"The Automotive Semiconductor Market valued at $ 56.32 billion in 2026, is expected to grow by 8.1% CAGR to reach market size worth $ 105.03billion by 2034."

The Automotive Semiconductor market is experiencing a period of unprecedented growth, driven by the rapid advancements in vehicle technologies and the increasing adoption of features like autonomous driving, advanced driver-assistance systems (ADAS), electrification, and connectivity. This report provides a comprehensive overview of this dynamic market, exploring the latest trends, drivers, and challenges shaping its future. It examines the diverse range of semiconductors powering the modern vehicle, from microcontrollers and processors to sensors and power management ICs, highlighting their critical role in enabling the transition towards a more intelligent, connected, and sustainable automotive landscape.

Automotive semiconductors are specialized integrated circuits (ICs) designed to meet the unique requirements of the automotive industry, including high reliability, durability, and resistance to harsh environmental conditions. These semiconductors power a wide range of vehicle systems, including engine control units (ECUs), infotainment systems, safety systems, driver assistance features, and electric powertrains. In 2024, the Automotive Semiconductor market witnessed significant developments with the introduction of more powerful and energy-efficient processors, advanced sensors with enhanced accuracy and functionality, and semiconductors with improved cybersecurity features. These advancements are driven by the increasing complexity of vehicle electronics and the growing demand for features like autonomous driving and connected car technologies.

Building on the momentum of 2024, the Automotive Semiconductor market is poised for continued robust growth in 2025 and beyond. The increasing adoption of electric vehicles (EVs), autonomous vehicles, and connected car technologies, combined with a growing emphasis on safety and efficiency, are key drivers for this expansion. Furthermore, the development of advanced semiconductors with enhanced processing power, improved connectivity, and greater energy efficiency is further propelling the market forward. As the automotive industry embraces electrification, autonomy, and connectivity, the demand for specialized semiconductors capable of powering these advanced technologies will continue to rise. This market is at the heart of the transformation of the automotive industry, driving the development of more intelligent, connected, and sustainable vehicles.

The Global Automotive Semiconductor Market Analysis Report will provide a comprehensive assessment of business dynamics, offering detailed insights into how companies can navigate the evolving landscape to maximize their market potential through 2034. This analysis will be crucial for stakeholders aiming to align with the latest industry trends and capitalize on emerging market opportunities.

Key Insights

- Automotive semiconductors have migrated from niche engine-control roles to pervasive use across powertrain, chassis, body, safety, comfort, and infotainment systems, reflecting a long-term shift from mechanical to electronic control that continues to increase silicon content per vehicle.

- Powertrain and body electronics remain foundational segments, with microcontrollers, gate drivers, and analog ICs managing combustion engines, transmissions, lighting, climate control, and convenience functions. Even as electrification grows, these domains still require substantial semiconductor content for control, diagnostics, and efficiency optimization.

- Electrified vehicles add a new layer of demand, particularly for power semiconductors used in traction inverters, onboard chargers, DC–DC converters and battery management systems. The move toward wide bandgap materials such as silicon carbide and gallium nitride enables higher efficiency, higher switching frequencies and more compact designs.

- Advanced driver assistance and automated driving are among the fastest-growing application areas, requiring high-performance processors, AI accelerators, and sensor front-end ICs that can process data from cameras, radar, lidar and ultrasonic sensors in real time under stringent safety requirements.

- The digital cockpit and connected vehicle domains drive demand for application processors, memory, display drivers, audio codecs and connectivity chipsets, as vehicles incorporate larger screens, richer multimedia, voice assistants and seamless integration with smartphones and cloud services.

- Architectural shifts toward centralized and zonal electronics reduce the number of electronic control units but significantly raise compute and networking requirements for remaining controllers, increasing the value of high-integration system-on-chips, Ethernet switches, and high-speed interface ICs.

- Functional safety, cybersecurity and long product lifecycles are critical differentiators in automotive semiconductors, with suppliers required to meet automotive quality standards, offer extended qualification and ensure security features that protect both safety-critical and connected systems.

- The global chip shortage highlighted the strategic importance of automotive semiconductors and prompted OEMs and Tier-1s to rethink sourcing models, pursue longer-term supply agreements, and collaborate more closely with foundries and IDMs on capacity planning and technology roadmaps.

- Regional industrial policies and incentives for local semiconductor manufacturing, especially in major automotive regions, are shaping the future landscape of supply, encouraging diversification of production locations and fostering new entrants and partnerships in automotive chip design and fabrication.

- Looking ahead, the automotive semiconductor market will be driven by convergence of electrification, automation, connectivity and shared mobility, rewarding suppliers that can combine advanced process technologies with automotive-grade reliability, strong software ecosystems and deep collaboration with vehicle-platform engineering teams.

Global industrial robot installations, 2018–2024 (units)

Figure:Global industrial robot installations (units), 2018–2024 – indicating rising automation intensity in automotive and other manufacturing plants, which drives demand for motion-control, power, sensing and safety semiconductors used in vehicle production and assembly equipment.

- Global industrial robot installations have remained at structurally high levels since 2018, reflecting accelerating automation across automotive assembly, body-in-white, painting, and component manufacturing lines. As robots integrate advanced motion-control, power electronics, sensors, and safety-certified processors, this sustained automation momentum directly reinforces demand for automotive-grade semiconductors. The trend highlights how semiconductor consumption is rising not only inside vehicles but also across the broader automotive production ecosystem.

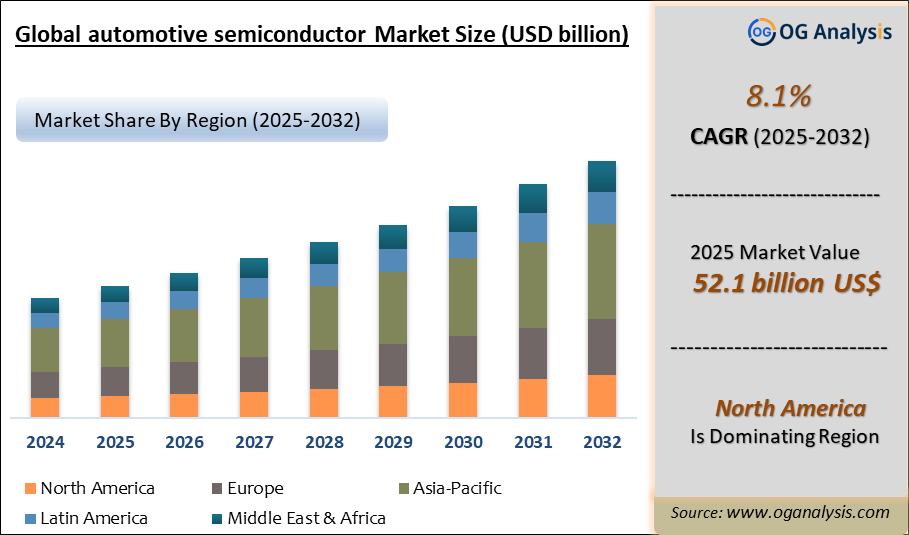

Regional Analysis

North America Automotive Semiconductor Market

North America Automotive Semiconductor Market is driven by strong demand for electric vehicles, connected cars, advanced driver assistance systems, autonomous driving technologies, in-vehicle infotainment, and power electronics. Market dynamics are shaped by the presence of major automakers, semiconductor design companies, EV manufacturers, automotive software developers, and increasing investment in domestic chip supply-chain resilience. Lucrative opportunities exist for companies supplying microcontrollers, power semiconductors, sensors, connectivity chips, memory devices, radar chips, AI processors, and battery management ICs. Latest trends include software-defined vehicles, zonal electrical architectures, silicon carbide power devices, automotive AI computing, advanced safety systems, and secure vehicle connectivity. The forecast outlook remains favorable as automakers continue increasing semiconductor content per vehicle and prioritize electrification, automation, cybersecurity, and supply reliability.

Asia Pacific Automotive Semiconductor Market

Asia Pacific Automotive Semiconductor Market is the most active regional market, supported by large-scale vehicle production, strong electronics manufacturing, rapid electric vehicle adoption, and the presence of major automotive and semiconductor supply chains. Market dynamics are driven by China’s EV ecosystem, Japan and South Korea’s automotive electronics capabilities, Taiwan’s semiconductor manufacturing strength, and expanding vehicle electrification across India and Southeast Asia. The region presents strong opportunities for chipmakers, foundries, OSAT companies, automotive Tier suppliers, battery electronics providers, and sensor manufacturers serving high-volume vehicle platforms. Latest trends include EV power electronics, battery management systems, ADAS chips, smart cockpit processors, connected vehicle modules, and local semiconductor sourcing strategies. The forecast remains positive as regional automakers accelerate innovation in electric mobility, digital interiors, and intelligent driving systems.

Europe Automotive Semiconductor Market

Europe Automotive Semiconductor Market is shaped by strong automotive engineering, premium vehicle production, electric mobility transition, stringent safety regulations, and growing demand for advanced driver assistance and vehicle connectivity. Market dynamics are influenced by the region’s focus on automotive-grade reliability, power electronics for EVs, functional safety, infotainment, radar systems, and semiconductor supply-chain localization. Lucrative opportunities exist for automotive chip suppliers, power semiconductor companies, sensor manufacturers, embedded software providers, and Tier suppliers supporting European OEMs. Latest trends include silicon carbide and gallium nitride adoption, electrified powertrains, software-defined vehicle platforms, centralized computing, digital cockpits, and advanced safety electronics. The forecast outlook remains steady as European automakers continue investing in electrification, automation, sustainability, and semiconductor partnerships to support next-generation vehicle architectures.

Middle East & Africa Automotive Semiconductor Market

Middle East & Africa Automotive Semiconductor Market is developing through rising vehicle electrification interest, connected mobility adoption, luxury vehicle demand, smart transportation projects, and gradual modernization of automotive electronics across regional markets. Market dynamics vary across the region, with Gulf countries showing stronger demand for premium vehicles, EV infrastructure, fleet digitization, and intelligent transport systems, while African markets present opportunities through vehicle connectivity, aftermarket electronics, telematics, and mobility modernization. Companies can benefit by offering cost-effective and reliable semiconductor solutions for infotainment, safety systems, vehicle tracking, EV charging, battery management, and connected fleet applications. Latest trends include smart mobility platforms, automotive telematics, EV charging electronics, advanced infotainment, and digital vehicle services. The forecast remains constructive as regional governments and private players invest in connected transportation and cleaner mobility ecosystems.

South & Central America Automotive Semiconductor Market

South & Central America Automotive Semiconductor Market is supported by vehicle production, aftermarket electronics, connected car adoption, fleet management, infotainment upgrades, and gradual movement toward electrified mobility. Market dynamics are shaped by demand for cost-efficient automotive electronics, safety features, emission-control systems, telematics, powertrain control units, and digital cockpit components across passenger and commercial vehicles. Opportunities exist for semiconductor suppliers, automotive electronics distributors, Tier component manufacturers, telematics providers, EV infrastructure companies, and local assembly partners. Latest trends include increased use of sensors, microcontrollers, vehicle connectivity modules, battery electronics, infotainment chips, and electronic control systems for fuel efficiency and safety. The forecast outlook remains positive as regional automakers and suppliers continue improving vehicle intelligence, electronic content, and readiness for future electric and connected mobility.

Market Scope

| Parameter | Automotive Semiconductor Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Component, By Vehicle Type, By Propulsion Type, By Application |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Automotive Semiconductor Market Segmentation

By Component

- Processors

- Analog ICs

- Discrete Power Devices

- Sensors

- Memory Devices

- Others

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

By Propulsion Type

- Internal Combustion Engine (ICE) Vehicles

- Electric Vehicles (EVs)

- Hybrid Vehicles

By Application

- Powertrain

- Safety Systems

- Body Electronics

- Chassis

- Telematics & Infotainment

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

List Of Companies

Infineon Technologies AG, NXP Semiconductors N.V., STMicroelectronics N.V., Texas Instruments Incorporated, Renesas Electronics Corporation, ON Semiconductor Corporation, Analog Devices Inc., Microchip Technology Inc., Qualcomm Technologies Inc., NVIDIA Corporation, Intel Corporation, Samsung Electronics Co. Ltd., Robert Bosch GmbH, Toshiba Electronic Devices & Storage Corporation, ROHM Co. Ltd., Mitsubishi Electric Corporation, Wolfspeed Inc., Melexis NV, Allegro MicroSystems Inc., MediaTek Inc.

Recent Developments

- May 2026 - onsemi reported improving automotive demand and issued a stronger quarterly outlook, supported by recovery in electric vehicle-related semiconductor demand and renewed momentum for silicon carbide chips used in EV power systems.

- May 2026 - Infineon raised its outlook after reporting improved automotive order intake and stronger growth prospects across its semiconductor portfolio. The update reinforced Infineon’s positioning in automotive power devices, microcontrollers, sensors, and vehicle electrification technologies.

- April 2026 - onsemi and Geely Auto Group expanded their strategic collaboration to integrate onsemi’s silicon carbide technologies across Geely’s next-generation electric and hybrid vehicle platforms. The partnership supports faster EV development and improved powertrain efficiency.

- April 2026 - Bosch and Qualcomm expanded their strategic partnership from cockpit vehicle computers into advanced driver assistance systems. The collaboration focuses on scalable vehicle computers using Snapdragon platforms to support centralized automotive computing architectures.

- April 2026 - Bosch introduced its third-generation silicon carbide power chips for electric vehicles and began supplying samples to global automakers. The development supports higher EV efficiency, improved power conversion, and next-generation electric drivetrain performance.

- March 2026 - NXP advanced its automotive radar portfolio with its third-generation radar transceiver, targeting higher-performance sensing for ADAS and automated driving systems. The development strengthens demand for radar semiconductors in vehicle safety and perception systems.

- March 2026 - Renesas expanded its automotive MCU portfolio with the RH850/U2C family for vehicle control and automotive safety applications. The launch supports domain and zonal architectures, functional safety, and next-generation vehicle electronics requirements.

- March 2026 - STMicroelectronics introduced a new ultra-wideband chip family for automotive and smart device applications. The development supports secure digital key systems, precise positioning, access control, and connected vehicle use cases.

- February 2026 - STMicroelectronics introduced the Stellar P3E automotive microcontroller with AI acceleration for edge intelligence. The MCU is designed to support real-time AI functions, multi-function integration, EV systems, body control, and zonal vehicle architectures.

- February 2026 - Infineon and BMW Group joined forces to support the Neue Klasse software-defined vehicle platform. The collaboration focuses on semiconductor technologies that enable scalable, intelligent, and future-ready vehicle electronics architectures.

- January 2026 - Texas Instruments introduced new automotive semiconductors and development resources, including high-performance computing SoCs and radar technologies for safer and more automated vehicles. The launch supports ADAS, edge AI, vehicle autonomy, and software-defined vehicle development.

FAQ's

The Automotive Semiconductor Market is estimated to generate $ 56.32 billion in revenue in 2026

The Automotive Semiconductor Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 8.1% during the forecast period from 2026 to 2034.

The Automotive Semiconductor Market is estimated to reach $ 105.03 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!