"The Automotive Seat Heater Market valued at $2.3 billion in 2024, is expected to grow by 4.3% CAGR to reach market size worth $3.6 billion by 2034."

"The Global Automotive Seat Heater Market valued at USD 2.3 billion in 2024, is expected to grow by 4.3% CAGR to reach market size worth USD 3.6 billion by 2034."

The Automotive Seat Heater market is experiencing a period of steady growth, driven by increasing consumer demand for enhanced comfort and convenience within vehicles, particularly in colder climates. This report provides a comprehensive analysis of this market, examining the latest trends, drivers, and challenges shaping its future. It explores the diverse range of seat heater technologies, including electric resistance heaters, carbon fiber heaters, and heated massage seats, highlighting their role in enhancing the driving experience and creating a more comfortable and enjoyable environment for passengers.

Market Introduction

Automotive seat heaters provide warmth and comfort to passengers during cold weather, enhancing the driving experience and improving passenger well-being. These heaters are integrated into vehicle seats, often using electrical resistance wires or carbon fiber elements to generate heat. The Automotive Seat Heater market encompasses a wide range of heating systems, varying in design, technology, and features, catering to different vehicle types and consumer preferences. In 2024, the Automotive Seat Heater market witnessed advancements in heating technologies, with manufacturers focusing on improved heating efficiency, faster warm-up times, and the integration of features like massage functions and temperature control settings. These advancements reflect a growing focus on enhancing comfort and creating a more luxurious driving experience.

Market Overview

Building upon the innovations and progress of 2024, the Automotive Seat Heater market is poised for continued growth in 2025 and beyond. The increasing popularity of heated seats across vehicle segments, driven by consumer demand for enhanced comfort and convenience, is a key driver for this growth. Furthermore, the expansion of heated seats into luxury and premium vehicle segments, where comfort and personalized features are highly valued, is contributing to market growth. As automakers strive to provide a more enjoyable and luxurious driving experience, the adoption of heated seats is expected to rise, creating a greater demand for advanced and sophisticated heating technologies.

The Global Automotive Seat Heater Market Analysis Report will provide a comprehensive assessment of business dynamics, offering detailed insights into how companies can navigate the evolving landscape to maximize their market potential through 2034. This analysis will be crucial for stakeholders aiming to align with the latest industry trends and capitalize on emerging market opportunities.

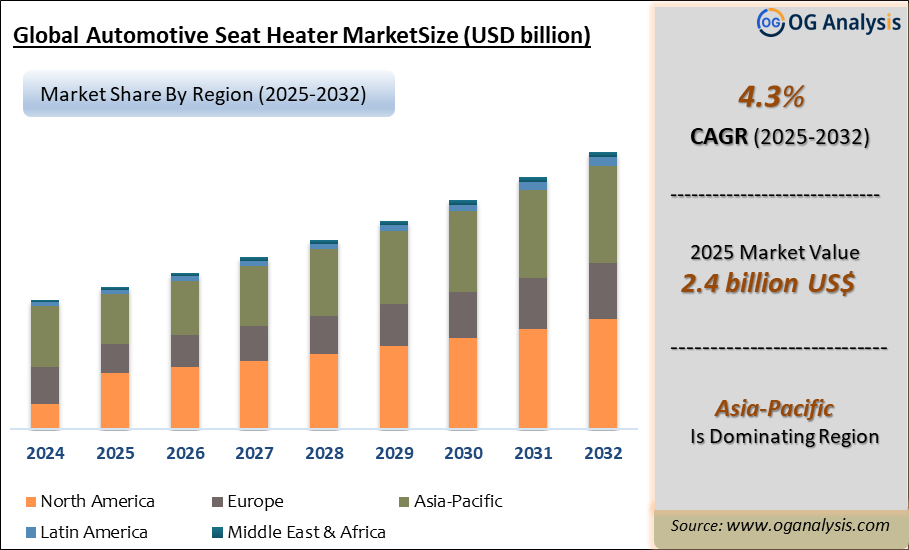

Asia-Pacific is the leading region in the Automotive Seat Heater Market, powered by growing vehicle production, rising consumer preference for enhanced in-car comfort, and increasing adoption of premium features in mid-range vehicles across emerging economies.

Key Insights

- Automotive seat heaters initially emerged as premium features in high-end vehicles and cold-climate markets, but have progressively migrated into mid-range models, reflecting broader consumer expectations for comfort and convenience across price tiers and body styles.

- The primary end-use remains passenger cars and SUVs, where front-seat heating is widely adopted and rear-seat heating is offered in higher trims. Light commercial vehicles and selected heavy trucks increasingly offer driver seat heating to support comfort and alertness on long routes.

- Technology has evolved from simple on–off resistive pads to multi-stage, electronically controlled systems with feedback from temperature sensors. This allows more precise heat regulation, avoids hot spots and improves durability by preventing overheating in specific seat zones.

- Integration with broader climate-control and infotainment systems is a key development, as seat heating can be controlled through central touchscreens, voice commands or mobile apps. This integration supports pre-conditioning, remote activation and personalized driver profiles linked to seat positions and climate settings.

- Electric and hybrid vehicles provide a structural boost to seat heater demand, since localized seat heating can contribute to range optimization by reducing reliance on energy-intensive cabin air heating. This makes seat heaters a strategic comfort feature in many new EV interior designs.

- Materials and design trends focus on thinner, more flexible heating elements, including carbon-fiber and advanced printed-heater technologies, which better conform to complex seat contours and work with lightweight foam and upholstery concepts without compromising comfort or aesthetics.

- Safety, reliability and regulatory compliance are central design considerations, with systems engineered to avoid overheating, short circuits and electromagnetic interference. Robust testing and quality standards are essential, particularly as seat heaters become more pervasive in global platforms.

- The aftermarket remains relevant in regions with large existing vehicle fleets lacking factory-installed seat heating. Retrofit kits for popular models allow dealers and accessory shops to add heating functionality, extending market reach beyond new vehicle sales.

- Regional demand patterns are influenced by climate, income levels and consumer preferences. Cold and temperate regions show higher standard-fit rates, while warmer climates adopt seat heating more selectively, often in combination with ventilation to create year-round, dual-mode seat climate features.

- Looking ahead, the automotive seat heater market is expected to evolve in tandem with smart interiors, advanced seating and connected services. Suppliers that can integrate efficient heating technologies with multi-function seat modules, intuitive controls and vehicle-energy management strategies are likely to capture the most attractive opportunities.

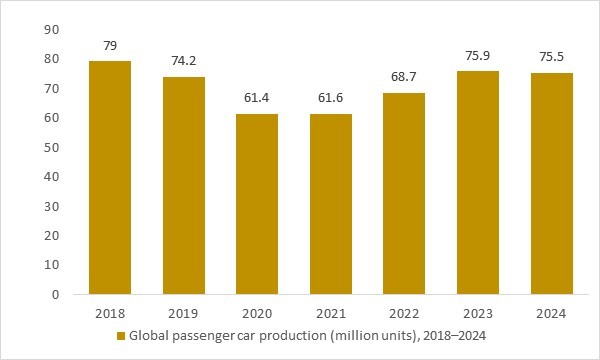

Global passenger car production (million units), 2018–2024

Figure: Global passenger car production increased steadily from 2018 to 2024, rebuilding from the 2020 downturn and expanding the vehicle base for factory-fitted and aftermarket automotive seat heaters. As automakers raise heated-seat fitment across mass-market and premium segments, the growing global car output directly scales the addressable market for heating elements, control modules and related components. The trend underlines how vehicle production recovery and rising comfort-content per car jointly support the long-term demand outlook for the Automotive Seat Heater market.

- Global passenger car production showed a steady rebound from 2018 to 2024, forming a strong and expanding vehicle base for automotive seat heater installations. As manufacturers increase comfort-feature penetration across compact, SUV and premium segments, rising car output directly supports long-term demand for heating elements, control switches and integrated comfort modules. The trend highlights how macro-level vehicle manufacturing growth continues to drive OEM and aftermarket opportunities in the Automotive Seat Heater market.

Regional Insights

North America Automotive Seat Heater Market Analysis

The North American Automotive Seat Heater market experienced significant developments in 2024, driven by the rapid adoption of advanced automotive technologies such as electric vehicle telematics, artificial intelligence, and blockchain solutions. The region has become a hub for innovation in automotive IoT, autonomous driving, and electrification, supported by favorable regulatory frameworks and increasing investments in R&D. The Automotive Seat Heater market is projected to witness robust growth from 2025, fueled by the expansion of EV charging infrastructure, rising demand for smart mobility solutions, and advancements in lightweight materials like copper busbars and tire fabrics. Key players are enhancing their competitive edge through strategic partnerships and product diversification, focusing on sustainability and energy efficiency. The market landscape remains dynamic with a high degree of competition, marked by major OEMs and emerging startups leveraging digital transformation to address evolving consumer demands.

Europe Automotive Seat Heater Market Outlook

In 2024, the European Automotive Seat Heater market showcased a strong focus on sustainability, aligning with stringent environmental regulations and the European Green Deal. Key developments included advancements in electric vehicle components, such as HVAC compressors and turbochargers, alongside innovations in AI-powered automotive technologies and smart mobility solutions. Anticipated growth from 2025 is underpinned by increased electrification in the automotive sector, expansion of bike and scooter-sharing telematics, and the deployment of second-life EV batteries. The region’s automotive giants are collaborating with technology providers to enhance vehicle connectivity and automation. The competitive landscape is shaped by a mix of established players and innovative disruptors, as the market transitions towards circular economy models and next-generation mobility solutions.

Asia-Pacific Automotive Seat Heater Market Forecast

The Asia-Pacific Automotive Seat Heater market recorded exceptional progress in 2024, primarily driven by booming EV adoption, urbanization, and rising disposable incomes. Developments spanned automotive powertrain sensors, AI-driven telematics, and tire cord innovations catering to high-performance vehicles. Growth projections for 2025 are bolstered by government incentives for EV manufacturing, rapid advancements in semiconductor technologies, and the integration of IoT across automotive applications. The competitive landscape is characterized by a strong presence of regional manufacturers and global players expanding operations to cater to this high-potential market. China and India remain focal points, with escalating demand for smart, connected, and sustainable automotive solutions.

Middle East, Africa, Latin America Automotive Seat Heater Market Overview

The Automotive Seat Heater market across the Middle East, Africa, Latin America witnessed steady advancements in 2024, driven by growing investments in automotive refinish coatings, reverse logistics, and railcar leasing for freight transportation. Markets in Latin America and the Middle East are positioning themselves as emerging hubs for smart mobility and automotive blockchain technologies. Expected growth from 2025 will be driven by rising industrialization, improved logistics networks, and adoption of second-life EV batteries to address sustainability challenges. Competitive dynamics in the RoW are defined by niche players catering to local demands and global manufacturers exploring untapped markets. The focus remains on affordability, customization, and fostering innovation to navigate diverse market conditions.

Market Scope

| Parameter | Automotive Seat Heater Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation – Automotive Seat Heater Market

By Vehicle Type

-

Passenger Cars

-

SUVs & Crossovers

-

Light Commercial Vehicles (LCVs)

-

Heavy Commercial Vehicles (HCVs)

By Seat Position

-

Front Seats

-

Rear Seats

-

Third-Row / Specialty Seats

By Technology / Heating Element Type

-

Wire-Based Resistive Heaters

-

Carbon-Fiber / Textile Heaters

-

Printed / Film Heaters

By Control & Integration Level

-

Manual / Two-Stage Controls

-

Multi-Level Electronic Controls

-

Integrated Seat Climate Systems

By Sales Channel

-

OEM (Factory-Fitted)

-

Aftermarket / Retrofit

By Vehicle Propulsion

-

Internal Combustion Engine (ICE) Vehicles

-

Hybrid Electric Vehicles

-

Battery Electric Vehicles (BEVs)

By End-User / Ownership Type

-

Private / Retail Customers

-

Fleet & Corporate Users

Key Companies Covered

- Gentherm Incorporated

- Continental AG

- Lear Corporation

- Kongsberg Automotive ASA

- I.G. Bauerhin GmbH

- Hyundai Transys

- Toyota Boshoku Corporation

- Panasonic Corporation

- Laird Connectivity / Laird Thermal Systems

- Joyson Safety Systems

- Vogelsitze GmbH

- Check Corporation

- Champion Seat Systems

- Rostra Precision Controls, Inc.

- Changchun Faway Automobile Components Co., Ltd.

FAQ's

The Automotive Seat Heater Market is estimated to reach USD 3.6 billion by 2034.

The Global Automotive Seat Heater Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.3% during the forecast period from 2025 to 2034.

The Global Automotive Seat Heater Market is estimated to generate USD 2.4 billion in revenue in 2025

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!