"The Air Quality Sensors Market was valued at $ 5437.18 billion in 2026 and is projected to reach $ 9203.32 billion by 2034, growing at a CAGR of 7.48%."

The air quality sensors market is a fast-growing segment of the environmental monitoring, smart building, automotive, industrial safety, and IoT sensing industry, focused on detecting and measuring pollutants, gases, particles, and environmental conditions that affect indoor and outdoor air quality. These sensors are widely used in residential air purifiers, HVAC systems, smart homes, offices, schools, hospitals, industrial facilities, vehicles, public infrastructure, environmental monitoring stations, and wearable or portable devices. Key sensing targets include particulate matter, carbon dioxide, carbon monoxide, volatile organic compounds, nitrogen oxides, ozone, sulfur dioxide, humidity, and temperature. Demand is being driven by rising awareness of air pollution, growing concern over indoor air quality, stricter environmental and workplace safety expectations, and increasing adoption of connected monitoring systems across buildings, cities, and industrial operations.

Recent trends in the air quality sensors market include miniaturization, improved sensor accuracy, low-power designs, multi-gas sensing modules, wireless connectivity, and integration with building automation and air purification systems. Manufacturers are focusing on sensors that deliver real-time data, longer operating life, better calibration stability, and compatibility with IoT platforms and predictive ventilation controls. Growth is further supported by smart city initiatives, green building practices, health-conscious consumers, industrial emission monitoring, and automotive cabin air quality management. Competitive dynamics are shaped by sensor manufacturers, semiconductor companies, environmental monitoring firms, HVAC technology providers, consumer electronics brands, and industrial automation suppliers competing on accuracy, reliability, cost, form factor, response time, and platform integration. At the same time, calibration drift, cross-sensitivity, standardization challenges, data interpretation complexity, and cost pressure continue to influence product development and market adoption.

Key Insights

- Indoor air quality monitoring remains a major demand driver as homes, offices, schools, healthcare facilities, and commercial buildings increasingly adopt sensors to detect pollutants, carbon dioxide, volatile organic compounds, and particulate matter. Growing awareness of ventilation quality and occupant health is strengthening demand for real-time monitoring. This trend is making air quality sensors integral to smart buildings and wellness-focused indoor environments.

- Particulate matter sensors are among the most important product categories due to their role in measuring fine particles from pollution, smoke, dust, combustion, and industrial sources. These sensors are widely used in air purifiers, environmental monitors, HVAC systems, and portable devices. Demand is supported by rising concern over respiratory health and the need for continuous monitoring of airborne particle exposure.

- Carbon dioxide sensing is gaining importance in building ventilation management, especially as occupants and facility managers seek better visibility into air exchange and indoor crowding conditions. CO₂ sensors help optimize HVAC operation, improve comfort, and support energy-efficient ventilation. Their adoption is increasing across offices, classrooms, public buildings, and smart home systems.

- Smart city and outdoor monitoring applications are creating opportunities for sensor networks that measure urban pollution, traffic emissions, industrial air quality, and environmental exposure. Compact connected sensors can support distributed monitoring beyond traditional fixed stations. This is strengthening demand for scalable, wireless, and data-enabled air quality monitoring solutions.

- Automotive air quality sensing is becoming more relevant as vehicle manufacturers integrate cabin air monitoring, automatic recirculation control, and pollutant detection into comfort and safety systems. Sensors help manage exposure to exhaust gases, particulate matter, and volatile compounds. As connected and premium vehicles evolve, cabin environmental sensing is becoming a stronger differentiator.

- Industrial and workplace safety applications support demand for gas sensors that detect hazardous gases, emissions, and poor air conditions in factories, mines, refineries, laboratories, and confined spaces. These applications require reliable detection, fast response, and robust performance under harsh operating conditions. Regulatory compliance and worker safety remain key purchasing drivers.

- IoT integration and wireless connectivity are reshaping the market by enabling real-time monitoring, remote alerts, cloud analytics, and automated control of ventilation, filtration, and environmental systems. Connected sensors are becoming part of broader building management and environmental intelligence platforms. This creates opportunities for suppliers offering hardware, software, and data integration capabilities.

- Future market growth will be driven by rising pollution awareness, smart buildings, air purification demand, environmental regulation, industrial safety, and consumer interest in health-oriented technologies. Opportunities will expand where sensors deliver accuracy, low power use, small size, and easy integration. Long-term competitiveness will depend on calibration reliability, data quality, interoperability, and cost-effective manufacturing.

Regional Analysis

North America Air Quality Sensors Market

North America remains a leading air quality sensors market, supported by strong environmental awareness, advanced smart building adoption, stringent workplace safety standards, and growing deployment of connected monitoring systems. Market dynamics are shaped by demand from residential buildings, commercial facilities, healthcare institutions, industrial plants, and smart city projects. Lucrative opportunities are strong in indoor air quality monitoring, HVAC optimization, industrial gas detection, and environmental sensing networks. The forecast remains favorable as health and sustainability priorities increase, while latest developments focus on AI-enabled monitoring, wireless sensor networks, and integration with building management systems.

Asia Pacific Air Quality Sensors Market

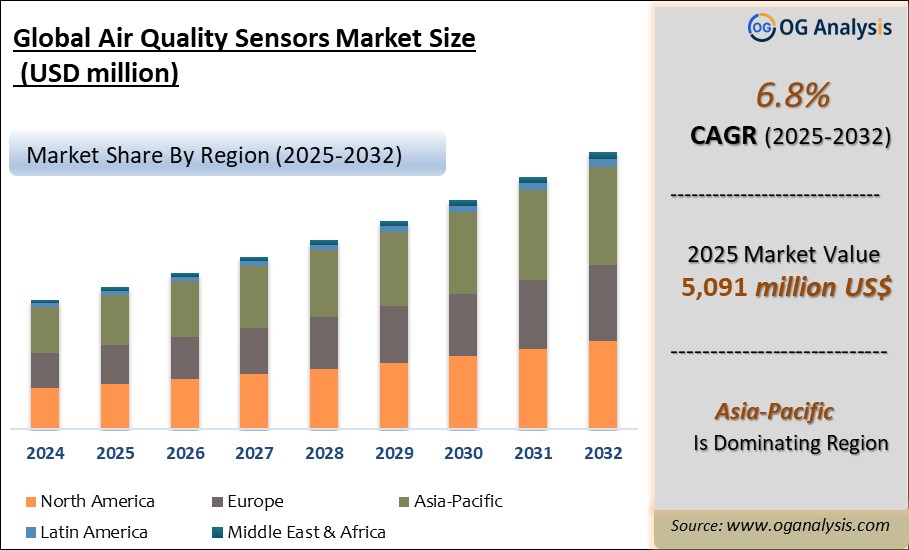

Asia Pacific is the fastest-growing air quality sensors market, driven by rapid urbanization, industrial expansion, rising pollution concerns, smart city initiatives, and increasing adoption of air purification systems. Market dynamics are influenced by government air quality programs, growing consumer awareness, and demand for environmental monitoring across residential, commercial, and industrial sectors. Lucrative opportunities are visible in smart homes, industrial emission monitoring, public infrastructure, portable air quality devices, and connected HVAC systems. The forecast remains robust as environmental monitoring becomes a priority across major economies, while latest developments focus on low-cost sensors, local manufacturing, and large-scale sensor deployment networks.

Europe Air Quality Sensors Market

Europe represents a mature and regulation-driven air quality sensors market, supported by strict environmental standards, sustainable building initiatives, smart mobility programs, and strong emphasis on public health. Market dynamics are shaped by demand for indoor air quality management, urban pollution monitoring, industrial compliance, and energy-efficient building operations. Lucrative opportunities are concentrated in smart buildings, transportation systems, environmental monitoring networks, and advanced ventilation management solutions. The forecast remains constructive as sustainability and emissions reduction efforts continue, while latest developments center on high-accuracy sensors, integrated environmental platforms, and real-time air quality analytics.

Middle East & Africa Air Quality Sensors Market

The Middle East & Africa air quality sensors market is developing steadily, supported by urban development, industrial expansion, smart city investments, and increasing awareness of environmental health issues. Market dynamics are influenced by air pollution monitoring requirements, industrial safety needs, harsh climate conditions, and demand for indoor air quality management in commercial and residential buildings. Lucrative opportunities are emerging in smart infrastructure, industrial facilities, healthcare environments, and public air monitoring systems. The forecast remains positive as environmental monitoring initiatives expand, while latest developments focus on smart city integration, wireless monitoring solutions, and broader deployment of indoor air quality technologies.

South & Central America Air Quality Sensors Market

South & Central America presents promising growth opportunities in the air quality sensors market, supported by increasing urbanization, industrial activity, environmental awareness, and adoption of smart building technologies. Market dynamics are shaped by demand for pollution monitoring, workplace safety systems, residential air quality solutions, and environmental compliance applications. Lucrative opportunities are visible in commercial buildings, industrial facilities, public monitoring projects, and consumer air purification devices. The forecast remains encouraging as governments and private organizations invest in environmental monitoring capabilities, while latest developments focus on connected sensing platforms, portable monitoring devices, and expansion of regional air quality management programs.

Market Scope

| Parameter | Air Quality Sensors Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Pollutant, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type:

- Indoor

- Outdoor

By Pollutant:

- Particulate Matter

- Gases

- Others

By End User:

- Residential

- Commercial

- Industrial

- Government

By Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Key Companies Covered

Honeywell International Inc., Siemens AG, Bosch Sensortec GmbH, Sensirion AG, ams-OSRAM AG, STMicroelectronics N.V., Infineon Technologies AG, Renesas Electronics Corporation, Figaro Engineering Inc., Alphasense Ltd., Aeroqual Ltd., Vaisala Oyj, Teledyne FLIR LLC, SPEC Sensors LLC, Cubic Sensor and Instrument Co., Ltd., Winsen Electronics Technology Co., Ltd., OMRON Corporation, Panasonic Holdings Corporation, ABB Ltd., Emerson Electric Co.

Recent Developments

- March 2026 – Honeywell expanded its indoor air quality portfolio with advanced connected sensing solutions designed for smart buildings, integrating air quality monitoring with automated ventilation and building management systems.

- February 2026 – Sensirion introduced next-generation environmental sensing modules featuring enhanced particulate matter and gas detection capabilities for air purifiers, HVAC equipment, and smart indoor environments.

- January 2026 – Bosch Sensortec advanced its compact air quality sensor portfolio with improved measurement accuracy and lower power consumption for wearable, smart home, and IoT applications.

- November 2025 – Siemens strengthened its smart building technologies by integrating advanced indoor air quality monitoring functions into building automation platforms to support healthier and more energy-efficient facilities.

- October 2025 – ams OSRAM launched enhanced environmental sensing solutions capable of measuring particulate matter and multiple air quality parameters, targeting consumer electronics, smart buildings, and industrial monitoring applications.

- September 2025 – Renesas Electronics expanded its environmental sensor offerings with integrated air quality monitoring capabilities designed for connected home, industrial, and smart city applications.

- July 2025 – Figaro Engineering introduced upgraded gas sensing technologies for indoor air quality monitoring, focusing on improved sensitivity, reliability, and long-term operational stability.

- June 2025 – Infineon Technologies enhanced its environmental sensing portfolio through advanced MEMS-based solutions supporting real-time air quality monitoring in smart devices and building management systems.

- April 2025 – Honeywell launched new industrial-grade gas detection and air monitoring technologies aimed at improving worker safety, environmental compliance, and operational visibility across industrial facilities.

- February 2025 – STMicroelectronics expanded its environmental sensor platform with improved integration capabilities for smart homes, connected appliances, air purification systems, and portable air quality monitoring devices.

FAQ's

The Air Quality Sensors Market is estimated to generate $ 5437.19 million in revenue in 2026.

The Air Quality Sensors Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period from 2026 to 2034.

The Air Quality Sensors Market is estimated to reach $ 9203.22 million by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!