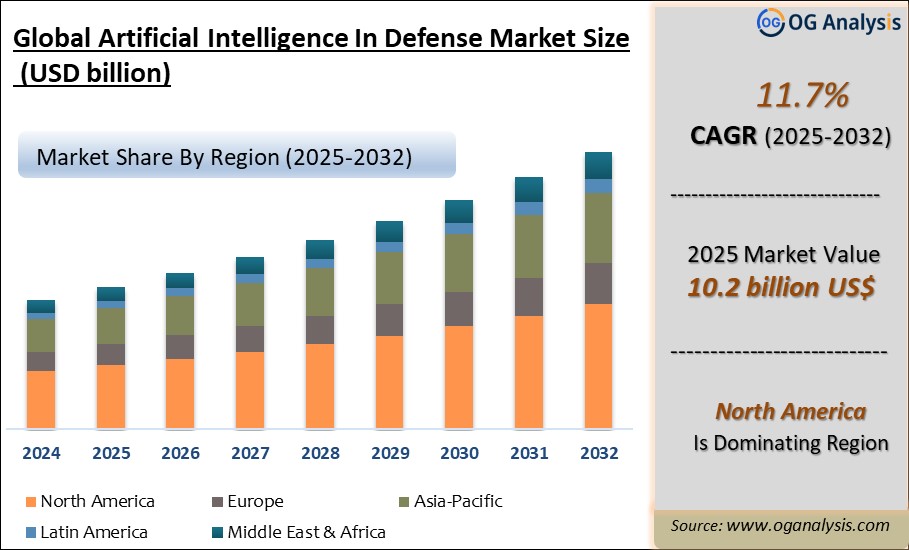

"The Global Artificial Intelligence in Defense Market Size was valued at USD 9.3 billion in 2024 and is projected to reach USD 10.2 billion in 2025. Worldwide sales of Artificial Intelligence in Defense are expected to grow at a significant CAGR of 11.7%, reaching USD 28.4 billion by the end of the forecast period in 2034."

Artificial Intelligence in Defense Market Report Description

The artificial intelligence (AI) in defense market is revolutionizing the way military and defense operations are conducted worldwide. AI technologies, encompassing machine learning, natural language processing, and computer vision, are being integrated into various defense applications to enhance decision-making, improve operational efficiency, and reduce human involvement in dangerous missions. AI-driven systems are capable of analyzing vast amounts of data in real-time, providing actionable intelligence, predicting potential threats, and automating complex tasks. These advancements enable militaries to respond faster and more accurately to emerging threats, significantly enhancing their strategic capabilities. The adoption of AI in defense is driven by the need to maintain technological superiority, address evolving security challenges, and optimize resource allocation. Governments and defense organizations are investing heavily in AI research and development, fostering collaborations with technology companies and academic institutions to advance AI capabilities. This report provides a comprehensive analysis of the current state of AI in the defense market, highlighting key trends, drivers, challenges, and the competitive landscape.

The North America region dominates the Artificial Intelligence in Defense Market, propelled by substantial investments in cybersecurity. It is projected to account for approximately 45% of the total market share.

Artificial Intelligence in Defense Market: Latest Trends, Drivers, and Challenges

One of the most significant trends in the AI in defense market is the development of autonomous weapon systems. These systems leverage AI to perform tasks such as target identification, threat assessment, and decision-making without human intervention. Autonomous drones, ground vehicles, and naval vessels are being designed to carry out missions independently, offering strategic advantages in terms of speed and precision. Another notable trend is the use of AI for cyber defense. AI algorithms are employed to detect, analyze, and respond to cyber threats in real-time, enhancing the cybersecurity posture of defense networks. Additionally, AI is being integrated into intelligence, surveillance, and reconnaissance (ISR) systems to improve data collection, analysis, and dissemination. These AI-powered ISR systems provide enhanced situational awareness, enabling defense forces to make informed decisions quickly. The trend towards AI-driven simulation and training programs is also gaining traction, offering realistic and adaptive training environments for military personnel.

Several factors are driving the growth of AI in the defense market. The primary driver is the increasing need for advanced defense capabilities to counter sophisticated threats. AI technologies provide a competitive edge by enhancing the speed and accuracy of threat detection and response. The growing volume and complexity of data generated by modern defense systems necessitate the use of AI for efficient data processing and analysis. Another key driver is the push for automation in defense operations to reduce human involvement in high-risk missions and improve operational efficiency. Governments and defense organizations are prioritizing investments in AI to maintain technological superiority and strengthen national security. Additionally, the advancements in AI technologies, such as deep learning and neural networks, are expanding the potential applications of AI in defense, driving further adoption. Collaborative efforts between defense agencies and technology companies are also fostering innovation and accelerating the development of AI solutions for defense applications.

Despite the promising growth prospects, the AI in defense market faces several challenges. One of the primary challenges is the ethical and legal implications of using AI in autonomous weapon systems. The potential for unintended consequences and the lack of accountability in decision-making raise significant concerns. Ensuring the reliability and security of AI systems is another major challenge, as adversarial attacks on AI algorithms can compromise their effectiveness. The high cost of developing and deploying AI technologies poses financial challenges for defense organizations, particularly in developing countries. Additionally, the integration of AI into existing defense systems requires significant infrastructure and interoperability improvements, which can be complex and time-consuming. The shortage of skilled AI professionals and the need for continuous advancements in AI research and development also present hurdles to the widespread adoption of AI in defense.

Major Players in the AI in Defense Market

1. Lockheed Martin Corporation

2. Northrop Grumman Corporation

3. Raytheon Technologies Corporation

4. Boeing Defense, Space & Security

5. BAE Systems plc

6. Thales Group

7. Leonardo S.p.A.

8. General Dynamics Corporation

9. IBM Corporation

10. Microsoft Corporation

11. NVIDIA Corporation

12. Palantir Technologies Inc.

13. L3Harris Technologies, Inc.

14. Elbit Systems Ltd.

15. SAIC (Science Applications International Corporation)

Market scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD Billion |

| Market Splits Covered | By Application, By Technology, and By Platform |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

**By Application:** - Autonomous Weapons - Cyber Defense - Intelligence, Surveillance, and Reconnaissance (ISR) - Simulation and Training - Logistics and Supply Chain Management

**By Technology:** - Machine Learning - Natural Language Processing - Computer Vision - Others

**By Platform:** - Airborne - Land-based - Naval

**By Region:** - North America - Europe - Asia-Pacific - Latin America - Middle East & Africa

FAQ's

The Global Artificial Intelligence in Defense Market is estimated to generate USD 9.3 billion in revenue in 2024.

The Global Artificial Intelligence in Defense Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 11.7% during the forecast period from 2025 to 2032.

The Artificial Intelligence in Defense Market is estimated to reach USD 22.5 billion by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!