"The Aerospace Fluid Conveyance Systems Market was valued at $ 4.68 billion in 2026 and is projected to reach $ 11.19 billion by 2034, growing at a CAGR of 11.5%."

The Aerospace Fluid Conveyance Systems Market is a critical segment of the aerospace components and systems industry, driven by the need for safe, lightweight, reliable, and high-performance movement of fluids across aircraft, spacecraft, defense platforms, and propulsion systems. Aerospace fluid conveyance systems include hoses, tubes, ducts, couplings, fittings, manifolds, seals, valves, rigid and flexible assemblies, and integrated distribution systems used to transport fuel, hydraulic fluids, lubricants, coolant, air, oxygen, water, wastewater, and other mission-critical fluids. These systems are used across commercial aircraft, regional jets, business aircraft, military aircraft, helicopters, unmanned aerial vehicles, satellites, launch vehicles, and space exploration platforms. Demand is supported by aircraft production, fleet modernization, rising defense aviation programs, engine efficiency improvements, electrification of aircraft systems, and the need for lighter and more durable fluid transfer solutions.

The competitive landscape of the Aerospace Fluid Conveyance Systems Market includes aerospace component manufacturers, hose and tubing suppliers, precision fitting companies, fluid control system providers, engine component suppliers, defense contractors, MRO service providers, and material technology companies. Companies compete through weight reduction, pressure resistance, temperature performance, vibration durability, corrosion resistance, leak prevention, certification compliance, system integration capability, and long lifecycle reliability. Latest trends include lightweight titanium and composite tubing, flexible high-pressure hose assemblies, advanced thermal management fluid systems, electric aircraft cooling loops, improved quick-disconnect couplings, additive-manufactured manifolds, and fluid conveyance systems designed for sustainable aviation fuel compatibility. Growth is driven by commercial aircraft deliveries, aging fleet replacement, rising MRO activity, defense modernization, space launch demand, and increasing fluid system complexity in next-generation aircraft. However, challenges include strict certification requirements, material cost pressure, long qualification cycles, supply-chain constraints, and the need to meet extreme performance standards. The outlook remains positive as aerospace platforms continue evolving toward lighter, safer, more efficient, and more integrated fluid management architectures.

Key Insights

- Commercial aircraft production remains one of the strongest demand drivers for aerospace fluid conveyance systems, as every aircraft requires extensive hydraulic, fuel, lubrication, potable water, environmental control, and cooling fluid pathways. New aircraft platforms increasingly require lighter and more compact assemblies that improve fuel efficiency and reduce maintenance burden. Suppliers capable of meeting aircraft OEM specifications and production schedules are well positioned.

- Hydraulic systems continue to represent a major application area because flight controls, landing gear, brakes, actuation systems, and other aircraft functions depend on reliable high-pressure fluid transfer. Aerospace hydraulic conveyance components must withstand pressure cycling, vibration, temperature variation, and long service intervals. This creates steady demand for certified hoses, tubes, fittings, couplings, and seals.

- Fuel conveyance systems are becoming more technically demanding as aircraft designs focus on efficiency, safety, and compatibility with evolving fuel types. Fuel lines, connectors, pumps, valves, and transfer assemblies must prevent leaks, resist corrosion, and maintain performance under changing thermal and pressure conditions. Sustainable aviation fuel adoption is increasing the importance of material compatibility and validation.

- Thermal management is creating new opportunities as aircraft electronics, avionics, batteries, electric propulsion systems, and high-power components require efficient cooling. Fluid conveyance systems used for coolant circulation are becoming more important in hybrid-electric aircraft, advanced avionics bays, and defense electronics. This trend supports demand for leak-tight, lightweight, and thermally stable fluid routing solutions.

- Defense aviation remains a significant market segment because military aircraft, helicopters, UAVs, and mission systems operate in harsh environments and require highly durable fluid conveyance components. These platforms demand resistance to vibration, shock, temperature extremes, chemicals, and contamination. Suppliers with defense-grade engineering and long-term program support capabilities can capture high-value opportunities.

- Space and launch vehicle applications are expanding demand for specialized fluid conveyance systems used in propulsion, cryogenic fuel transfer, thermal control, pressurization, and life-support systems. These applications require extreme reliability, low leakage, lightweight construction, and compatibility with demanding fluids and operating conditions. Space commercialization is broadening the customer base for advanced conveyance technologies.

- Lightweight materials are a major innovation focus because reducing aircraft weight directly supports fuel efficiency, payload capability, and emissions reduction. Titanium, aluminum alloys, composites, advanced polymers, and optimized hose constructions are being adopted to replace heavier legacy components. Material selection must balance weight savings with strength, durability, fire resistance, and certification requirements.

- MRO and aftermarket demand is important because fluid conveyance components require inspection, replacement, repair, and lifecycle management due to wear, fatigue, corrosion, and seal degradation. Airlines, defense operators, and MRO providers rely on dependable replacement parts to maintain aircraft safety and availability. Aftermarket support, documentation, and global service networks are key competitive factors.

- Certification and qualification requirements create high entry barriers in the market, as aerospace fluid conveyance systems must meet strict safety, performance, material, fire, pressure, and environmental standards. Product validation can require extensive testing and long approval timelines. Established suppliers with proven quality systems and OEM relationships hold a competitive advantage.

- Competition is shifting toward integrated fluid management solutions that combine hoses, tubes, fittings, couplings, valves, manifolds, sensors, and system-level engineering support. Aerospace customers increasingly prefer suppliers that can reduce complexity, improve installation efficiency, support platform-specific design, and deliver long-term reliability. Companies offering lightweight, certified, and application-specific solutions are expected to remain strongly positioned.

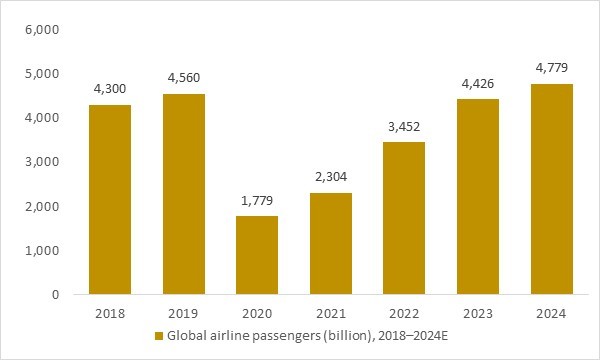

Global airline passengers (billion), 2018–2024E

Figure: Global airline passenger traffic fell sharply in 2020 and then rebounded above pre-disruption levels by 2023, with further growth expected in 2024. This trend underpins rising aircraft utilisation, new narrowbody and widebody deliveries, and higher MRO activity, all of which drive demand for advanced aerospace fluid conveyance systems and airport radiation detection and security solutions.

- Global airline passenger traffic collapsed in 2020 but recovered to more than 4.4 billion passengers by 2023, with further growth expected in 2024. This rebound underpins renewed demand for aerospace fluid conveyance systems in new aircraft and MRO, while also driving higher investment in airport radiation detection and security screening infrastructure worldwide.

Regional Analysis

North America Aerospace Fluid Conveyance Systems Market

North America Aerospace Fluid Conveyance Systems Market is driven by strong commercial aircraft production, defense aviation programs, space launch activity, aircraft MRO demand, and advanced aerospace component manufacturing. Market dynamics are shaped by the presence of major aircraft OEMs, engine manufacturers, defense contractors, space companies, and certified aerospace suppliers requiring high-performance hoses, tubes, ducts, fittings, couplings, manifolds, and fluid control assemblies. Lucrative opportunities exist for suppliers offering lightweight titanium tubing, flexible hose assemblies, thermal management fluid systems, fuel conveyance solutions, hydraulic lines, and sustainable aviation fuel-compatible components. Latest trends include lightweight material adoption, additive-manufactured manifolds, electric aircraft cooling loops, advanced quick-disconnect couplings, and integrated fluid management systems. The forecast outlook remains favorable as aircraft production, fleet upgrades, defense modernization, and space exploration programs continue supporting demand for safe, certified, and reliable fluid conveyance technologies.

Asia Pacific Aerospace Fluid Conveyance Systems Market

Asia Pacific Aerospace Fluid Conveyance Systems Market is expanding due to rising aircraft deliveries, airline fleet growth, regional aviation expansion, defense aircraft procurement, MRO development, and increasing aerospace manufacturing localization. Market dynamics are supported by strong demand from commercial airlines, aircraft component manufacturers, military aviation programs, and emerging space and UAV sectors across China, India, Japan, South Korea, and Southeast Asia. The region presents strong opportunities for aerospace tubing suppliers, hose assembly manufacturers, fluid control system providers, MRO firms, and local component partners capable of meeting global aerospace certification standards. Latest trends include localized aerospace supply chains, lightweight fluid routing systems, hydraulic and fuel system upgrades, thermal management solutions for advanced avionics, and increased use of high-reliability components in new aircraft platforms. The forecast remains positive as regional aviation demand, defense spending, and aircraft maintenance activity continue expanding.

Europe Aerospace Fluid Conveyance Systems Market

Europe Aerospace Fluid Conveyance Systems Market is shaped by strong commercial aerospace manufacturing, defense aviation, helicopter production, aircraft engine programs, space systems, and sustainability-focused aircraft innovation. Market dynamics are influenced by demand for lightweight, fuel-efficient, low-emission, and certified fluid transfer systems used in fuel, hydraulic, lubrication, coolant, environmental control, and thermal management applications. Lucrative opportunities exist for aerospace component suppliers, precision tube manufacturers, advanced material companies, coupling and fitting producers, and MRO providers supporting OEM and aftermarket requirements. Latest trends include sustainable aviation fuel compatibility, lightweight titanium and composite tubing, fluid systems for hybrid-electric aircraft, advanced thermal control loops, and high-performance conveyance assemblies for next-generation engines. The forecast outlook remains steady as European aerospace companies continue investing in aircraft efficiency, defense readiness, space technology, and long-life component reliability.

Middle East & Africa Aerospace Fluid Conveyance Systems Market

Middle East & Africa Aerospace Fluid Conveyance Systems Market is developing through airline fleet expansion, long-haul aviation growth, defense aircraft procurement, MRO investment, airport infrastructure development, and regional aerospace service capability building. Market dynamics vary across the region, with Gulf countries showing stronger demand from large airline fleets, premium aviation maintenance hubs, military aircraft programs, and business aviation, while African markets present opportunities through fleet renewal, regional connectivity, and aircraft maintenance modernization. Companies can benefit by offering certified replacement hoses, hydraulic assemblies, fuel system components, cooling lines, couplings, and maintenance support suited to harsh operating environments. Latest trends include expansion of aerospace MRO facilities, demand for lightweight replacement components, defense aircraft support programs, and improved aftermarket supply reliability. The forecast remains constructive as regional aviation networks, defense requirements, and aircraft maintenance ecosystems continue strengthening.

South & Central America Aerospace Fluid Conveyance Systems Market

South & Central America Aerospace Fluid Conveyance Systems Market is supported by regional aircraft operations, defense aviation, business jets, commercial fleet maintenance, helicopter usage, and aerospace manufacturing capabilities in selected markets. Market dynamics are shaped by demand for reliable fluid conveyance components in hydraulic systems, fuel lines, lubrication circuits, environmental control systems, and aftermarket replacement applications. Opportunities exist for certified component suppliers, MRO providers, hose and tubing manufacturers, aerospace distributors, and fluid system service companies offering cost-effective and compliant solutions for airlines, defense operators, and regional aircraft manufacturers. Latest trends include fleet maintenance optimization, replacement of aging fluid system components, lightweight materials for aircraft efficiency, and stronger demand for reliable spare parts supply. The forecast outlook remains positive as regional operators continue focusing on aircraft safety, maintenance efficiency, and modernization of aviation support infrastructure.

Market Scope

| Parameter | Aerospace Fluid Conveyance Systems Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Aircraft Type, By Material Type, By Application Type |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Aerospace Fluid Conveyance Systems Market Segmentation

By Product Type

- Hoses

- Low-Pressure Ducts

- High-Pressure Ducts

By Aircraft Type

- Commercial Aircraft

- Regional Aircraft

- Helicopter

- Other Aircraft Types

By Material Type

- Nickel And Alloys

- Titanium And Alloys

- Stainless Steel And Alloys

- Composites

- Other Material Types

By Application Type

- Fuel

- Air

- Hydraulic)

- By End User (General Aviation

- Civil Aviation

- Military Aircraft

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Analysed

General Electric Company, Lockheed Martin Corporation, AIM Industries Inc., Safran SA, Eaton Corporation PLC, TE Connectivity Ltd., SKF AB, Arconic Corporation, Precision Castparts Corp, TransDigm Group Incorporated, GKN Aerospace Services Limited, Crane Co, Smiths Group PLC, ITT Corporation, Woodward Inc., Stelia Aerospace, Triumph Group Inc., Senior PLC, Kaman Corporation, PFW Aerospace GmbH, Arrowhead Products Corporation, SEKISUI Aerospace Inc., Hutchinson S.A., Titeflex Corporation, Flexfab LLC, CFM S.r.l., Seginus Aerospace LLC, Amcraft Manufacturing Inc.

Recent Developments

- May 2026 - Collins Aerospace announced an investment to expand its Largo, Florida facility, supporting higher production capacity for advanced aerospace and defense systems. While the investment is not limited to fluid conveyance, it reflects broader aerospace supplier capacity expansion as aircraft systems become more complex and production demand rises.

- April 2026 - Safran Aircraft Engines announced a major forging capability upgrade at its Gennevilliers site to manufacture strategic parts for commercial and military aircraft engines. The investment supports next-generation engine production, supply-chain resilience, and advanced aerospace component manufacturing, which indirectly strengthens demand for associated fluid, thermal, and propulsion system components.

- March 2026 - Collins Aerospace completed the Clean Aviation HECATE project, achieving a technology readiness milestone for high-voltage electric power systems supporting future hybrid-electric aircraft. The development is relevant to aerospace fluid conveyance systems because more-electric and hybrid-electric platforms are increasing demand for advanced thermal management, cooling loops, and integrated system architectures.

- March 2026 - Safran Aircraft Engines launched the Clean Aviation TAKE OFF project with partners to advance open fan engine flight demonstration activity. The project supports future propulsion architectures, where lighter, more efficient thermal, fuel, lubrication, and fluid routing systems will remain critical to engine integration and performance.

- February 2026 - Japan Airlines and Safran signed a long-term Support By the Hour agreement covering Airbus A350 aircraft, bringing together multiple Safran companies under one support model. The agreement includes maintenance, component pooling, logistics, and data-driven service support, reinforcing aftermarket demand for reliable aircraft systems and replacement components.

- December 2025 - Senior plc secured a multi-year Airbus contract to design, qualify, and manufacture highly engineered aerospace standard parts for fluid conveyance applications. Initial production will support both single-aisle and twin-aisle commercial aircraft platforms, with deliveries beginning from Senior’s European facilities.

- November 2025 - Eaton joined the HYLENA hydrogen-electric propulsion research project led by Airbus and other European partners. The project is focused on hydrogen-powered electric propulsion and supports long-term demand for advanced aerospace systems capable of safely managing power, heat, and next-generation fuel architectures.

- October 2025 - Eaton extended its global exclusive distribution agreement with Satair for commercial aircraft fuel components and piece parts from Eaton’s Titchfield facility. The agreement supports aircraft operators with improved component availability, supply-chain efficiency, and aftermarket access for critical fuel-system products.

- September 2025 - Bell selected Eaton to design, develop, and certify the aerial refueling retractable probe for the MV-75 Future Long Range Assault Aircraft program. The award reinforces Eaton’s position in advanced fuel-transfer and mission-critical aerospace fluid system technologies for next-generation military platforms.

- June 2025 - Eaton signed an agreement to acquire Ultra PCS Limited to strengthen its position in aerospace markets. The acquisition broadens Eaton’s safety-critical aerospace systems portfolio and supports demand for integrated aircraft technologies across military and commercial platforms.

- April 2025 - Eaton appointed VSE Aviation as its first authorized aerospace service center in the Americas for repair and overhaul of hydraulic components used on large commercial transport and regional aircraft. The move supports localized MRO capacity and faster turnaround for hydraulic system components.

- April 2025 - Eaton appointed Air Support as its first aerospace authorized service center in Europe, the Middle East, and Africa for local repair and overhaul of engine fuel components. The development strengthens regional aftermarket support for fuel-system products and reduces repair lead times for airline and MRO customers.

FAQ's

The Aerospace Fluid Conveyance Systems Market is estimated to generate $ 4.68 billion in revenue in 2026.

The Aerospace Fluid Conveyance Systems Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 11.54% during the forecast period from 2026 to 2034.

The Aerospace Fluid Conveyance Systems Market is estimated to reach $ 11.19 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!