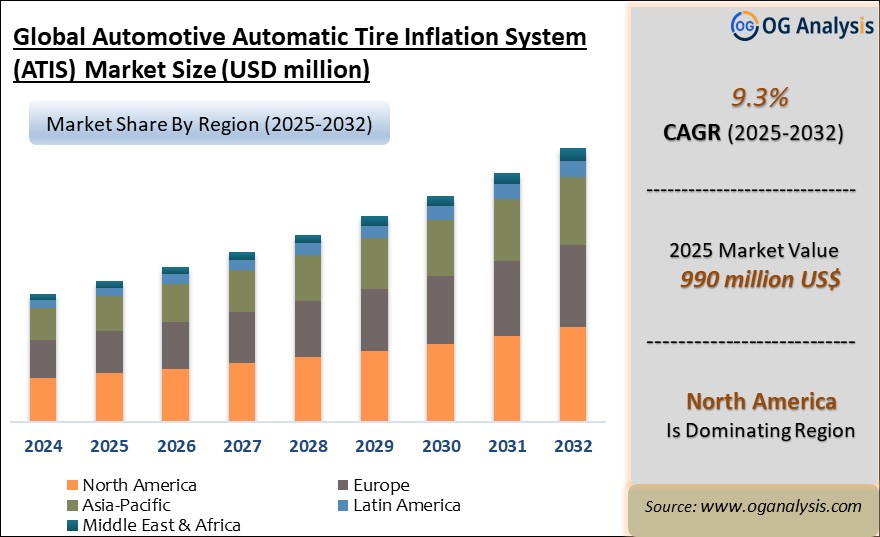

"The Automotive Automatic Tire Inflation System Market Size was valued at $917 million in 2024 and is projected to reach $990 million in 2025. Worldwide sales of Automotive Automatic Tire Inflation System are expected to grow at a significant CAGR of 9.3%, reaching USD 2,255 million by the end of the forecast period in 2034."

Introduction and Overview of the Automotive Automatic Tire Inflation System Market

The Automotive Automatic Tire Inflation System (ATIS) market is rapidly gaining prominence due to the increasing demand for safety, fuel efficiency, and vehicle performance optimization in the automotive industry. ATIS technology allows vehicles to automatically maintain the correct tire pressure, which directly impacts fuel economy, tire lifespan, and vehicle handling. With the growing awareness of the benefits of well-maintained tire pressure, including reducing carbon emissions and improving road safety, ATIS has become a sought-after feature in both commercial and passenger vehicles. Moreover, the rise in long-haul transportation, coupled with stringent government regulations on vehicle safety and fuel efficiency, is driving the adoption of ATIS solutions globally.

The market has witnessed significant growth as manufacturers incorporate ATIS into their vehicle portfolios, particularly in trucks, buses, and heavy-duty vehicles. The increasing focus on reducing vehicular downtime, improving fleet management efficiency, and enhancing tire life expectancy further bolsters the demand for ATIS systems. In addition, the push towards smart vehicles and the integration of advanced technologies such as the Internet of Things (IoT) in automotive systems are contributing to the expansion of the ATIS market. Key players in the market are continuously innovating to improve product reliability and cost-effectiveness, making ATIS solutions more accessible to a broader range of vehicles.

North America is the leading region in the automotive automatic tire inflation system market, powered by stringent vehicle safety regulations, high adoption of advanced commercial vehicle technologies, and the presence of key industry players focused on fleet efficiency and tire performance optimization.

Key Insights

- Automatic tire inflation systems emerged first in demanding off-highway and defense environments, where vehicles operate on rough terrain and tire failures are especially costly. This heritage shaped expectations for ruggedness, redundancy, and fail-safe operation, which now carry over into mainstream commercial road transport applications.

- Fuel savings and lower rolling resistance represent a core economic driver, as even modest underinflation can increase energy consumption and emissions. By maintaining pressure close to optimal targets, these systems support fleet sustainability goals, reduce fuel spend, and complement broader aerodynamics and powertrain efficiency measures.

- Tire life extension is another critical factor, since underinflated or unevenly inflated tires wear faster and are more prone to blowouts. Automatic inflation helps equalize pressure across axles and vehicle combinations, reducing irregular wear patterns and improving casing quality, which is particularly important for retreading strategies.

- Safety and compliance are growing in importance as regulators and insurers pay closer attention to tire condition in heavy commercial fleets. Automatic tire inflation, combined with pressure and temperature monitoring, provides traceable data that can support preventive maintenance, reduce roadside incidents, and demonstrate due diligence in fleet safety management.

- OEMs increasingly view automatic tire inflation systems as an integrated element of chassis and axle design rather than a bolt-on accessory. Dedicated channels in axles and hubs, optimized routing of air lines, and harmonized electronic interfaces support better reliability, shorter installation times, and easier service throughout the vehicle life.

- The aftermarket remains a significant channel, especially for large fleets seeking to retrofit existing assets to capture efficiency gains without waiting for new vehicle purchases. Retrofit kits, modular control units, and standardized installation procedures lower adoption barriers for operators with mixed fleets and varying duty cycles.

- Digitalization and connectivity are reshaping value propositions, as automatic tire inflation systems feed data into telematics, fleet platforms, and maintenance management tools. Fleet managers can monitor pressure trends, identify recurring issues on specific routes or vehicles, and schedule service proactively rather than reacting to breakdowns and roadside repairs.

- Product development is moving toward lighter, more compact components that fit within tight packaging envelopes and are compatible with electric axles and hub motors. Lower parasitic losses, minimized noise, and optimized power consumption are key design considerations as electrified commercial vehicles and trailers gain share.

- Regional dynamics matter, with adoption strongest in markets where long-haul trucking, strict safety and emission rules, and high labor costs amplify the benefits of automation. In emerging markets, awareness building, local service networks, and financing solutions play important roles in accelerating uptake among cost-sensitive operators.

- Looking forward, the Global Automotive Automatic Tire Inflation System Market is expected to benefit from broader trends in smart mobility, autonomous trucking, and connected fleets. Suppliers that combine robust mechanical designs with strong electronics, software integration capabilities, and lifecycle support services are best positioned to capture long-term growth and participate in evolving vehicle platform strategies.

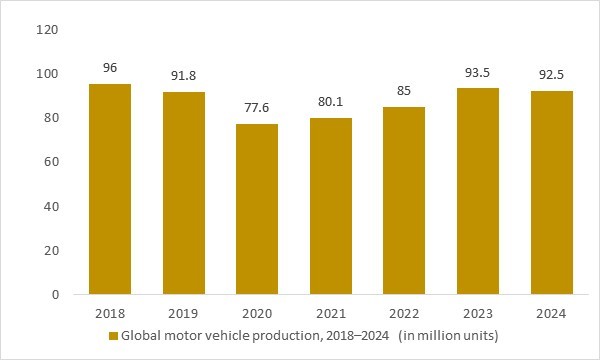

Global motor vehicle production, 2018–2024 (in million units)

Figure: Global motor vehicle production (million units), 2018–2024 – a key parc and tire-volume driver supporting adoption of automotive automatic tire inflation systems.

- Rising global motor vehicle production from 2018 to 2024 expands the active vehicle parc and associated tire volumes. This structural increase in commercial trucks, trailers and buses is encouraging OEMs and fleet operators to adopt automatic tire inflation systems to improve safety, uptime and fuel efficiency.

Regional Insights

North America Automotive Automatic Tire Inflation System Market

In North America, the automotive automatic tire inflation system market is anchored by a large heavy-duty trucking and trailer base, long-haul freight corridors, and strong fleet focus on fuel savings and uptime. Adoption is most advanced on trailers and vocational trucks, where automatic inflation has been proven to cut fuel consumption, extend tire life, and reduce roadside breakdowns. OEMs integrate systems at the axle and suspension level, while retrofit kits target mixed and aging fleets looking for fast payback on operating expenses. Tight safety and emissions regulations, together with widespread TPMS mandates, help create awareness of tire pressure management and support complementary adoption of ATIS solutions. Partnerships between tire makers, telematics providers, and ATIS specialists are expanding, enabling connected offerings that blend real-time pressure control with analytics and predictive maintenance for large fleets.

Europe Automotive Automatic Tire Inflation System Market

In Europe, demand for automatic tire inflation systems is shaped by dense freight networks, high fuel and labor costs, and stringent safety and CO₂ reduction targets. While regulatory focus has historically centered on TPMS for heavy commercial vehicles, fleets are increasingly exploring ATIS as a way to go beyond monitoring and actively control tire pressure across complex truck–trailer combinations. Regional OEMs and Tier-1 suppliers integrate tire pressure control into advanced chassis, axle, and braking platforms, aligning with EU rules on tire performance, rolling resistance, and emissions. Cross-border operations and tight delivery windows emphasize reliability and reduced downtime, making automated inflation attractive for long-haul, tanker, and high-value cargo fleets. As low-emission zones, toll differentiation, and fuel-efficiency initiatives expand, ATIS is gaining recognition as part of broader eco-driving and fleet-optimization strategies.

Asia-Pacific Automotive Automatic Tire Inflation System Market

Asia-Pacific is a fast-growing region for automatic tire inflation systems, driven by rising freight activity, expanding logistics networks, and modernization of commercial vehicle fleets. Large markets such as China and India are upgrading truck and trailer specifications, with attention to fuel economy, tire costs, and safety on increasingly congested highways. International and regional suppliers are targeting OEM fitment on premium tractors and trailers, as well as aftermarket retrofits for long-haul and mining fleets that operate under harsh conditions. As regional TPMS and safety regulations evolve, fleets are beginning to pair monitoring with active inflation to stabilize performance over long routes and variable loading. Growing interest in connected fleet platforms and telematics in key APAC economies also supports adoption of smarter ATIS solutions that integrate pressure data, alerts, and maintenance workflows.

Rest of the World Automotive Automatic Tire Inflation System Market

In the rest of the world, including Latin America, the Middle East, and Africa, the market for automotive automatic tire inflation systems is at an earlier but steadily developing stage. Heavy-duty fleets in oil and gas, mining, construction, and cross-border logistics are early adopters, as they face extreme operating conditions, long distances, and costly downtime. Much of the current activity is concentrated in high-spec fleets and international operators that import trucks and trailers already equipped with ATIS or retrofit systems from global suppliers. Local awareness of tire-related fuel and safety losses is increasing, prompting interest in technologies that can stabilize tire pressures when service infrastructure is sparse. Over time, as road networks, regulatory frameworks, and digital fleet-management tools expand, ATIS is expected to move from niche to more broadly accepted efficiency equipment in targeted segments.

Market Scope

| Parameter | Global Automotive Automatic Tire Inflation System Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Central Tire Inflation

- Continuous Tire Inflation

- Others

By Technology Node

- 10/7/5 nm

- 16/14 nm

- 20 nm

- 28 nm

- 45/40 nm

- Others

By Component

- Rotary Union

- Compressor

- Pressure Sensor

- Air Delivery System

- Other

By Foundry Type

- Pure Play Foundry

- IDMs

By Vehicle Type

- On-Highway Vehicle(Light Duty and Heavy Duty Vehicle)

- Off-Highway Vehicle(Agriculture tractors and Construction Vehicle)

- Electric heavy-duty vehicles(Battery Electric Vehicle,Plug-In Hybrid Electric Vehicle and Fuel Cell Electric Vehicle)

By Application

- Communication

- Consumer Electronics

- Computer

- Automotive

- Others

By Sales Channel

- OEM

- Aftermarket

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Covered

- Michelin

- Goodyear

- Bridgestone

- Continental AG

- Dana Incorporate

- Hendrickson

- Pressure Systems International (PSI)

- Nexter Group

- Meritor, Inc.

- Aperia Technologies, Inc.

- STEMCO (EnPro Industries)

- Haldex AB

- WABCO (ZF Group)

FAQ's

The Global Automotive Automatic Tire Inflation System Market is estimated to generate USD 917 million in revenue in 2024.

The Global Automotive Automatic Tire Inflation System Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.3% during the forecast period from 2025 to 2032.

The Automotive Automatic Tire Inflation System Market is estimated to reach USD 1867.8 million by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!