed production of 155mm ammunition in Ukraine with Ukrainian Armor. The program starts with significant local content and is intended to scale up over time as a major domestic supply source.

September 2025 - Rheinmetall announced that Latvia had ordered a new ammunition factory featuring shell forging and filling lines. The facility is intended to produce 155mm artillery shells and deepen domestic participation in the regional munitions value chain.

August 2025 - MSM North America, part of Czechoslovak Group, won a U.S. Army contract to build the Future Artillery Complex in the United States. The facility is planned to load and assemble large monthly volumes of 155mm rounds, strengthening North American and allied ammunition production capacity.

FAQ's

The Global 155Mm Ammunition Market is estimated to generate USD 4.8 billion in revenue in 2026.

The Global 155Mm Ammunition Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 3.64% during the forecast period from 2026 to 2034.

The 155Mm Ammunition Market is estimated to reach USD 6.3 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!