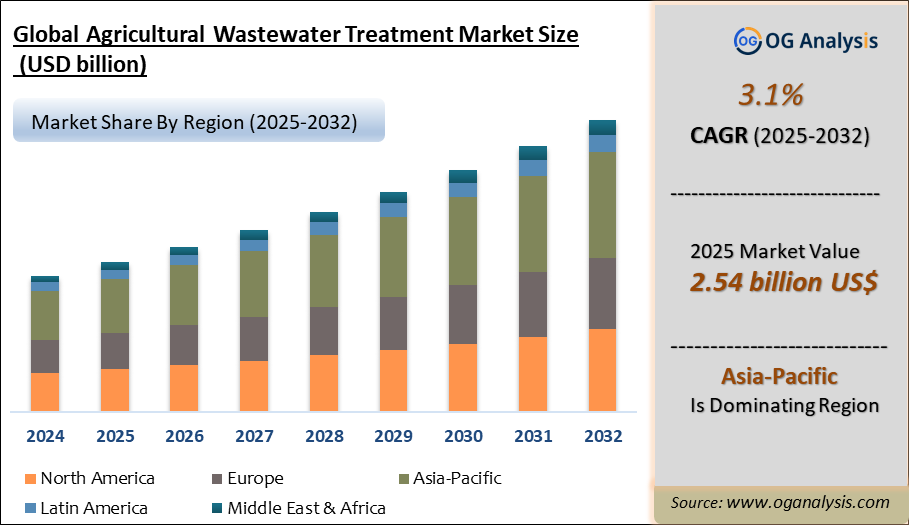

"The Global Agricultural Wastewater Treatment Market is valued at USD 2.47 billion in 2024. Worldwide sales of Agricultural Wastewater Treatment Market are expected to grow at a significant CAGR of 3.1%, reaching USD 3.16 billion by the end of the forecast period in 2032."

Introduction and Overview

The Agricultural Wastewater Treatment Market is experiencing significant growth due to the rising global awareness of environmental sustainability and the need for cleaner agricultural practices. Wastewater from agricultural activities, such as livestock operations, crop irrigation, and pesticide use, can contain harmful chemicals, nutrients, and pathogens. These contaminants, if left untreated, can cause severe damage to ecosystems and water supplies. As the agricultural industry continues to expand, there is an increasing demand for effective wastewater treatment technologies to address these concerns. This has led to the development of innovative solutions such as advanced filtration systems, biological treatment methods, and chemical treatments designed specifically to treat agricultural wastewater. The adoption of such technologies is essential to reduce the environmental impact of agricultural practices and ensure sustainable water use in the future.

Governments, particularly in emerging economies, are taking an active role in promoting regulations and policies to manage agricultural wastewater efficiently. These regulations are aimed at controlling water pollution, ensuring public health, and achieving sustainability in agricultural practices. As a result, agricultural businesses are increasingly adopting wastewater treatment solutions to comply with environmental regulations and safeguard the environment. The market is further supported by advancements in wastewater treatment technologies, including the use of artificial intelligence and machine learning to optimize treatment processes. These technologies help improve the efficiency of wastewater treatment and reduce costs for agricultural businesses. The combination of regulatory pressure, technological advancements, and a global push towards sustainability is driving the growth of the agricultural wastewater treatment market.

Asia-Pacific is the largest region in the agricultural wastewater treatment market, propelled by rapid agricultural expansion, increasing water scarcity, and stringent environmental regulations. Within this market, the biological treatment segment is the leading technology, fueled by its cost-effectiveness, environmental sustainability, and growing adoption among farmers to meet compliance and efficiency goals.

Latest Trends in the Agricultural Wastewater Treatment Market

One of the latest trends in the agricultural wastewater treatment market is the growing adoption of integrated treatment systems that combine multiple technologies to maximize efficiency and minimize environmental impact. These systems often integrate physical, chemical, and biological treatment processes to address the complex nature of agricultural wastewater. For example, many solutions now combine activated sludge systems with membrane filtration to provide higher levels of treatment and ensure that the treated water is safe for reuse in irrigation or livestock activities. Additionally, there is a rise in the adoption of decentralized wastewater treatment systems, particularly in rural and remote agricultural areas. These systems offer cost-effective, localized solutions for farmers and small agricultural businesses that may not have access to centralized treatment plants.

Another significant trend is the increasing focus on nutrient recovery from agricultural wastewater. Nutrient pollution, particularly nitrogen and phosphorus, is a major concern in agricultural wastewater. Innovations in nutrient recovery technologies allow the extraction of valuable nutrients from wastewater and their subsequent reuse as fertilizers. This trend aligns with the circular economy model, where waste materials are turned into resources, reducing the overall environmental footprint of agriculture. In addition to reducing pollution, nutrient recovery helps farmers lower input costs by reducing the need for synthetic fertilizers. This dual benefit of environmental sustainability and cost savings is contributing to the growing interest in nutrient recovery technologies in the agricultural wastewater treatment market.

Furthermore, there is a growing trend toward the use of digital technologies, such as artificial intelligence (AI) and the Internet of Things (IoT), in the agricultural wastewater treatment industry. These technologies enable real-time monitoring of wastewater quality, allowing farmers to optimize treatment processes and detect potential issues before they escalate. For instance, AI-powered systems can analyze large volumes of data from sensors placed within wastewater treatment systems, providing insights that help improve decision-making and efficiency. The integration of IoT devices in wastewater treatment facilities also allows for remote monitoring and management, offering cost-effective solutions for farmers and agricultural businesses with limited resources. This trend is expected to continue as digital technologies become increasingly integrated into agricultural operations worldwide.

Drivers of the Agricultural Wastewater Treatment Market

The increasing demand for water conservation and the reduction of water pollution are major drivers of the agricultural wastewater treatment market. With the growing global population and the corresponding rise in food production, the agricultural industry is using more water, which can put stress on local water resources. Wastewater treatment is essential to ensure that agricultural operations do not deplete available water supplies or contaminate the environment. Effective wastewater management also helps in the recycling of water for agricultural use, reducing the reliance on freshwater sources. As climate change continues to exacerbate water scarcity, the need for water-efficient agricultural practices will further propel the demand for wastewater treatment technologies.

Another key driver is the increasing regulatory pressure on agricultural practices. Governments and regulatory bodies worldwide are tightening their environmental regulations, especially concerning water quality and pollution control. Farmers and agricultural businesses are being compelled to adopt sustainable wastewater treatment solutions to comply with these regulations and avoid penalties. In some regions, failure to manage agricultural wastewater adequately can result in severe consequences, including fines and potential loss of access to water resources. As a result, agricultural producers are more inclined to invest in wastewater treatment systems to ensure compliance and reduce the risk of environmental damage. These regulations are accelerating market growth as more businesses seek to implement effective wastewater management solutions.

The growing emphasis on sustainable agricultural practices and corporate social responsibility (CSR) initiatives is also contributing to the market's expansion. Consumers are increasingly demanding food products that are produced sustainably and with minimal environmental impact. In response, many agricultural companies are adopting eco-friendly practices, including the treatment and reuse of wastewater. By implementing wastewater treatment systems, agricultural producers can reduce their environmental footprint and improve their reputation in the market. As sustainability becomes a key differentiator in the food and agriculture sector, the market for agricultural wastewater treatment technologies continues to grow, driven by the need for greener, more responsible farming practices.

Market Challenges in Agricultural Wastewater Treatment

Despite the promising growth, the agricultural wastewater treatment market faces several challenges that could hinder its expansion. One of the major challenges is the high initial investment required for advanced wastewater treatment technologies. Small and medium-sized agricultural enterprises, particularly those in developing regions, may find it difficult to afford the upfront costs of installing and maintaining such systems. The financial burden of purchasing sophisticated treatment equipment, as well as the ongoing operational and maintenance costs, can be a significant barrier to adoption. Additionally, the lack of technical expertise and trained personnel to operate complex wastewater treatment systems in rural areas poses another challenge. Without proper knowledge and skills, the effectiveness of these systems can be compromised, leading to inefficiencies and even failure in wastewater management. To overcome these challenges, governments and industry stakeholders must collaborate to provide financial incentives, subsidies, and training programs that enable wider adoption of agricultural wastewater treatment solutions. Nevertheless, these barriers must be addressed to ensure the continued growth of the market and its ability to meet the growing demand for sustainable agricultural practices.

Market Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By technology, By segment, By Application |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

By Technology

- Physical Solutions

- Chemical Solutions

- Biological Solutions

- By Pollutant Source

- Point Source

- Nonpoint Source

By Segment

- Chemicals

- Equipment

- Services

By Application

- Farming

- Soil Resources

- Groundwater Resources

- Other Applications

Key Market Players Presented in the Report Include

Evoqua Water Technologies LLC

Dow Water & Process Solutions Inc.

Veolia Environnement S. A.

Kurita Water Industries Ltd.

Pentair plc

Suez SA

Lindsay Corporation

IDE Technologies Ltd.

DuPont de Nemours Inc.

Jacobs Engineering Group Inc.

BASF SE

WSP Global Inc.

Grundfos Holding A/S

Dover Corporation

FAQ's

The Agricultural Wastewater Treatment Market is estimated to reach USD 3.16 Billion by 2032.

The Global Agricultural Wastewater Treatment Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 3.1% during the forecast period from 2025 to 2032.

The Global Agricultural Wastewater Treatment Market is estimated to generate USD 2.47 Billion in revenue in 2024.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!