"The Automotive Door Hinges Market Size was valued at $ 6.7 billion in 2026. Worldwide sales of Automotive Door Hinges are expected to grow at a significant CAGR of 7.5%, reaching $ 12.0 billion by the end of the forecast period in 2034."

The Automotive Door Hinges Market is a specialized segment of vehicle body hardware, closure systems, structural components, and automotive safety parts, serving passenger cars, commercial vehicles, electric vehicles, luxury vehicles, SUVs, pickup trucks, buses, and specialty vehicles. Automotive door hinges are mechanical components that connect vehicle doors to the body structure and enable controlled opening, closing, alignment, and load-bearing performance. These hinges are used in side doors, tailgates, liftgates, sliding doors, hood systems, trunk lids, and specialty access panels. Key product types include conventional door hinges, concealed hinges, strap hinges, forged hinges, stamped hinges, sliding door hinges, check-arm integrated hinges, liftgate hinges, and lightweight aluminum or composite-compatible hinge systems.

The market is gaining traction as automakers focus on vehicle safety, lightweighting, durability, design flexibility, corrosion resistance, and improved passenger convenience. Automotive door hinges are increasingly designed to support higher door loads, better crash performance, precise fit and finish, smoother operation, and compatibility with advanced body architectures. Key trends include lightweight hinge materials, compact hinge designs, high-strength steel and aluminum hinges, anti-corrosion coatings, automated assembly-compatible hinges, electric vehicle-specific body hardware, power sliding door integration, and improved hinge durability for premium and utility vehicles. Growth is supported by passenger vehicle production, SUV and crossover demand, electric vehicle platforms, commercial vehicle replacement, rising focus on vehicle aesthetics, and increasing use of automated manufacturing. However, challenges include raw material price volatility, strict quality requirements, cost pressure from OEMs, corrosion and fatigue performance needs, and competition from integrated closure system suppliers. The competitive landscape includes automotive hardware manufacturers, body component suppliers, metal forming companies, hinge specialists, Tier suppliers, and vehicle closure system providers.

Regional Analysis

North America Automotive Door Hinges Market

North America represents a mature and quality-driven market for automotive door hinges, supported by strong demand from passenger vehicles, pickup trucks, SUVs, commercial vans, and electric vehicles. The United States is the leading market, where OEMs and Tier suppliers focus on durable hinge systems that support heavier doors, large tailgates, sliding doors, corrosion resistance, crash safety, and precise body-panel alignment. Market dynamics are shaped by SUV and pickup popularity, EV platform launches, automated assembly requirements, aftermarket replacement demand, and the need for lightweight yet strong closure hardware. Opportunities remain strong in aluminum hinges, high-strength steel hinges, anti-corrosion coatings, liftgate hinges, power sliding door mechanisms, and EV-specific closure systems. Growth is expected to remain steady as vehicle production, fleet replacement, and connected manufacturing investments support demand for precision-engineered body hardware.

Asia Pacific Automotive Door Hinges Market

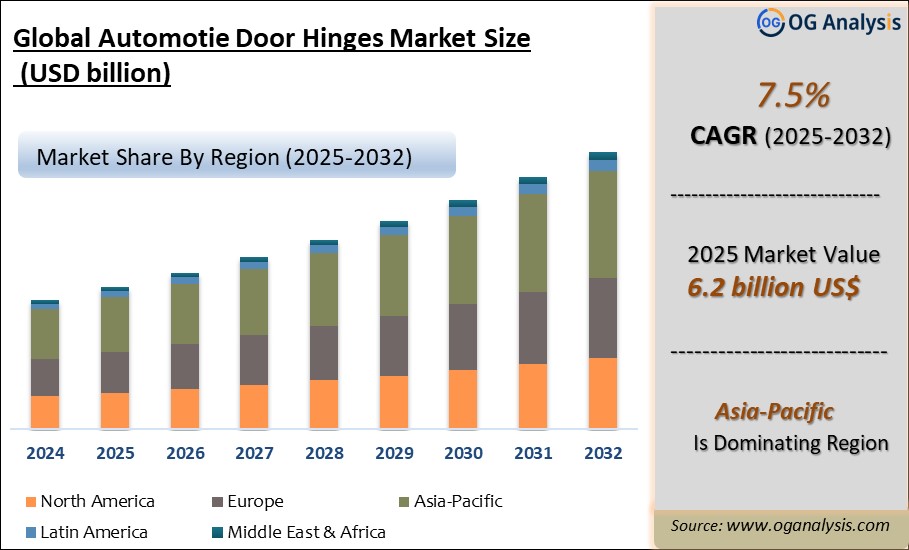

Asia Pacific is the largest and fastest-growing region in the Automotive Door Hinges Market, driven by high vehicle production, expanding EV manufacturing, growing middle-class vehicle ownership, and strong automotive component supply chains. China, Japan, India, South Korea, Thailand, Indonesia, and Vietnam are key markets, with China leading due to its large passenger vehicle and electric vehicle manufacturing base. OICA reported that global vehicle production increased in 2025 and that automotive growth increasingly shifted toward Asia, reinforcing the region’s manufacturing importance. Demand is strong for conventional side-door hinges, hood hinges, tailgate hinges, sliding door hinges, and lightweight hinge assemblies used in passenger cars, SUVs, MPVs, electric vehicles, and commercial vehicles. Future opportunities will be supported by EV body architecture innovation, localized component manufacturing, cost-efficient metal forming, and increasing demand for premium fit-and-finish quality.

Europe Automotive Door Hinges Market

Europe’s Automotive Door Hinges Market is shaped by premium vehicle manufacturing, strict quality standards, vehicle safety requirements, electrification, lightweighting, and advanced body design. Germany, France, the United Kingdom, Italy, Spain, Sweden, Czech Republic, Poland, and Hungary are important markets, supported by strong OEM and Tier supplier ecosystems. European automakers require hinge systems that deliver precision alignment, corrosion resistance, low noise, long service life, and compatibility with lightweight vehicle platforms. Demand is increasing for aluminum hinges, concealed hinges, optimized steel hinges, anti-corrosion surface treatments, and hinges designed for electric SUVs, compact EVs, and premium mobility models. The IEA expects electric car sales in Europe to grow further in 2025, supporting continued redesign of closure systems for EV platforms and aerodynamic body structures. Growth will remain steady as automakers prioritize lighter components, automated assembly, sustainability, and high-quality vehicle closure performance.

Middle East & Africa Automotive Door Hinges Market

The Middle East & Africa Automotive Door Hinges Market is developing gradually, supported by vehicle imports, commercial vehicle demand, replacement parts, fleet maintenance, and growing automotive assembly activity in selected countries. Gulf countries, particularly Saudi Arabia and the UAE, are important demand centers due to premium vehicle ownership, SUV demand, and commercial fleet expansion. South Africa, Egypt, Morocco, Kenya, and Nigeria offer opportunities through local assembly, aftermarket distribution, and growing demand for passenger cars, vans, buses, and light commercial vehicles. Automotive door hinges in this region must withstand heat, dust, corrosion, frequent use, and harsh road conditions, making durability and coating quality important purchasing factors. However, limited local component manufacturing, import dependence, price sensitivity, and uneven vehicle production capacity can affect market development. Future growth will be supported by vehicle parc expansion, aftermarket replacement demand, regional assembly programs, and stronger dealer and component distribution networks.

South & Central America Automotive Door Hinges Market

South & Central America is an emerging market for automotive door hinges, supported by vehicle production, aftermarket replacement, commercial transportation, and demand for affordable passenger vehicles. Brazil and Mexico are the leading markets, with Mexico benefiting from its integration with North American automotive supply chains and Brazil supported by its domestic vehicle manufacturing base. Argentina, Chile, Colombia, Peru, and Central American countries offer gradual opportunities through replacement parts, vehicle imports, and light commercial vehicle demand. Market dynamics are influenced by economic volatility, currency movement, steel and aluminum costs, import tariffs, and OEM production cycles. Opportunities are strongest in cost-efficient stamped hinges, corrosion-resistant hinges, replacement hinge assemblies, commercial vehicle door hardware, and body hardware for SUVs and utility vehicles. Future demand will improve as regional vehicle production stabilizes, aftermarket networks expand, and automakers localize more component sourcing.

Key Insights

- Passenger vehicle production is one of the strongest growth drivers for the Automotive Door Hinges Market. Cars, SUVs, crossovers, and light trucks require multiple hinge systems across side doors, tailgates, hoods, and trunk lids, creating steady demand from OEM production lines.

- SUVs and crossover vehicles are important demand contributors because they often use heavier doors, larger tailgates, and stronger closure components. These vehicles require durable hinge systems that support weight, alignment, repeated use, and long-term reliability.

- Electric vehicles are creating new opportunities for automotive door hinge suppliers. EV platforms often use new body structures, lightweight materials, flush surfaces, aerodynamic styling, and premium access designs that require customized hinge engineering and precise integration.

- Lightweighting is a major technology trend as automakers seek to reduce vehicle weight and improve efficiency. Aluminum hinges, optimized steel designs, and advanced forming techniques help reduce component weight without compromising strength, durability, or safety.

- Door alignment and fit quality are critical buying factors for OEMs. Hinges must support accurate panel gaps, smooth opening and closing, low noise, vibration control, and consistent performance throughout the vehicle lifecycle.

- Corrosion resistance is essential because hinges are exposed to moisture, road salt, dust, temperature changes, and repeated mechanical stress. Coatings, surface treatments, stainless materials, and improved sealing practices are important for long-term durability.

- Commercial vehicles provide steady aftermarket and OEM demand. Vans, trucks, buses, delivery vehicles, and utility vehicles require robust hinge systems for frequent door operation, high load-bearing needs, and harsh working environments.

- Power doors and sliding doors are supporting advanced hinge development. Minivans, premium vehicles, mobility vehicles, and commercial vans increasingly use powered sliding doors, soft-close systems, and automated access features that require reliable hinge and guide mechanisms.

- Manufacturing precision is becoming increasingly important as automakers adopt automated body assembly and tighter quality standards. Suppliers must deliver hinges with consistent dimensions, weldability, coating quality, and compatibility with robotic installation.

- Future market growth will be shaped by vehicle production recovery, SUV and EV demand, lightweight body structures, premium closure systems, automated assembly, corrosion-resistant materials, and durability-focused engineering. Suppliers offering strong design support, cost-efficient production, high-quality coatings, and application-specific hinge solutions are expected to remain competitive.

Global Automotive Door Hinges Market Analysis 2025-2032: Industry Size, Share, Growth Trends, Competition and Forecast Report

Report Scope

| Parameter | Automotive Door Hinges Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Type Process, By Material, By Vehicle Type and By Sales channel |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Integral type

- Separable type

By Type of Process

- Press

- Rolling

- die-casting

- Stamping

- Injection molding

- Extrusion

- Other

By Material

- Steel

- Aluminum

- Brass

- Composite

By Vehicle Type

- Passenger Cars (PCs)

- Commercial Vehicles (CVs)

By Sales Channel

- OEM

- Aftermarket

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Market Players

1. Dura Automotive Systems, Inc.

2. Magna International Inc.

3. Multimatic Inc.

4. Aisin Seiki Co., Ltd

5. Gestamp Group

6. Multimatic Inc.

7. Brano Group

8. DEE Emm Giken

9. ER Wagner

10. Midlake Products & Mfg. Company Inc.

11. Pinet Industrie

12. Monroe Engineering

13. Reell Precision Manufacturing Inc.

14. The Paneloc Corporation

15. Saint Gobain

Recent Developments

April 2026 – Edscha announced a new state-of-the-art site in Hefei, China, with operations expected to start in summer 2026. The facility will combine production, R&D, and administration, and will manufacture door hinges, door checks, and tailgate hinges while more than tripling the company’s production capacity in China.

March 2026 – FCA US / Jeep issued a recall for certain 2024–2026 Jeep Wagoneer S vehicles due to rear hinge covers that may not be properly clipped into position and may detach from the vehicle. The remedy involves inspection, repair, or replacement of the hinge cover, highlighting the importance of hinge-cover retention and assembly quality in vehicle closure systems.

December 2025 – Ford Motor Company recalled certain Ford Escape vehicles in the United States over improperly secured liftgate hinge covers that could detach while driving. Dealers were instructed to inspect, reinstall, or replace missing hinge covers as required.

June 2025 – Edscha and Gestamp showcased automotive body and closure innovations at Automotive Engineering Exposition 2025 in Japan. Edscha introduced its Active Frunk system for electric vehicles, combining automatic front-hood opening and closing with an active pedestrian protection hinge.

May 2025 – Edscha and Gestamp presented new mobility technologies at Auto Shanghai 2025, including Edscha’s Power Sliding Door system designed to improve user comfort and safety. The development reflects growing demand for powered closure systems and advanced door mechanisms in EVs and premium vehicles.

April 2025 – Stabilus secured a major order from a Chinese automaker for more than 400,000 electromechanical door drive systems per year, with production starting from 2026. The company’s system includes an electric door drive, ECU, radar technology, and proprietary software for automatic side-door control.

April 2025 – Brose showcased smart vehicle access and door-system technologies at Auto Shanghai 2025, including intelligent access features, smart digital key functions, high-end latch technologies, and a lightweight door module made from recycled materials.

March 2025 – Toshiba Electronic Devices & Storage started mass production of the TB9103FTG gate driver IC for automotive brushed DC motors used in power backdoors, power slide doors, latch motors, lock motors, power windows, and power seats. The launch supports smaller and more reliable electrified closure systems.

January 2025 – Edscha and Gestamp displayed closure and body innovations at Bharat Mobility Global Expo 2025 in India, including Edscha’s Active Frunk solution for EVs that combines a fully automatic front-lid system with a hinge for active pedestrian protection.

FAQ's

Common types include butt hinges, concealed hinges, continuous (piano) hinges, and strap hinges, with each type suited for different vehicle designs and door functions (e.g., standard, sliding, gull-wing doors).

Asia-Pacific leads the market, driven by large-scale automotive production in China, India, Japan, and South Korea. Europe and North America follow, supported by established automotive manufacturing hubs and demand for high-end vehicles.

Key growth drivers include rising global vehicle production, growing demand for lightweight and durable components, increased adoption of luxury vehicles with advanced door designs, and technological innovations in automotive door systems.

The Automotive Door Hinges Market is estimated to reach USD 10.3 billion by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!