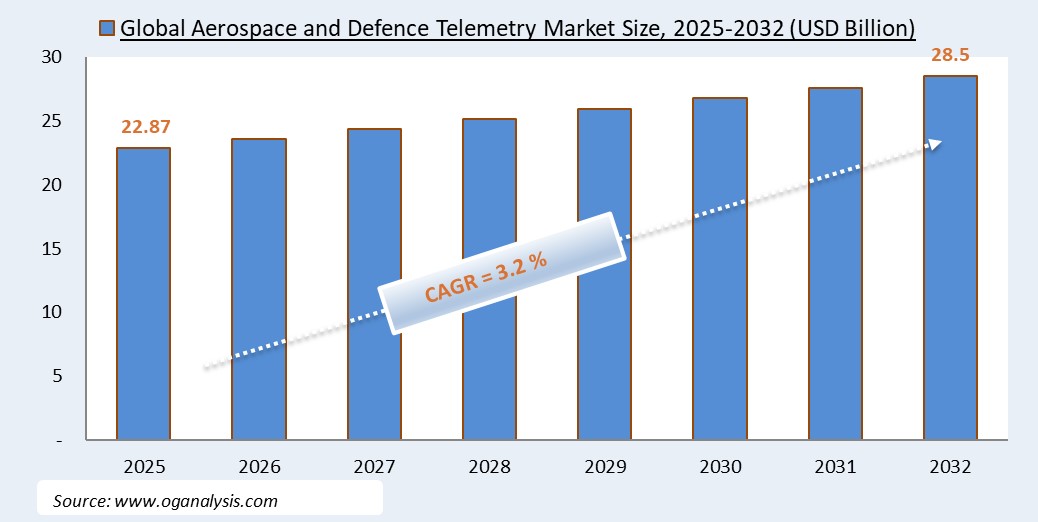

"The Global Aerospace and Defence Telemetry Market is valued at USD 22.87 Billion in 2025. Worldwide sales of Aerospace and Defence Telemetry Market are expected to grow at a significant CAGR of 3.2%, reaching USD 28.51 Billion by the end of the forecast period in 2032."

The Aerospace and Defence Telemetry Market is experiencing significant expansion as the demand for real-time data acquisition and analysis continues to grow across military, space, and aviation sectors. Telemetry systems collect, transmit, and analyze vital information from airborne, ground, and naval platforms to monitor performance, environmental parameters, and system health. This data is critical during missile tests, live-fly exercises, spacecraft launches, and fighter jet operations to ensure mission success and safety. Market drivers include increased defense budgets, advancements in satellite and UAV technologies, integration of IoT and AI in aerospace systems, and the shift towards digital twin models in aircraft development. Telemetry enhances situational awareness, predictive maintenance, and in-flight diagnostics, empowering operators with actionable insights and improving mission reliability, operational readiness, and cost-efficiency.

Major aerospace and defense contractors, telemetry equipment manufacturers, and system integrators are investing in high-bandwidth RF, satellite communication, software-defined radios, secure data links, and cloud-based ground stations. North America leads due to substantial defense R&D spending and space exploration initiatives, while Asia Pacific is witnessing rapid growth owing to new satellite programmes, military modernisation, and UAV deployments. The competitive landscape features partnerships between technology providers and government agencies to develop encrypted, IP-based telemetry systems with enhanced data security and bandwidth. However, challenges include spectrum congestion, cybersecurity threats, and high deployment costs. Looking ahead, market growth is projected through miniaturisation of telemetry units, adoption of advanced modulation techniques, integration with AI analytics, and expansion of satellite-based telemetry services for global low-latency coverage.

By Technology, the largest segment is Wireless Telemetry. This is because wireless telemetry offers flexible, real-time data transmission from airborne, naval, and ground-based platforms without the limitations of physical cabling, enabling its widespread adoption in aircraft flight tests, UAV operations, and missile telemetry for reliable, high-speed data acquisition.

By Application, the fastest-growing segment is Unmanned Aerial Vehicles (UAVs). The rapid growth is driven by increasing military and commercial UAV deployments globally, requiring advanced telemetry systems for real-time flight control, payload data transmission, surveillance, and mission-critical diagnostics to ensure safe and efficient operations.

Key Insights

- The aerospace and defence telemetry market is expanding due to growing demand for real-time data from flight tests, UAVs, missile systems, and space missions, enabling monitoring of critical parameters like engine performance, structural integrity, and environmental conditions.

- High-data-rate RF and IP-based telemetry systems dominate segment share by offering secure, low-latency, and reliable links for transmitting video, sensor, and diagnostic data from high-altitude and supersonic platforms.

- Satellite telemetry services are gaining momentum, especially in space launches and UAS beyond line-of-sight missions, to ensure continuous, global data connectivity across vast and remote operational areas.

- North America leads due to substantial defense R&D, private space projects, and established aerospace infrastructure, while Asia Pacific shows fastest growth driven by new satellite launches, UAV modernisation, and regional defence upgrades.

- Telemetry unit miniaturisation and weight reduction are key trends, facilitating integration in small UAVs, microsatellites, and guided munitions without compromising data throughput or mission flexibility.

- AI-driven analytics and predictive diagnostics are enabling telemetry systems to process complex datasets onboard or at ground stations, delivering actionable insights such as failure prediction and performance optimisation.

- Defense modernization programs are driving demand for secure, encrypted telemetry solutions that ensure data integrity and protection from cyber threats during live exercises and operational missions.

- Software-defined radios and agile SDR-based telemetry platforms are being adopted for frequency flexibility and interoperability across global military and commercial aerospace systems.

- Collaborations between telemetry OEMs, space agencies, and integrators are increasing, fostering joint development of next-gen systems supporting multi-mission flexibility, satellite control, and UAV swarm telemetry.

- Future market growth is expected through deployment of multi-band, high-throughput telemetry links, enhanced AI-based onboard processing, and satellite telemetry expansion to meet global low-latency communication needs.

Reort Scope

| Parameter | Detail |

|---|---|

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Component, By Technology, By Application, By End User |

| Countries Covered | North America (USA, Canada, Mexico) Europe (Germany, UK, France, Spain, Italy, Rest of Europe) Asia-Pacific (China, India, Japan, Australia, Rest of APAC) The Middle East and Africa (Middle East, Africa) South and Central America (Brazil, Argentina, Rest of SCA) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10 % free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Datafile |

What You Receive

• Global Aerospace And Defence Telemetry market size and growth projections (CAGR), 2024- 2034• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Aerospace And Defence Telemetry.

• Aerospace And Defence Telemetry market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Aerospace And Defence Telemetry market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Aerospace And Defence Telemetry market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Aerospace And Defence Telemetry market, Aerospace And Defence Telemetry supply chain analysis.

• Aerospace And Defence Telemetry trade analysis, Aerospace And Defence Telemetry market price analysis, Aerospace And Defence Telemetry Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Aerospace And Defence Telemetry market news and developments.

The Aerospace And Defence Telemetry Market international scenario is well established in the report with separate chapters on North America Aerospace And Defence Telemetry Market, Europe Aerospace And Defence Telemetry Market, Asia-Pacific Aerospace And Defence Telemetry Market, Middle East and Africa Aerospace And Defence Telemetry Market, and South and Central America Aerospace And Defence Telemetry Markets. These sections further fragment the regional Aerospace And Defence Telemetry market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways1. The report provides 2024 Aerospace And Defence Telemetry market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Aerospace And Defence Telemetry market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Aerospace And Defence Telemetry market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Aerospace And Defence Telemetry business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Aerospace And Defence Telemetry Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Aerospace And Defence Telemetry Pricing and Margins Across the Supply Chain, Aerospace And Defence Telemetry Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Aerospace And Defence Telemetry market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

FAQ's

The Global Aerospace and Defence Telemetry Market is estimated to generate USD 22.87 Billion revenue in 2025.

The Global Aerospace and Defence Telemetry Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 3.2% during the forecast period from 2025 to 2032.

By 2032, the Aerospace and Defence Telemetry Market is estimated to account for USD 28.51 Billion.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!