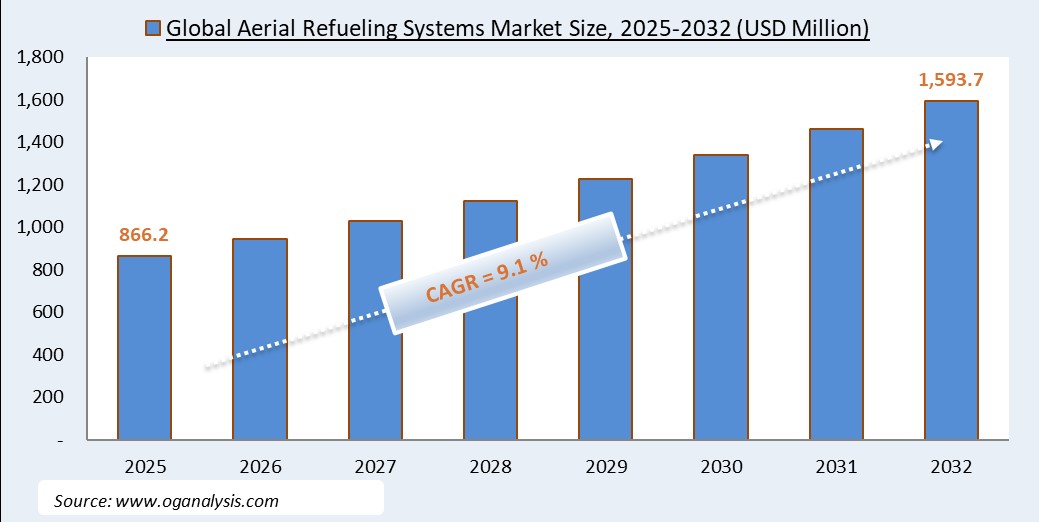

"The Global Aerial Refueling Systems Market is valued at USD 866.25 Million in 2025. Worldwide sales of Aerial Refueling Systems Market are expected to grow at a significant CAGR of 9.1%, reaching USD 1593.74 Million by the end of the forecast period in 2032."

Aerial Refueling Systems Market Overview

The aerial refueling systems market plays a crucial role in modern military and defense operations, enabling extended flight endurance and operational range for aircraft. Aerial refueling, also known as air-to-air refueling (AAR), is a critical capability for air forces worldwide, allowing aircraft to stay airborne longer, conduct extended missions, and reduce the need for ground refueling stops. The market encompasses various refueling systems, including probe-and-drogue, boom refueling, and autonomous refueling technologies. As geopolitical tensions rise and defense budgets increase, countries are investing heavily in upgrading their aerial refueling capabilities to enhance their air force’s operational readiness. The demand for tanker aircraft, advanced refueling pods, and automated refueling systems has surged, particularly in the U.S., Europe, and Asia-Pacific. Technological advancements, such as smart refueling systems with real-time data integration and enhanced fuel efficiency, are also shaping the market landscape. Furthermore, commercial applications, including aerial refueling for unmanned aerial vehicles (UAVs), are gaining traction, expanding the scope of the market beyond military operations.

In 2024, the aerial refueling systems market has witnessed significant developments driven by increased defense spending and modernization programs across major military forces. Several countries have ramped up procurement of next-generation tanker aircraft, with a focus on enhancing fuel transfer efficiency and operational flexibility. The integration of advanced automation technologies, such as AI-driven fuel management and automated refueling booms, has improved safety and precision in refueling operations. Additionally, multinational defense collaborations have fueled market expansion, with joint development programs and strategic alliances driving innovation. The growing demand for multi-role tanker transport aircraft, which offer both refueling and cargo transport capabilities, has further shaped industry trends. In the commercial aviation sector, interest in UAV refueling systems has intensified, with research initiatives exploring autonomous aerial refueling for long-endurance drones. However, supply chain constraints and regulatory challenges have posed hurdles, affecting the timely delivery of new tanker aircraft and refueling components. Despite these challenges, the market remains resilient, with strong demand from both established and emerging military forces.

Looking ahead to 2025 and beyond, the aerial refueling systems market is expected to undergo rapid evolution with the introduction of next-generation autonomous refueling technologies. AI-powered refueling drones, enhanced sensor integration, and real-time communication networks will transform how aerial refueling operations are conducted. The development of fully autonomous refueling pods, capable of adjusting fuel transfer rates dynamically based on aircraft needs, is anticipated to enhance operational efficiency. Furthermore, hybrid-electric and sustainable aviation fuel (SAF) initiatives will influence the market as governments push for greener defense solutions. The growing role of space-based surveillance and long-range strike capabilities will drive further investments in aerial refueling infrastructure to support extended missions. In addition, regional defense partnerships in Asia-Pacific, the Middle East, and NATO countries will boost the market as nations collaborate on shared tanker programs. The industry is also expected to see advancements in 3D printing and lightweight materials for refueling components, reducing operational costs and improving performance. With continued technological advancements and strategic investments, the aerial refueling systems market is poised for sustained growth, shaping the future of air combat and strategic mobility.

Market Segmentation

- By Refueling System Type:

- Probe-and-Drogue

- Flying Boom

- Autonomous Refueling

- By Component:

- Refueling Pods

- Fuel Tanks

- Hoses

- Booms

- Valves

- Nozzles

- By Aircraft Type:

- Tanker Aircraft

- Receiver Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Combat Aircraft

- Transport Aircraft

- By End-User:

- Military

- Commercial Aviation

- Unmanned Systems

- By Geography:

- North America (U.S., Canada, Mexico)

- Europe (Germany, U.K., France, Italy, Spain, Rest of Europe)

- Asia-Pacific (China, India, Japan, South Korea, ASEAN, Rest of Asia-Pacific)

- Latin America (Brazil, Argentina, Rest of Latin America)

- Middle East & Africa (GCC, South Africa, Rest of MEA)

Major Players in the Aerial Refueling Systems Market

- Boeing

- Lockheed Martin Corporation

- Airbus SE

- Northrop Grumman Corporation

- Embraer S.A.

- General Dynamics Corporation

- Draken International

- Eaton Corporation

- GE Aviation

- Cobham Limited

- BAE Systems plc

- Parker Hannifin Corporation

- Marshall Aerospace and Defence Group

- Safran S.A.

- L3Harris Technologies, Inc.

FAQ's

The Global Aerial Refueling Systems Market is estimated to generate USD 866.25 Million revenue in 2025.

The Global Aerial Refueling Systems Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.1% during the forecast period from 2025 to 2032.

By 2032, the Aerial Refueling Systems Market is estimated to account for USD 1593.74 Million.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!