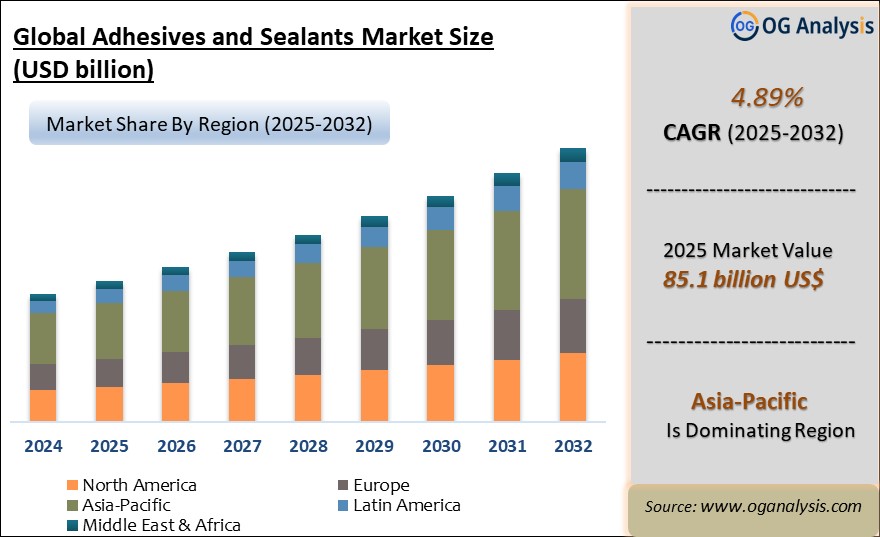

"The Adhesives and Sealants Market valued at $81.2 billion in 2024, is expected to grow by 4.89% CAGR to reach market size worth $133.7 billion by 2034."

The adhesives and sealants market is a critical component of various industries, providing essential solutions for bonding, sealing, and protecting materials across diverse applications. Adhesives and sealants are used to assemble, secure, and protect a wide range of products, from consumer goods and automotive components to construction materials and aerospace structures. The market has witnessed consistent growth over the years, driven by factors like technological advancements, increasing demand for durable and reliable bonding solutions, and growing focus on sustainability. In 2024, the adhesives and sealants market saw a surge in the development of innovative products with enhanced performance characteristics, including improved adhesion, faster curing times, and enhanced resistance to environmental factors. Furthermore, the industry saw a significant shift towards more sustainable and environmentally friendly adhesives and sealants, driven by a growing concern for reducing the environmental footprint of manufacturing and construction processes.

Looking ahead to 2025, the adhesives and sealants market is expected to continue its robust growth trajectory, fueled by the expanding global economy, increasing urbanization, and the growing demand for advanced materials and technologies. The automotive, construction, and aerospace industries are anticipated to remain key drivers, fueled by factors like technological advancements, infrastructure development, and a growing middle class in developing economies. Furthermore, the development of new and innovative adhesives and sealants, particularly those with improved performance, sustainability, and ease of use, is expected to drive market growth. The market is likely to witness intensified competition among existing players and new entrants, with a focus on innovation, cost optimization, and sustainability. The adhesives and sealants market is thus positioned for a period of robust growth, offering compelling opportunities for manufacturers and suppliers.

The Global Adhesives and Sealants Market Analysis Report will provide a comprehensive assessment of business dynamics, offering detailed insights into how companies can navigate the evolving landscape to maximize their market potential through 2034. This analysis will be crucial for stakeholders aiming to align with the latest industry trends and capitalize on emerging market opportunities.

Asia-Pacific is the leading region in the adhesives and sealants market, powered by rapid industrialization, robust growth in the construction and automotive sectors, and increasing demand for packaging and electronics applications across emerging economies.

Trade Intelligence for Adhesives and Sealants Market

| Global Glaziers putty, resin cements, caulking compounds, mastics Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 6,288 | 7,692 | 8,242 | 8,269 | 8,534 |

| Germany | 437 | 525 | 533 | 561 | 572 |

| China | 509 | 618 | 578 | 517 | 561 |

| United States of America | 319 | 395 | 516 | 459 | 501 |

| France | 237 | 325 | 360 | 398 | 413 |

| Canada | 261 | 314 | 377 | 384 | 371 |

| Source: OGAnalysis | |||||

- Germany, United States of America, Belgium, China and France are the top five countries importing 51.6% of global Glaziers putty, resin cements, caulking compounds, mastics in 2024

- Global Glaziers putty, resin cements, caulking compounds, mastics Imports increased by 34.3% between 2020 and 2024

- Germany accounts for 20.7% of global Glaziers putty, resin cements, caulking compounds, mastics trade in 2024

- United States of America accounts for 10.8% of global Glaziers putty, resin cements, caulking compounds, mastics trade in 2024

- Belgium accounts for 9.4% of global Glaziers putty, resin cements, caulking compounds, mastics trade in 2024

| Global Glaziers putty, resin cements, caulking compounds, mastics Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

Key Insights

- Adhesives and sealants historically gained share by enabling design freedom and weight reduction compared with mechanical joining, particularly in transportation and consumer goods. This legacy continues as engineers seek to join dissimilar materials and optimize structures for performance and aesthetics.

- Construction and infrastructure remain foundational end-use sectors, where sealants and construction adhesives support weatherproofing, structural glazing, flooring, roofing, and façade systems. Rising expectations for energy-efficient, airtight buildings keep demand resilient throughout both new-build and renovation cycles.

- Automotive and transportation markets rely on structural adhesives, body-in-white bonding, glass bonding, and seam sealants to improve crash performance, reduce noise, and lower weight. The transition toward electrified and connected vehicles further expands use in battery systems, electronics encapsulation, and thermal management assemblies.

- Packaging applications, especially in flexible packaging and labelling, remain a key volume driver for adhesives. Hot melts, water-based systems, and specialty laminating adhesives enable lightweight, high-speed packaging formats while supporting requirements for shelf life, printability, and consumer convenience.

- Electronics and electrical applications are growing in importance, with adhesives and sealants increasingly used for die attach, underfill, potting, conformal coating, and thermal interface management. These materials protect sensitive components from moisture, vibration, and thermal stress in compact, densely packed devices.

- Technology trends favour reactive and hybrid chemistries such as polyurethane, silyl-modified polymers, and epoxy-based systems that deliver strong bonds, flexibility, and improved durability. These formulations often replace solvent-based products and offer better balance between mechanical performance, processability, and environmental profile.

- Sustainability and regulatory pressures are accelerating the shift toward low-VOC, solvent-free, and reduced-hazard products. Producers are reformulating portfolios with water-based systems, higher solids, and alternative raw materials, while also supporting customers in meeting evolving building, automotive, and environmental standards.

- Process integration and automation are critical differentiators, as manufacturers look to shorten cycle times and improve consistency. Adhesive and sealant suppliers increasingly provide rheology-tailored products, cure-on-demand technologies, and application know-how that align with robotic dispensing, high-speed lines, and digital quality control.

- Specialty and niche applications, such as medical devices, aerospace, renewable energy, and high-performance sports equipment, are expanding the value mix of the market. These segments demand highly engineered formulations with specific biocompatibility, flame-retardancy, or extreme-environment performance attributes.

- Looking ahead, the adhesives and sealants market is expected to benefit from megatrends such as urbanization, lightweighting, electrification, modular construction, and circular design. Companies that combine broad chemistry capabilities with strong application support, regulatory expertise, and sustainability roadmaps will be best positioned to capture long-term growth opportunities.

Global cement production (million tonnes), 2018–2024

Figure: Global cement production (million tonnes), 2018–2024e, indicating sustained construction and infrastructure activity that underpins demand for construction adhesives and sealants.

- Global cement production remained above 4 billion tonnes through 2018–2024e, reflecting sustained construction and infrastructure activity worldwide—the largest demand center for structural adhesives, construction sealants, waterproofing systems and glazing compounds. This steady upstream indicator highlights the strong substrate base of concrete, masonry and prefabricated elements that rely on high-performance bonding and sealing solutions, reinforcing the robust long-term growth outlook for the Adhesives and Sealants Market.

Regional Insights

North America Adhesives and Sealants Market Analysis

The North America Adhesives and Sealants market demonstrated robust growth in 2024, driven by advancements in eco-friendly materials, regulatory shifts favoring sustainable production, and increased investments in R&D. Chemicals and Materials markets such as bio-based polymers, adhesives and sealants, and paints and coatings additives saw significant traction, spurred by strong demand from construction, automotive, and packaging sectors. The anticipated Adhesives and Sealants industry growth in 2025 is underpinned by heightened focus on green building materials, innovative self-healing materials, and expansion of end-user industries such as electronics and aerospace. Competitive dynamics reflect increasing collaboration between key players and technology providers, with a focus on sustainable innovation and scaling advanced manufacturing technologies. Major players are leveraging partnerships and acquisitions to address regulatory standards and expand their market presence, creating an intensely competitive landscape.

Europe Adhesives and Sealants Market Outlook

The European Adhesives and Sealants market maintained a steady growth trajectory in 2024, bolstered by stringent environmental regulations and the growing adoption of circular economy principles. High demand for specialty chemicals and bio-based polymers was observed due to infrastructure projects and the push for green building initiatives. From 2025 onward, growth is expected to accelerate with innovations in materials catering to advanced applications in pharmaceuticals, cosmetics, and industrial coatings. The region’s leadership in sustainable technologies and commitment to reducing carbon footprints are key driving factors. The competitive landscape is characterized by well-established global leaders and emerging regional players focusing on localized manufacturing and energy-efficient solutions, creating a diverse and evolving market.

Asia-Pacific Adhesives and Sealants Market Forecast

Asia-Pacific’s Adhesives and Sealants market experienced dynamic growth in 2024, fueled by industrialization, urbanization, and increasing investments in construction, automotive, and consumer goods. Overall, the chemicals and Materials segment saw exponential demand due to infrastructure projects and expanding manufacturing bases. Anticipated growth from 2025 is supported by government initiatives promoting domestic production and green manufacturing. Its competitive production costs and technological advancements drive the region's dominance in key end-use markets. The competitive landscape is highly fragmented, with local manufacturers scaling operations to meet global export demands while international players continue to expand their footprints through joint ventures and acquisitions.

Middle East, Africa, Latin America Adhesives and Sealants Market Overview

The Adhesives and Sealants market across the Rest of the World, encompassing Latin America, the Middle East, and Africa, showed promising growth in 2024. This growth was supported by rising investments in the construction and energy sectors, driven by increasing oil and gas exploration and infrastructure development. From 2025, anticipated growth will stem from industrial diversification efforts, especially in GCC countries, and the adoption of high-performance materials like potassium sorbate and self-healing materials in emerging industries. The competitive landscape is evolving as regional players strengthen production capabilities and international players capitalize on untapped markets through strategic partnerships.

Adhesives and Sealants Market Dynamics and Future Analytics

The research analyses the Adhesives and Sealants parent market, derived market, intermediaries’ market, raw material market, and substitute market are all evaluated to better prospect the Adhesives and Sealants market outlook. Geopolitical analysis, demographic analysis, and Porter’s five forces analysis are prudently assessed to estimate the best Adhesives and Sealants market projections.

Recent deals and developments are considered for their potential impact on Adhesives and Sealants's future business. Other metrics analyzed include the Threat of New Entrants, Threat of New Substitutes, Product Differentiation, Degree of Competition, Number of Suppliers, Distribution Channel, Capital Needed, Entry Barriers, Govt. Regulations, Beneficial Alternative, and Cost of Substitute in Adhesives and Sealants market.

Adhesives and Sealants trade and price analysis helps comprehend Adhesives and Sealants's international market scenario with top exporters/suppliers and top importers/customer information. The data and analysis assist our clients in planning procurement, identifying potential vendors/clients to associate with, understanding Adhesives and Sealants price trends and patterns, and exploring new Adhesives and Sealants sales channels. The research will be updated to the latest month to include the impact of the latest developments such as the Russia-Ukraine war on the Adhesives and Sealants market.

Adhesives and Sealants Market Structure, Competitive Intelligence and Key Winning Strategies

The report presents detailed profiles of top companies operating in the Adhesives and Sealants market and players serving the Adhesives and Sealants value chain along with their strategies for the near, medium, and long term period.

OGAnalysis’ proprietary company revenue and product analysis model unveils the Adhesives and Sealants market structure and competitive landscape. Company profiles of key players with a business description, product portfolio, SWOT analysis, Financial Analysis, and key strategies are covered in the report. It identifies top-performing Adhesives and Sealants products in global and regional markets. New Product Launches, Investment & Funding updates, Mergers & Acquisitions, Collaboration & Partnership, Awards and Agreements, Expansion, and other developments give our clients the Adhesives and Sealants market update to stay ahead of the competition.

Company offerings in different segments across Asia-Pacific, Europe, the Middle East, Africa, and South and Central America are presented to better understand the company strategy for the Adhesives and Sealants market. The competition analysis enables users to assess competitor strategies and helps align their capabilities and resources for future growth prospects to improve their market share.

Report Scope

| Parameter | Adhesives and Sealants Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Diagnostic Method, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Segmentation

By Technology

- Water Based

- Solvent Based

- Hot Melt

- Reactive

- Others

By Product

- Acrylic

- PVA

- Polyurethanes

- Styrenic block

- Epoxy

- EVA

- Others

By Application

- Paper & packaging

- Consumer & DIY

- Building & construction

- Furniture & woodworking

- Footwear & leather

- Automotive & transportation

- Medical

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

-

Ashland Inc.

-

Avery Denison Corporation

-

H B Fuller

-

Henkel AG

-

Sika AG

-

Pidilite Industries

-

Huntsman

-

Wacker Chemie AG

-

RPM International Inc.

-

Dow

-

Kuraray Co., Ltd.

Recent Developments

-

Feb 2026 – Henkel: Agreed to acquire Stahl, a specialty coatings leader, strengthening Henkel’s Adhesive Technologies business and expanding its reach in high-value industrial substrate solutions. The deal supports portfolio premiumization and broader customer coverage in engineered bonding ecosystems.

-

Jan 2026 – U.S. FTC / Henkel: The U.S. FTC filed a lawsuit to block Henkel’s proposed acquisition of Liquid Nails, citing competition concerns in construction adhesives. The action highlights intensifying regulatory scrutiny around consolidation in key adhesive categories.

-

Jun 2025 – Sika: Announced strategic manufacturing investments across China, Brazil, and Morocco to expand local production capacity and improve responsiveness. The program supports growth in construction sealants, waterproofing, and industrial bonding demand.

-

May 2024 – H.B. Fuller: Acquired ND Industries, adding threadlockers, sealing solutions, and specialty adhesive technologies. The move broadens H.B. Fuller’s engineered adhesives portfolio for industrial fastening, assembly, and maintenance applications.

-

Dec 2024 – H.B. Fuller: Announced acquisitions in medical adhesive technologies (Medifill and a provisional agreement for GEM), expanding its specialty portfolio. The deals reinforce ongoing shift toward higher-margin, regulated end markets that demand advanced bonding performance.

FAQ's

The Global Adhesives and Sealants Market is estimated to generate USD 84.3 billion in revenue in 2025

The Global Adhesives and Sealants Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.89% during the forecast period from 2025 to 2034.

The Adhesives and Sealants Market is estimated to reach USD 133.7 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!