"The 5g security Market was valued at $ 9.32 billion in 2025 and is projected to reach $ 39.71 billion by 2034, growing at a CAGR of 17.47%."

The 5G Security Market is emerging as a critical component of the global telecommunications infrastructure, driven by the rollout of high-speed, low-latency 5G networks that power advanced technologies such as autonomous vehicles, smart cities, industrial automation, and IoT ecosystems. With 5G enabling exponentially more connected devices and data exchange, the need to secure networks, endpoints, and applications has become a top priority for governments, telecom providers, and enterprises. The market encompasses a wide array of solutions including network segmentation, endpoint detection and response (EDR), security orchestration, next-gen firewalls, and zero-trust architectures. As cyber threats evolve in sophistication, the demand for robust, scalable, and AI-driven security frameworks tailored for 5G environments is accelerating.

As 5G networks shift from non-standalone (NSA) to standalone (SA) architectures, the security perimeter expands, creating new challenges across edge devices, virtualized network functions, and multi-access edge computing (MEC). Telecom operators are collaborating with cybersecurity vendors to develop integrated solutions that offer real-time threat intelligence, identity and access management, and compliance with international standards such as 3GPP and NIST. Additionally, regulatory pressure is prompting nations to develop sovereign cybersecurity capabilities to protect national infrastructure. Enterprises across sectors including healthcare, finance, manufacturing, and logistics are also investing in 5G security to safeguard data, ensure service continuity, and mitigate operational risks arising from cyberattacks targeting mission-critical applications.

Key Market Insights

-

The expansion of standalone 5G networks is accelerating the demand for advanced security solutions that can handle distributed architecture, edge computing, and software-defined networking, which significantly increase the attack surface.

-

Telecom operators are adopting zero-trust security models that verify every network access request and continuously authenticate device identity to reduce the risk of lateral attacks and insider threats in 5G ecosystems.

-

Cloud-native security solutions are gaining traction as 5G networks increasingly rely on virtualized infrastructure and container-based network functions that require dynamic, automated threat detection and response capabilities.

-

AI and machine learning are being integrated into 5G security tools to enhance anomaly detection, automate policy enforcement, and respond proactively to potential threats before they compromise network integrity.

-

Governments and regulatory bodies are pushing for stringent compliance with global security standards such as 3GPP, GDPR, and NIST to ensure the safe deployment and operation of 5G services across industries.

-

Enterprises in sectors like healthcare, manufacturing, and financial services are investing in private 5G networks with embedded security to protect sensitive data and support mission-critical applications in real time.

-

The use of network slicing in 5G requires dedicated security controls for each slice to prevent data leakage and maintain service-level isolation, adding complexity to security management frameworks.

-

Identity and access management is becoming essential in 5G networks to control device authentication, authorize network access, and enforce encryption policies for billions of connected IoT devices.

-

Partnerships between telecom providers, cybersecurity vendors, and cloud platforms are expanding to create integrated 5G security ecosystems that address end-to-end protection, including endpoints, core, and edge infrastructure.

-

Real-time threat intelligence sharing and orchestration platforms are helping telecom operators and enterprises respond faster to sophisticated cyberattacks, while enhancing situational awareness across distributed 5G infrastructures

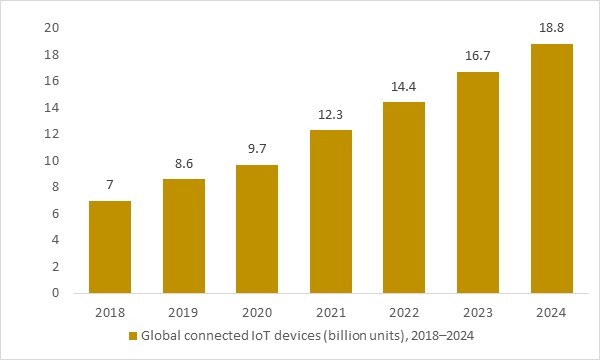

Global connected IoT devices (billion units), 2018–2024

Figure: Global connected IoT devices increased from around 7.0 billion units in 2018 to an estimated 18.8 billion units in 2024, significantly expanding the digital attack surface across mobile networks. As a growing share of these devices connect via 5G and 5G standalone architectures, telecom operators and enterprises face heightened risks related to signaling abuse, identity fraud, distributed denial-of-service attacks, and insecure edge connectivity. OG Analysis estimates, derived from global IoT ecosystem tracking and telecom industry studies, illustrate how rapid IoT proliferation directly strengthens long-term demand for advanced 5G security solutions worldwide.

- Global connected IoT devices expanded rapidly from around 7.0 billion in 2018 to an estimated 18.8 billion in 2024, sharply increasing the number of endpoints operating on mobile networks. As a rising share of these devices migrate to 5G and 5G standalone architectures, the overall network attack surface expands across radio, core, edge, and cloud layers. This growth heightens exposure to threats such as signaling abuse, identity spoofing, botnet formation, and distributed denial-of-service attacks. Consequently, the accelerating scale of IoT connectivity directly underpins sustained demand for robust and specialized 5G security solutions.

Regional Insights

North America 5G Security Market

In North America, the 5G security landscape is rapidly advancing, propelled by aggressive 5G network deployments across telecom and enterprise sectors. The region is witnessing heightened integration of zero-trust frameworks, AI-driven threat intelligence, and cloud-native security tools into 5G architectures to address complex risks tied to virtualization and edge computing. Enterprises in verticals like automotive, healthcare, and industrial automation are prioritizing robust security layers to protect critical systems and data. Service providers offering advanced network slicing protection, identity and access management, and real-time analytics are ideally positioned to lead in this environment, driven by a strong regulatory focus on privacy and infrastructure resilience.

Asia Pacific 5G Security Market

Asia Pacific is emerging as a high-growth region for 5G security, supported by fast-paced telecom expansion, smart city initiatives, and dynamic IoT ecosystems across nations such as China, India, Japan, and Southeast Asia. There is growing demand for flexible, cost-effective security solutions that integrate seamlessly with large-scale 5G infrastructure rollouts. Security vendors offering localized threat monitoring, lightweight endpoint protection for IoT devices, and standards-compliant access control solutions are gaining traction. Public-private partnerships in urban digitalization and national cybersecurity enhancements are contributing to a flourishing 5G security ecosystem in this diverse and rapidly evolving market.

Europe 5G Security Market

Europe’s 5G security market is evolving steadily under the influence of robust regulatory frameworks, such as EU cybersecurity directives and GDPR, which demand transparency, encryption, and accountability in network operations. Telecom operators and critical industries are investing in secure network slicing, edge protection, and data sovereignty assurances. Vendors that provide multi-tenant security controls, compliance-ready orchestration, and interoperability with 5G core and RAN components are finding competitive advantage. Sustainability-focused infrastructure and the integration of secure edge architectures for smart infrastructure further reinforce Europe’s forward-leaning and risk-conscious approach to 5G security.

Report Scope

| Parameter | 5g Security Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

5g security Market Segments Covered In The Report

By Components

- Solutions

- Services

By Deployment Type

- On-Premises

- Cloud

By Organization Size

- Large Enterprises

- SMEs

By Application

- Virtual and Augmented Reality

- Connected Automotive

- Smart Manufacturing

- Smart Cities

- Other Applications

By Industry Vertical

- Manufacturing

- Healthcare

- Retail

- Automotive and Transportation

- BFSI

- Other Industry Verticals

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

Telefonaktiebolaget LM Ericsson, Palo Alto Networks Inc., Cisco Systems Inc., Allot Ltd., Huawei Technologies Co. Ltd., A10 Networks, Nokia Networks, F5 Networks Inc., Juniper Networks Inc., Spirent Communications plc, Fortinet Inc., Mobileum Inc., Trend Micro Inc., Radware Inc., Riscure B.V., G+D Mobile Security, China Mobile Ltd., Cloudflare Inc., DigitCert Inc., Infineon Technologies AG, ZTE Corporation, Akamai Technologies Inc., Colt Technology Services Group Limited, CLAVISTER, AT&T Inc., Avast Software s.r.o., Check Point Software Technologies Ltd., ForgeRock Inc., Positive Technologies, Thales Group, Symantec Enterprise, McAfee Corp.

What You Receive

• Global 5g security market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of 5g security.

• 5g security market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• 5g security market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term 5g security market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the 5g security market, 5g security supply chain analysis.

• 5g security trade analysis, 5g security market price analysis, 5g security Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest 5g security market news and developments.

The 5g security Market international scenario is well established in the report with separate chapters on North America 5g security Market, Europe 5g security Market, Asia-Pacific 5g security Market, Middle East and Africa 5g security Market, and South and Central America 5g security Markets. These sections further fragment the regional 5g security market by type, application, end-user, and country.

FAQ's

The Global 5g security Market is estimated to generate USD 9.32 billion in revenue in 2025.

The Global 5g security Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 17.47% during the forecast period from 2025 to 2034.

The 5g security Market is estimated to reach USD 39.71 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!