"The Global Antibody Based Therapeutics Market valued at USD 267.8 billion in 2024, is expected to grow by 8.2% CAGR to reach market size worth USD 601.3 billion by 2034."

The Antibody-Based Therapeutics Market has emerged as a transformative force in modern medicine, offering highly targeted treatments for a range of chronic and life-threatening diseases including cancer, autoimmune disorders, infectious diseases, and more. The market's growth is driven by advancements in monoclonal antibody engineering, increasing approval rates of biologics, and strong demand for precision medicine. In recent years, pharmaceutical companies have increasingly shifted focus from traditional small molecules to antibody-based therapies due to their superior specificity and efficacy. Furthermore, the rise in chronic illnesses globally, aging populations, and strategic collaborations between biotechnology firms and academic institutions are accelerating innovation and commercial uptake. Regulatory agencies such as the FDA and EMA are also fast-tracking approvals of novel antibody therapeutics, reinforcing the market’s growth potential through 2034.

A surge in R&D investments, emergence of bispecific antibodies, and the adoption of AI for antibody design are reshaping the competitive landscape. From oncology to neurology and rare diseases, antibody-based therapeutics are gaining traction for their adaptability and efficacy. Biosimilar development is adding a cost-competitive edge, making these treatments more accessible across emerging economies. The market is highly consolidated with leading players investing in next-generation antibody formats, such as antibody-drug conjugates and immunocytokines, which are showing promising results in clinical trials. Additionally, the increasing adoption of subcutaneous formulations over intravenous administration is improving patient compliance and convenience. Supply chain resilience, manufacturing scalability, and the integration of real-world data are becoming critical for market participants to maintain a competitive edge in a rapidly evolving global therapeutic environment.

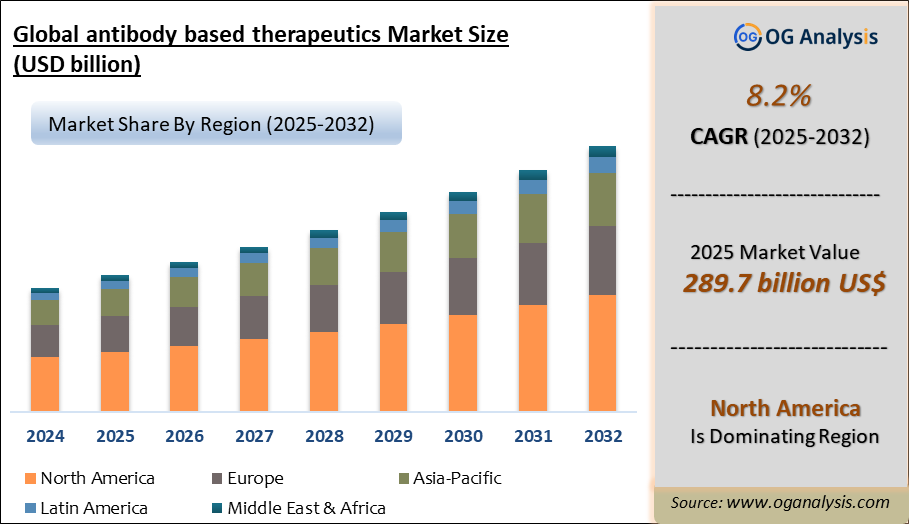

North America dominates the antibody-based therapeutics market with a commanding 44% share, fueled by advanced healthcare infrastructure and high R&D investments, while the oncology segment leads due to the rising prevalence of cancer and targeted treatment innovations.

Antibody Based Therapeutics Market Strategy, Price Trends, Drivers, Challenges and Opportunities to 2034

-

The rise in chronic illnesses such as cancer, rheumatoid arthritis, and Crohn’s disease is accelerating demand for antibody-based therapeutics due to their high specificity and fewer side effects compared to traditional drugs, making them integral to long-term disease management in both developed and developing regions.

-

Monoclonal antibodies dominate the therapeutic landscape, supported by continued innovations in antibody engineering and Fc modification techniques, which improve pharmacokinetics, enhance immune response, and reduce immunogenicity, enabling their use in an expanding range of disease indications.

-

Pharmaceutical companies are aggressively pursuing bispecific antibodies and antibody-drug conjugates, which combine targeting precision with cytotoxic payloads, offering superior efficacy in oncology treatments and showing strong performance in ongoing clinical trials for solid tumors and hematologic malignancies.

-

Strategic alliances between biotech startups and pharmaceutical giants are increasing to co-develop next-generation antibody therapies, optimize development timelines, and expand commercialization reach, helping smaller firms navigate regulatory complexities while accelerating innovation.

-

The biosimilars segment is gaining traction as patents expire for blockbuster monoclonal antibody drugs like Humira and Herceptin, enabling broader patient access, driving down treatment costs, and promoting healthy competition among manufacturers globally.

-

AI-driven platforms are transforming antibody discovery by predicting binding affinity, optimizing antibody structure, and reducing development time, significantly boosting R&D productivity and improving clinical candidate selection across multiple therapeutic areas.

-

Patient-friendly drug delivery formats such as subcutaneous and auto-injector-based formulations are gaining popularity over intravenous options due to ease of use, improved compliance, reduced healthcare facility visits, and enhanced patient quality of life.

-

The increasing prevalence of infectious diseases, including COVID-19 and RSV, is boosting the development of neutralizing antibody therapies, with governments and health agencies supporting rapid development and procurement for pandemic preparedness.

-

Manufacturing scalability is being addressed through single-use bioreactors, modular facilities, and strategic outsourcing, helping producers meet growing global demand while maintaining stringent quality and regulatory standards.

-

The therapeutic potential of antibody-based drugs is expanding beyond oncology into neurology, cardiology, and rare genetic disorders, supported by positive clinical trial outcomes and ongoing regulatory approvals that highlight their broad clinical utility.

North America Antibody Based Therapeutics Market Analysis

The North American Antibody Based Therapeutics market witnessed significant growth in 2024, driven by advances in biopharmaceutical innovation, digital health integration, and increasing demand for precision medicine. Key segments such as healthcare cloud computing, IoT medical devices, and advanced wound care are thriving due to strong adoption of next-generation technologies and supportive regulatory frameworks. From 2025 and beyond, the market is expected to expand at a steady CAGR, bolstered by investments in artificial intelligence for diagnostics, mHealth solutions, and real-world evidence platforms. Rising healthcare expenditure, growing prevalence of chronic diseases, and the push for home-based care are critical growth drivers. Furthermore, market dynamics are influenced by developments in the active pharmaceutical ingredients (API) market and regenerative medicine. The ongoing adoption of track-and-trace solutions and advancements in preimplantation genetic testing further exemplify North America's leadership in healthcare innovation.

Europe Antibody Based Therapeutics Market Outlook

The European healthcare and pharmaceuticals market observed steady growth in 2024, fueled by the region's emphasis on sustainability, advanced therapeutics, and digital transformation. The strong focus on biopharmaceuticals, including antibody-based therapeutics and regenerative medicine, complements growing investments in healthcare simulation and remote patient monitoring. The Antibody Based Therapeutics market is anticipated to accelerate in 2025, with substantial gains through 2034 driven by EU healthcare reforms, greater adoption of proteomics and single-cell analysis, and initiatives promoting healthcare cloud computing and sterilization equipment. The demand for advanced diagnostic and therapeutic solutions is supported by government-backed R&D programs and a rising aging population. Additionally, Europe's leadership in clinical trial innovations, coupled with increasing adoption of IoT medical devices and mental health screening, enhances its position as a key global player in the healthcare sector.

Asia-Pacific Healthcare & Pharmaceuticals Market

The Asia-Pacific healthcare and pharmaceuticals market is set for dynamic expansion, underpinned by rapid advancements in biotechnology, digital healthcare solutions, and rising healthcare infrastructure investment. Growing economies like China and India are at the forefront, driving demand for mHealth solutions, biopreservation technologies, and smart medical devices. The Antibody Based Therapeutics market is projected to grow at the fastest pace globally during the forecast period 2025 to 2034, spurred by increasing healthcare access, population growth, and rising prevalence of chronic diseases. The adoption of laboratory information systems (LIS), real-world evidence solutions, and sepsis diagnostics reflects a trend toward data-driven, precision-focused healthcare. Strategic partnerships in the biopharmaceutical processing equipment and consumables sector, alongside burgeoning interest in 3D cell culture and amniotic membrane applications, highlight the region’s evolving role as a healthcare innovation hub.

Middle East, Africa, Latin America Antibody Based Therapeutics Market Overview

The Rest of the World Antibody Based Therapeutics market registering moderate growth in 2024, is driven by increasing healthcare initiatives in emerging markets and growing interest in telemedicine and at-home testing solutions. Investments in anesthesia drugs, animal health, and anti-counterfeit pharmaceuticals packaging are gaining traction, particularly in Latin America, Africa, and the Middle East. From 2025 through 2034, the market is expected to witness accelerated growth, fueled by expanding healthcare infrastructure and rising awareness of advanced healthcare solutions. Markets for remote patient monitoring, rehabilitation equipment, and radiation dose management systems are emerging as key areas of focus. Growth in these regions is supported by a rising middle-class population, greater healthcare access, and enhanced pharmaceutical supply chain capabilities. The adoption of smart medical devices and clinical trial innovations also underscores the evolving healthcare landscape in the Middle East, Africa, Latin America regions.

Antibody Based Therapeutics Market Dynamics and Future Analytics

The research evaluates the Antibody-Based Therapeutics market by analyzing its parent, derived, and intermediary markets, along with raw material sourcing and substitute options to provide a comprehensive market outlook. It includes geopolitical and demographic assessments, along with Porter’s Five Forces analysis, to deliver accurate market projections and understand the competitive dynamics shaping the industry.

Recent mergers, acquisitions, and strategic developments are reviewed for their influence on the market's future direction. Key indicators such as barriers to entry, capital intensity, government regulations, product differentiation, supplier landscape, substitute cost, and distribution channels are thoroughly examined. This approach highlights market attractiveness and identifies growth opportunities and competitive pressures within the Antibody-Based Therapeutics segment.

Trade and pricing trends are also analyzed to understand global market dynamics. This includes identifying top exporting and importing countries, evaluating key supplier and customer bases, and assessing international pricing patterns. The findings support clients in strategic procurement planning, identifying reliable vendor partnerships, interpreting pricing fluctuations, and tapping into new distribution channels. The research is continuously updated to reflect the latest developments, including geopolitical impacts such as the Russia-Ukraine conflict, ensuring relevance and accuracy in decision-making.

Antibody Based Therapeutics Market Structure, Competitive Intelligence and Key Winning Strategies

The report presents detailed profiles of top companies operating in the Antibody Based Therapeutics market and players serving the Antibody Based Therapeutics value chain along with their strategies for the near, medium, and long term period.

OGAnalysis’ proprietary company revenue and product analysis model unveils the Antibody Based Therapeutics market structure and competitive landscape. Company profiles of key players with a business description, product portfolio, SWOT analysis, Financial Analysis, and key strategies are covered in the report. It identifies top-performing Antibody Based Therapeutics products in global and regional markets. New Product Launches, Investment & Funding updates, Mergers & Acquisitions, Collaboration & Partnership, Awards and Agreements, Expansion, and other developments give our clients the Antibody Based Therapeutics market update to stay ahead of the competition.

Company offerings in different segments across Asia-Pacific, Europe, the Middle East, Africa, and South and Central America are presented to better understand the company strategy for the Antibody Based Therapeutics market. The competition analysis enables users to assess competitor strategies and helps align their capabilities and resources for future growth prospects to improve their market share.

Antibody Based Therapeutics Market Research Scope

• Global Antibody Based Therapeutics market size and growth projections (CAGR), 2024- 2034

• Policies of USA New President Trump, Russia-Ukraine War, Israel-Palestine, Middle East Tensions Impact on the Antibody Based Therapeutics Trade and Supply-chain

• Antibody Based Therapeutics market size, share, and outlook across 5 regions and 27 countries, 2023- 2034

• Antibody Based Therapeutics market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2023- 2034

• Short and long-term Antibody Based Therapeutics market trends, drivers, restraints, and opportunities

• Porter’s Five Forces analysis, Technological developments in the Antibody Based Therapeutics market, Antibody Based Therapeutics supply chain analysis

• Antibody Based Therapeutics trade analysis, Antibody Based Therapeutics market price analysis, Antibody Based Therapeutics supply/demand

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products

• Latest Antibody Based Therapeutics market news and developments

The Antibody Based Therapeutics Market international scenario is well established in the report with separate chapters on North America Antibody Based Therapeutics Market, Europe Antibody Based Therapeutics Market, Asia-Pacific Antibody Based Therapeutics Market, Middle East and Africa Antibody Based Therapeutics Market, and South and Central America Antibody Based Therapeutics Markets. These sections further fragment the regional Antibody Based Therapeutics market by type, application, end-user, and country.

Market Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Source, By Indication, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Antibody Based Therapeutics market sales data at the global, regional, and key country levels with a detailed outlook to 2034 allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Antibody Based Therapeutics market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Antibody Based Therapeutics market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Antibody Based Therapeutics business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Antibody Based Therapeutics Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below –

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Antibody Based Therapeutics Pricing and Margins Across the Supply Chain, Antibody Based Therapeutics Price Analysis / International Trade Data / Import-Export Analysis,

Supply Chain Analysis, Supply – Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Antibody Based Therapeutics market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note Latest developments will be updated in the report and delivered within 2 to 3 working days

Antibody Based Therapeutics Market Segmentation

By Product Type

- Monoclonal Antibodies (mAbs)

- Antibody-Drug Conjugates (ADCs)

- Bispecific Antibodies

- Others

By Source

- Human Monoclonal Antibodies

- Humanized Monoclonal Antibodies

- Chimeric Monoclonal Antibodies

- Murine Monoclonal Antibodies

By Indication

- Oncology

- Autoimmune Diseases

- Infectious Diseases

- Hematological Diseases

By End-User

- Hospitals

- Specialty Centers

- Research Institutes

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

-

Roche

-

AbbVie

-

Amgen

-

Bristol-Myers Squibb

-

Johnson & Johnson

-

Seagen

-

Merck

-

Regeneron

-

Novartis

-

AstraZeneca

-

Eli Lilly

-

GlaxoSmithKline (GSK)

-

Takeda

Recent Developments

-

July 2025 I-Mab completed the acquisition of Bridge Health, securing upstream rights to the CLDN18.2 antibody and eliminating licensing costs for its bispecific therapy givastomig. The move enhances pipeline control and aligns with its broader oncology strategy.

-

July 2025 A neuroblastoma patient achieved over 18 years of remission following pediatric CAR-T therapy, highlighting the long-term potential of antibody-based cellular therapies in treating solid tumors.

-

June 2025 The FDA removed the REMS requirement for all approved CAR-T cell therapies, simplifying safety protocols and making it easier for smaller clinics to administer these treatments.

-

June 2025 The FDA granted accelerated approval to a TROP-2 targeting antibody-drug conjugate for use in EGFR-mutant non-small cell lung cancer, marking an expansion of targeted therapies in lung oncology.

-

May 2025 AbbVie secured FDA approval for telisotuzumab vedotin, an ADC aimed at c-Met positive non-squamous NSCLC, providing new treatment options for a subset of lung cancer patients.

-

May 2025 Regeneron and UCB received U.S. approval for linvoseltamab, a bispecific antibody targeting CD3 and BCMA, indicated for relapsed or refractory multiple myeloma, reinforcing advances in dual-targeted therapeutics.

-

April 2025 Tafasitamab's label was expanded by the FDA to include use in combination with lenalidomide and rituximab for relapsed or refractory follicular lymphoma, broadening its role in B-cell malignancies.

-

April 2025 A new antibody therapeutic against PD-L1 entered Phase 3 trials for head and neck cancers, signaling continued clinical expansion of checkpoint inhibitors into niche oncology segments.

-

March 2025 A mid-sized biotech initiated clinical trials for a first-in-class antibody targeting Siglec-15 in colorectal cancer, aiming to overcome resistance to existing immunotherapies.

FAQ's

The Antibody Based Therapeutics Market is estimated to reach USD 601.3 billion by 2034.

The Global Antibody Based Therapeutics Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% during the forecast period from 2025 to 2034.

The Global Antibody Based Therapeutics Market is estimated to generate USD 286.9 billion in revenue in 2025

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!