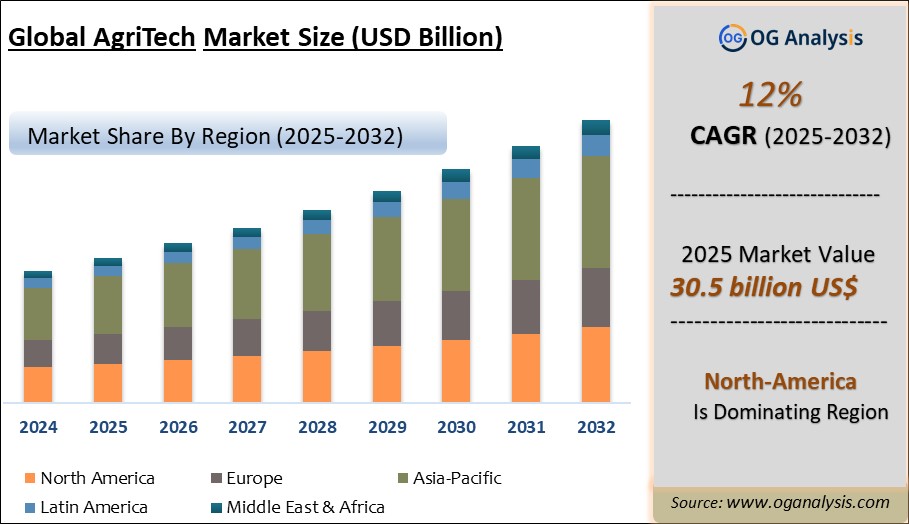

"The Agritech Market is valued at $ 34.16 billion in 2026. Further, the market is expected to grow at a CAGR of 12% to reach $ 84.58 billion by 2034."

The Agritech Market is undergoing rapid transformation as the agriculture industry adopts advanced technologies to improve productivity, sustainability, and profitability. Agritech—short for agricultural technology—encompasses a broad range of innovations including precision farming, IoT sensors, AI-driven analytics, drones, robotics, smart irrigation, and digital supply chains. The sector is responding to global challenges such as climate change, resource scarcity, and rising food demand, pushing farmers and agribusinesses to modernize operations. Increased investments, supportive government policies, and growing startup ecosystems are accelerating the adoption of digital tools and data-driven solutions. Agritech is empowering both smallholders and large-scale producers to maximize yields, optimize resource use, and reduce environmental impact, reshaping how food is grown, managed, and distributed.

As the market expands, companies are focusing on interoperability, connectivity, and user-friendly platforms to drive greater farmer participation. The integration of cloud computing, big data, and artificial intelligence is enabling real-time monitoring, predictive modeling, and precise decision-making at every stage of the crop cycle. Agritech is also fostering financial inclusion through agri-fintech solutions, expanding access to credit and insurance. Startups are leveraging remote sensing and automation to tackle labor shortages and increase operational efficiency. While adoption varies by region, the ongoing digital transformation is creating new revenue streams and business models, positioning agritech as a key enabler of food security and sustainable development for future generations.Big data and analytics is the fastest-growing segment in the agritech market, driven by the need for actionable insights to enhance farm productivity, resource allocation, and risk management. The ability to collect, process, and analyze vast amounts of agricultural data empowers growers to make data-driven decisions, optimize yields, and adapt quickly to changing environmental and market conditions.Production and maintenance is the largest application segment, as most agritech adoption focuses on improving crop management, machinery performance, and overall farm operations. Technologies that streamline planting, fertilization, pest control, and equipment upkeep deliver immediate value, making them essential for both smallholders and large-scale commercial farms seeking efficiency and profitability.

Key Insights

- Precision agriculture remains one of the strongest growth areas in the Agritech Market, as farmers increasingly use data to optimize seeding, irrigation, fertilization, spraying, and harvesting. GPS guidance, sensors, satellite imagery, and analytics platforms help reduce input waste and improve crop performance. This trend is especially important as growers face pressure to improve yields while managing rising costs and environmental expectations.

- Smart irrigation technologies are gaining strong attention because water scarcity and unpredictable rainfall are becoming major agricultural challenges. Sensor-based irrigation, automated valves, weather-linked scheduling, and remote monitoring help farmers apply water more efficiently. These solutions are particularly valuable in water-stressed regions where crop productivity depends on careful moisture management and reduced water loss.

- Agricultural drones are expanding across crop scouting, spraying, mapping, plant health assessment, and field monitoring applications. Drones help farmers identify stress, pest pressure, nutrient deficiency, and irrigation issues faster than manual inspection. Their value is increasing as image analytics and AI tools convert aerial data into practical farm-level recommendations.

- Farm management software is becoming a central digital tool for modern agriculture by helping farmers track field operations, input use, labor, machinery, crop performance, inventory, compliance, and profitability. These platforms support better planning and recordkeeping across farms of different sizes. Integration with sensors, drones, weather data, and equipment systems is improving their strategic value.

- Artificial intelligence is reshaping agritech by enabling predictive insights for disease risk, yield forecasting, pest detection, crop planning, price intelligence, and input optimization. AI-based advisory platforms can support faster decisions by analyzing weather, soil, crop, and market data. Adoption is rising as agribusinesses and farmers seek more accurate and localized recommendations.

- Robotics and autonomous equipment are gaining importance due to labor shortages, rising wages, and the need for repetitive task automation. Robotic systems are being developed for harvesting, weeding, planting, sorting, milking, feeding, and greenhouse operations. These technologies can improve consistency, reduce manual dependency, and support higher productivity in labor-intensive crops.

- Controlled-environment agriculture is creating opportunities for agritech providers serving greenhouses, vertical farms, hydroponics, and indoor cultivation systems. Automation, LED lighting, nutrient control, climate management, and data analytics help improve crop quality and production predictability. This segment is especially attractive for high-value vegetables, herbs, leafy greens, and urban food supply models.

- Livestock technology is expanding through animal health monitoring, smart collars, automated feeding, herd management software, milking automation, traceability systems, and disease detection tools. These solutions help farmers improve productivity, animal welfare, breeding efficiency, and operational control. Demand is increasing as livestock producers seek more data-driven and preventive management practices.

- Sustainability and climate-smart agriculture are becoming major drivers for agritech adoption. Tools supporting soil health, carbon measurement, regenerative practices, emissions tracking, fertilizer optimization, and climate risk assessment are gaining market relevance. Food companies, retailers, and investors are increasingly encouraging digital tools that demonstrate sustainable sourcing and environmental performance.

- Market success increasingly depends on affordability, usability, local adaptation, and measurable farmer value. Many agritech solutions fail when they are too complex, expensive, or disconnected from real farming conditions. Companies that combine technology with agronomic support, financing models, local partnerships, and clear return-on-investment evidence are expected to achieve stronger adoption.

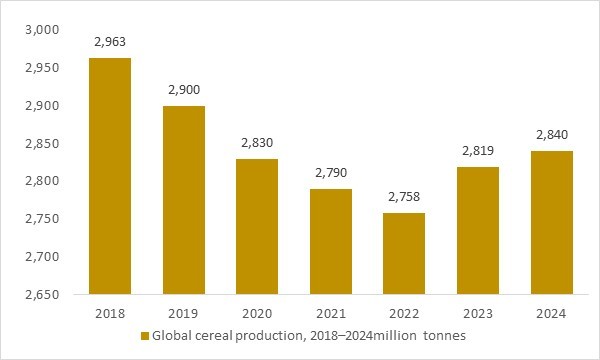

Global cereal production, 2018–2024 million tonnes

Figure: Global cereal production remained in the high 2.7–3.0 million tonne range between 2018 and 2024e, edging up from around 2.76 million tonnes in 2022 to an estimated 2.84 million tonnes in 2024. As wheat, maize, rice and other staple cereals continue to be produced at this scale, farmers face mounting pressure to optimize yields, inputs and resilience through advanced agritech solutions. OG Analysis estimates, derived from FAO cereal statistics and market outlooks, illustrate how large, stable cereal volumes underpin long-term demand for precision farming tools, digital platforms, automation and data-driven agritech services.

The agritech market is expanding as global cereal production remains exceptionally high—rising from about 2.76 million tonnes in 2022 to an estimated 2.84 million tonnes in 2024—driving demand for digital, automated, and precision-enabled farming systems. Sustaining output at this scale requires advances in sensors, IoT platforms, variable-rate technologies, and real-time crop analytics to manage climate volatility, input efficiency, and yield optimization. The continuous growth and complexity of cereal production reinforce the need for integrated agritech solutions that enhance productivity while reducing resource intensity. As governments and agribusinesses invest in resilient, data-driven food systems, agritech becomes central to long-term global food security and sustainable agricultural modernization.

Regional Analysis

North America Agritech Market

North America Agritech Market is driven by strong adoption of precision farming, farm management software, autonomous equipment, smart irrigation, livestock monitoring, and data-driven crop analytics. Market dynamics are shaped by large-scale commercial farming, labor shortages, rising input costs, sustainability targets, and demand for higher productivity across row crops, specialty crops, and livestock operations. Lucrative opportunities exist for drone companies, sensor providers, AI advisory platforms, robotics developers, irrigation technology firms, equipment manufacturers, and carbon farming solution providers. Latest trends include autonomous tractors, satellite-based crop monitoring, regenerative agriculture platforms, AI-enabled yield forecasting, digital farm records, and smart spraying technologies. The forecast outlook remains favorable as growers continue investing in automation, resource efficiency, climate resilience, and measurable farm profitability.

Asia Pacific Agritech Market

Asia Pacific Agritech Market is expanding rapidly due to population growth, food security needs, smallholder farm modernization, rising government support for digital agriculture, and increasing demand for efficient crop and livestock management. Market dynamics are supported by adoption of mobile advisory platforms, smart irrigation, drone spraying, farm mechanization, controlled-environment farming, and digital marketplaces across both developed and emerging agricultural economies. The region presents strong opportunities for agritech start-ups, equipment manufacturers, input companies, satellite analytics providers, agri-fintech platforms, and irrigation technology suppliers. Latest trends include AI-based crop advisory, drone-enabled farm services, precision irrigation, traceability tools, vertical farming, and climate-smart farming models. The forecast remains positive as farmers, cooperatives, governments, and agribusinesses invest in productivity improvement, digital access, and sustainable food production.

Europe Agritech Market

Europe Agritech Market is shaped by sustainability regulations, climate-smart farming policies, advanced farm mechanization, precision agriculture adoption, and strong emphasis on traceability and environmental performance. Market dynamics are influenced by demand for reduced chemical use, soil health monitoring, low-emission farming, digital compliance tools, robotic weeding, smart greenhouses, and data-driven livestock management. Lucrative opportunities exist for farm software vendors, robotics companies, sensor manufacturers, carbon measurement platforms, greenhouse technology providers, and precision equipment suppliers. Latest trends include regenerative agriculture tools, autonomous field robots, satellite monitoring, variable-rate input application, carbon farming platforms, and digital farm compliance systems. The forecast outlook remains steady as European agriculture continues prioritizing sustainability, resource efficiency, food quality, and resilient production systems.

Middle East & Africa Agritech Market

Middle East & Africa Agritech Market is developing through food security programs, water scarcity management, controlled-environment agriculture, irrigation modernization, digital advisory services, and livestock productivity improvement. Market dynamics vary across the region, with Gulf countries investing in vertical farms, greenhouse systems, hydroponics, smart irrigation, and desert agriculture, while African markets present opportunities through mobile farm advisory, mechanization, agri-marketplaces, soil testing, and climate-resilient crop tools. Companies can benefit by offering affordable, scalable, and locally adapted agritech solutions suited to smallholders, arid climates, and fragmented supply chains. Latest trends include solar-powered irrigation, digital extension services, protected cultivation, remote sensing, livestock tracking, and farm-to-market platforms. The forecast remains constructive as governments and investors focus on food self-sufficiency, water efficiency, and agricultural productivity.

South & Central America Agritech Market

South & Central America Agritech Market is supported by large-scale crop production, livestock farming, export-oriented agriculture, precision farming adoption, and growing need for sustainable land and input management. Market dynamics are shaped by soybean, corn, sugarcane, coffee, fruits, beef, and specialty crop production, where farmers seek technologies that improve yield, traceability, irrigation efficiency, and farm profitability. Opportunities exist for drone service providers, satellite analytics companies, farm management software firms, smart equipment suppliers, livestock monitoring platforms, and sustainability-focused agritech companies. Latest trends include digital crop scouting, precision spraying, soil health analytics, carbon and deforestation monitoring, smart irrigation, and supply-chain traceability. The forecast outlook remains positive as agribusinesses and producers continue investing in productivity, compliance, climate resilience, and export competitiveness.

Report Scope

| Parameter | Agritech Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Application, By Sector |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Big Data And Analytics

- Biotechnology And Biochemical

- Mobility

- Sensors And Connected Devices

- Other Types

By Application

- Production And Maintenance

- Irrigation

- Supply Chain

- Marketplace

- Other Applications

By Sector

- Precision Farming

- Agriculture

- Agrochemicals

- Smart Agriculture

- Biotechnology

- Indoor Farming

- Other Sectors

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Cargill Incorporated

- Archer Daniels Midland Company (ADM)

- BASF SE

- Wilmar International Limited

- Bunge Limited

- Dow AgroSciences LLC

- Bayer Crop Science AG

- Deere & Company

- Nutrien Ltd.

- Syngenta Group AG

- Olam International Limited

- Yara International ASA

- CNH Industrial NV

- Sumitomo Chemical Company Limited

- Kubota Corporation

- The Mosaic Company

- Corteva Agriscience Inc.

- The Andersons Inc.

- Land O'Lakes Inc.

- Tractor Supply Company

- Ball Corporation

- Tetra Pak Group

- AGCO Corporation

- Darling Ingredients Inc.

- Calavo Growers Inc.

Recent Developments

- May 2026 - Planet’s subsidiary Sinergise Solutions secured a contract with the Czech Republic’s State Agricultural Intervention Fund to provide satellite imagery and AI-powered analytics for agricultural monitoring. The development supports wider use of remote sensing, automated claim validation, and country-level digital farm compliance systems.

- May 2026 - TerraBlaster advanced plans for a real-time soil nutrient mapping launch, targeting tractor-speed NPK analysis for precision agriculture. The development reflects growing demand for in-field soil intelligence that can support variable-rate input management and better fertilizer decisions.

- April 2026 - CropX expanded its sensor portfolio with Apex, a multi-depth soil sensor integrated into its digital agronomy platform. The product strengthens root-zone monitoring, irrigation insights, salinity tracking, and data-driven crop management for growers.

- February 2026 - John Deere announced its 2026 Startup Collaborator cohort, including companies working on edge AI, telematics, soil sensing, robotics foundation models, and drone-based crop intelligence. The program reinforces growing collaboration between large equipment manufacturers and agritech start-ups.

- February 2026 - AGCO brands showcased innovations and autonomous solutions for the 2026 season, including offerings from Fendt, Massey Ferguson, and PTx. The development supports stronger adoption of practical automation, precision farming tools, and integrated equipment technologies.

- February 2026 - KIOTI Europe and Naïo Technologies signed a strategic partnership to develop a new agricultural robotic platform. The collaboration combines agricultural equipment manufacturing and robotics expertise to support autonomous farming solutions.

- February 2026 - Carbon Robotics launched its Large Plant Model, an AI technology designed to improve LaserWeeder performance across diverse crops, weeds, and field conditions. The development highlights rapid progress in AI-enabled, chemical-free weed control.

- January 2026 - SAP and Syngenta announced a multi-year strategic technology partnership to scale AI-assisted agriculture across Syngenta’s operations. The partnership supports digital transformation in agricultural innovation, enterprise workflows, and data-driven decision-making.

- January 2026 - Precision Planting launched a Seed Orientation System at the 2026 PTx Winter Conference, along with new planting and spraying technologies. The launch supports precision placement, improved field operations, and higher efficiency in crop establishment.

- January 2026 - Taranis and SiFly launched a field validation program combining autonomous drones with AI-driven crop intelligence. The program is designed to scale aerial data collection and improve operational productivity in precision crop monitoring.

FAQ's

The Agritech Market is estimated to reach $ 86.58 billion by 2034.

The Agritech Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 12% during the forecast period from 2026 to 2034.

The Agritech Market is estimated to generate $ 34.16 billion in revenue in 2026.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!