"The Automotive Heat Shield Market was valued at $14.83 billion in 2026 and is projected to reach $24.4 billion by 2034, growing at a CAGR of 6.43%."

The automotive heat shield market covers thermal management components designed to protect vehicle systems and occupants from high temperatures generated by exhaust lines, turbochargers, catalytic converters, batteries, and power electronics. Heat shields reduce radiant and convective heat transfer, prevent thermal degradation of nearby parts, and support compliance with durability, safety, and emissions requirements. Core applications include underbody and exhaust heat shields, turbo and manifold shields, catalytic converter shields, firewall and tunnel insulation, and increasingly, thermal protection around EV battery packs, inverters, e-motors, and charging components. End users span passenger cars, light commercial vehicles, heavy trucks, and off-highway platforms, with demand influenced by powertrain design, packaging density, and regulatory requirements for emissions and safety. OEMs and Tier suppliers prioritize lightweighting, heat resistance, durability under vibration and corrosion, ease of assembly, and compatibility with high-volume manufacturing, while also managing cost and recyclability constraints in increasingly sustainability-focused vehicle programs.

Market momentum is being shaped by tighter emissions standards, downsized turbocharged engines that generate higher localized heat loads, and growing electrification that shifts thermal management needs toward batteries and high-voltage systems. Latest trends include adoption of multi-layer composite shields, advanced stainless and aluminum structures, coated and embossed designs that improve insulation while reducing mass, and increased use of integrated thermal-acoustic solutions to manage both heat and NVH. For EVs, demand is rising for flame-resistant and thermally stable barrier materials that support battery safety strategies and protect adjacent structures from heat events, while also helping manage routine thermal loads during fast charging and high-power operation. Competitive dynamics include global thermal management specialists, Tier-1 component suppliers, and materials innovators; differentiation increasingly rests on co-design capability with OEMs, simulation and validation strength, material innovation, manufacturing efficiency, and the ability to supply regionally with consistent quality. Looking ahead, thermal shielding will remain essential across both ICE and electrified platforms as packaging tightens and thermal loads rise, making lightweight, high-performance, and cost-effective solutions central to vehicle durability and safety.

Automotive Heat Shield MarketKey Market Insights

-

Thermal load growth from turbocharging and tighter packaging sustains demand Downsized engines and higher underhood power density increase the need for targeted shielding. Current vehicles require more localized protection around turbochargers and aftertreatment. Future platforms will further tighten packaging, increasing heat management complexity. Suppliers that optimize performance per gram gain advantage.

-

Emissions and aftertreatment systems remain a major heat-shield demand anchor Catalytic converters and particulate filters operate at high temperatures and require underbody shielding. Current regulations push more complex aftertreatment layouts and closer-coupled components, raising heat exposure. Future emission control strategies will sustain shielding needs in ICE and hybrid fleets. Durability and corrosion resistance remain key requirements.

-

Electrification shifts shielding toward batteries and high-voltage components EVs and hybrids introduce new thermal protection needs around battery packs, inverters, e-motors, and charging hardware. Current focus includes protecting adjacent structures and improving safety margins under abnormal heat events. Future growth will emphasize materials that combine thermal insulation with flame resistance and low smoke. EV platform volumes will expand this segment materially.

-

Lightweight multi-layer and composite shields gaining share Traditional stamped metal shields face weight and packaging limits. Current programs increasingly use multi-layer constructions and composites to improve insulation with less mass. Future designs will balance thermal performance, cost, and recyclability. Material selection becomes a major differentiation lever.

-

Integration of thermal and acoustic functions increasing value per part OEMs seek components that reduce both heat transfer and noise transmission. Current solutions combine insulation layers with acoustic barriers to simplify assemblies and reduce part count. Future platforms will favor integrated systems to cut complexity and assembly time. This supports higher-value engineered solutions versus commodity shields.

-

Manufacturing efficiency and forming technology influence competitiveness High-volume platforms require repeatable forming, joining, and coating processes with tight tolerances. Current competition emphasizes embossing patterns, air gaps, and coatings that improve thermal resistance. Future productivity gains will come from improved automation and standardized modules. Suppliers with strong industrialization capability win global platforms.

-

Material innovation driven by higher temperature cycles and durability expectations Heat shields must withstand repeated thermal cycling, vibration, water, salt, and debris impacts. Current trends include improved alloys, coatings, and fiber-based insulation layers with higher stability. Future requirements may tighten with longer warranty expectations and harsher duty cycles. Testing and validation strength becomes more important.

-

Regional platform strategies increase demand for localized supply footprints OEMs increasingly require local sourcing for cost and resilience. Current suppliers expand regional manufacturing to support global platforms and reduce logistics risk. Future procurement will further reward suppliers with multi-region capacity and consistent quality systems. Localization also improves responsiveness to design changes.

-

Cost pressure remains high, pushing design-to-cost and modularization Heat shields are often cost-sensitive components, especially in mass-market vehicles. Current suppliers must deliver performance improvements without significant cost increases. Future designs will use modular patterns and shared parts across platforms to reduce engineering and tooling costs. Value engineering remains central to winning bids.

-

Safety and fire-risk considerations increasing attention to thermal barriers Beyond comfort and durability, thermal protection supports safety by reducing risk of heat damage and fire. Current EV programs in particular demand more rigorous thermal barrier performance and validation. Future standards and OEM requirements may tighten around flame resistance and thermal event containment. This elevates material compliance and system-level testing.

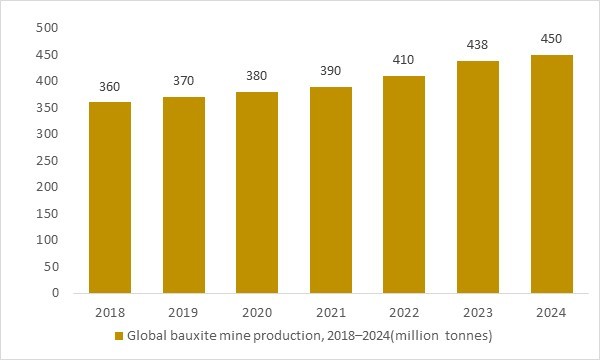

Global bauxite mine production, 2018–2024(million tonnes)

Figure: Global bauxite mine production has risen steadily from the late 2010s through 2023, with 2024 output expected to remain at historically high levels. This expanding ore supply underpins primary aluminium availability for lightweight metallic heat shields used in exhaust systems, engine bays and increasingly in battery and power-electronics enclosures. OG Analysis estimates, based on international bauxite mining statistics, highlight how upstream raw-material trends support long-term capacity for aluminium-intensive heat shield solutions in the global automotive heat shield market.

-

Global bauxite production—the upstream raw material base for aluminium used in automotive heat shields—has steadily expanded from around 350–360 million tonnes in 2018 to 438 million tonnes in 2023, with 2024 output estimated between 421 and 450 million tonnes. This sustained growth in ore availability strengthens aluminium sheet and foil supply, enabling OEMs to meet rising thermal protection requirements in exhaust systems, turbochargers, engine bays and EV battery enclosures. As vehicles incorporate higher power densities and lightweighting targets, the need for advanced aluminium-based heat shields increases across ICE, hybrid and electric platforms. The consistent upward trend in bauxite supply therefore underpins long-term manufacturing capacity and supports market stability for global automotive heat shield producers.

Regional Insights

North America Automotive Heat Shield Market

North America’s automotive heat shield market is driven by a large installed base of light trucks and SUVs, sustained production of turbocharged ICE and hybrid platforms, and increasing thermal management requirements in EV programs. Market dynamics emphasize heat protection around exhaust and aftertreatment systems for ICE/hybrids, alongside rising demand for thermal barriers near battery packs, inverters, and high-voltage cabling as electrification grows. Lucrative opportunities exist in lightweight multi-layer shields that reduce mass without sacrificing durability, integrated thermal-acoustic solutions that simplify assemblies, and EV-focused materials with higher thermal stability and flame resistance to support battery safety strategies. Latest trends include more localized shielding for tight packaging, improved coatings and embossing patterns to enhance insulation, and stronger co-design with OEMs using simulation to shorten development cycles. Forecast momentum remains favorable as thermal loads increase and vehicle packaging tightens, while recent developments center on expanding regional supply footprints, adoption of advanced composite and multi-layer structures, and greater alignment of heat shield design with platform-wide thermal management architectures.

Asia Pacific Automotive Heat Shield Market

Asia Pacific’s automotive heat shield market is shaped by high vehicle production volumes, rapid adoption of small-displacement turbocharged engines in many markets, and fast-growing EV output led by China, with strong supply chain depth for metals and thermal materials. Market dynamics include high demand for cost-optimized underbody and exhaust shielding in mass-market vehicles, increasing complexity in aftertreatment layouts, and accelerating growth of EV thermal protection components for batteries and power electronics. Lucrative opportunities are strongest in scalable, high-throughput manufacturing of lightweight shields, localized supply for OEM platform programs, and advanced thermal barrier materials that address EV safety requirements while maintaining cost targets. Latest trends include greater use of multi-layer constructions, integrated thermal-acoustic parts for cabin comfort, and supplier investment in automation and forming technologies to improve consistency and productivity. Forecast prospects remain strong as production scales and electrification expands, while recent developments highlight rapid material innovation, tighter integration with platform thermal simulations, and increasing OEM focus on standardized modules that can be deployed across multiple models to reduce tooling and engineering complexity.

Europe Automotive Heat Shield Market

Europe’s automotive heat shield market is influenced by stringent emissions and durability expectations, high penetration of turbocharged powertrains, and accelerating electrification that shifts thermal management priorities toward batteries and high-voltage systems. Market dynamics emphasize advanced aftertreatment heat management for remaining ICE/hybrid fleets, plus increased demand for EV thermal barriers that support safety, passenger comfort, and reliable performance in fast-charging and high-load use cases. Lucrative opportunities exist in lightweight, recyclable designs aligned with sustainability goals, engineered multi-layer shields that deliver higher thermal performance in compact packaging, and materials that combine thermal insulation with acoustic attenuation to improve cabin refinement. Latest trends include greater use of simulation-led co-engineering, integration of heat shielding with underbody aerodynamics and NVH targets, and adoption of higher-performance coatings and composites where temperature cycling is severe. Forecast momentum remains positive as OEMs redesign platforms around centralized thermal strategies, while recent developments center on broader deployment of EV-focused barrier materials, increased modularization across platforms, and deeper supplier involvement early in vehicle architecture to optimize thermal protection at system level.

Middle East & Africa Automotive Heat Shield Market

Middle East & Africa’s automotive heat shield market is smaller but strategically shaped by harsh climate conditions, long-distance driving profiles, and a vehicle mix that includes high heat-load SUVs, commercial vehicles, and imported models with varied thermal architectures. Market dynamics emphasize durability under high ambient temperatures, dust exposure, and demanding duty cycles, increasing the importance of corrosion resistance, robust fastening, and long-life insulation performance. Lucrative opportunities exist in heat shielding for commercial fleets and heavy-duty applications, aftermarket replacement demand where operating conditions accelerate wear, and niche EV thermal protection as premium EV adoption gradually rises in select urban hubs. Latest trends include stronger preference for durable materials and protective coatings, increased attention to cabin heat management, and procurement that favors reliable supply and service support for fleet operators. Forecast development is steady with growth tied to fleet modernization and infrastructure expansion, while recent developments highlight more localized distribution strategies, increased specification focus for high-temperature environments, and gradual introduction of higher-performance thermal barrier solutions as vehicle feature content rises.

South & Central America Automotive Heat Shield Market

South & Central America’s automotive heat shield market is driven by regional production of mass-market passenger vehicles and light commercial fleets, with demand shaped by cost sensitivity, road conditions, and the continued dominance of ICE powertrains while electrification builds gradually. Market dynamics prioritize durable, cost-effective exhaust and underbody shielding that withstands vibration, corrosion exposure, and rough-road debris, with increasing need for localized sourcing and consistent quality to support OEM platforms and service networks. Lucrative opportunities include value-engineered lightweight shields that improve fuel efficiency and packaging flexibility, integrated thermal-acoustic solutions that enhance cabin comfort without adding complexity, and growing aftermarket replacement channels as vehicle parc ages. Latest trends include incremental upgrades in materials and coatings, greater standardization across platforms to reduce tooling and inventory complexity, and supplier efforts to strengthen regional manufacturing footprints. Forecast prospects are positive but country-specific and tied to production cycles and consumer demand, while recent developments center on cost-focused redesigns, improved durability specifications for local conditions, and gradual expansion of EV-related thermal protection in early-adopter markets.

Report Scope

| Parameter | Automotive Heat Shield Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Material Type, By Vehicle Type, By Product Type, By Application, By Sales Channel |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Automotive Heat Shield Market Segments Covered In The Report

By Material Type

- Metallic

- Non-metallic

By Vehicle Type

- Passenger Car

- Light Commercial Vehicle

- Heavy Commercial Vehicle

By Product Type

- Single Shell

- Double Shell

- Sandwich

By Application

- Exhaust System Heat Shield

- Turbocharger Heat Shield

- Under Bonnet Heat Shield

- Engine Compartment Heat Shield

- Under Chassis

By Sales Channel

- OEM

- Aftermarket

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Covered

Autoneum Nittoku Pvt. Ltd., Carcoustics, Dana Incorporated, ElringKlinger AG, Lydall Inc., Morgan Advanced Materials plc, Tenneco Inc., UGN Inc., Covpress Ltd, DuPont de Nemours, Inc., Happich GmbH, Sumitomo riko Co. Ltd., Talbros Automotive Components Ltd., Ningbo Tuopu Group, Zhuzhou Times New Material Technology Co., Ltd., Zircotec Ltd., NICHIAS Corporation, Adient PLC, Aisin Corporation, BorgWarner Inc., Continental AG, Denso Corporation, Hitachi Astemo, Ltd., JTEKT Corporation, Parker Hannifin Corporation, Robert Bosch GmbH, Compagnie de Saint-Gobain S. A, Schaeffler Technologies AG & Co. KG, Siemens AG, Sogefi Group

Recent Industry Developments

-

June 2025: Aegis FibreTech unveiled an ultra-lightweight heat-shield insulation material that is 10× less thermally conductive and 100× less dense than conventional ceramic fire blankets, offering effective protection up to 1000 °C in automotive and motorsport applications.

-

March 2025: Dana Limited launched a new lightweight aluminum heat shield line aimed at improving thermal management in electric vehicles, enhancing performance and range while aligning with sustainability objectives.

-

April 2025: ElringKlinger showcased its ElroSeal™‑G rotary shaft seal at Auto Shanghai—a lightweight sealing solution designed for high-speed electric drivetrains, underscoring innovation in thermal and sealing technologies.

-

April 2025: Alpha Engineered Composites introduced next‑generation thin‑profile textile composite heat shields with enhanced thermo‑oxidative resistance, capable of withstanding rising engine compartment temperatures driven by modern combustion technologies.

-

November 2024: Autoneum inaugurated a new Research & Technology Center in Shanghai focused on next‑gen mobility thermal shielding, including solutions to enhance battery case protection and thermal propagation resistance.

FAQ's

The Automotive Heat Shield Market is estimated to reach $24.4 billion by 2034.

The Global Automotive Heat Shield Market is estimated to generate USD 14.83 billion in revenue in 2026.

The Global Automotive Heat Shield Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.43% during the forecast period from 2025 to 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!