"The Avalanche Radar Market was valued at $ 8.4 billion in 2026 and is projected to reach $ 119.9 billion by 2034, growing at a CAGR of 39.4%."

The Avalanche Radar Market is emerging as a specialized safety technology segment focused on real-time avalanche detection, monitoring, warning, and risk management across snow-covered mountainous regions. Avalanche radar systems are designed to detect moving snow masses during low visibility, night-time conditions, heavy snowfall, and remote terrain situations where conventional visual monitoring or manual observation is limited. These systems are increasingly used by transportation authorities, ski resorts, mountain rail operators, mining companies, hydropower operators, border security agencies, disaster management authorities, and infrastructure owners responsible for roads, tunnels, pipelines, power lines, and alpine facilities. The market is supported by rising awareness of climate-related snowpack instability, growing winter tourism activity, expansion of mountain infrastructure, and the need to reduce risks to people, vehicles, equipment, and critical assets. Avalanche radar is particularly valuable because it provides continuous surveillance and rapid alerts, enabling authorities to close roads, trigger alarms, support controlled avalanche release, and improve emergency response planning. As mountainous regions face increasing operational and safety pressures, radar-based avalanche detection is becoming a more reliable and automated alternative to manual patrols, observation posts, and weather-only forecasting methods.

The competitive landscape of the Avalanche Radar Market includes radar technology companies, geohazard monitoring specialists, remote sensing providers, weather and environmental monitoring firms, defense radar manufacturers, system integrators, and infrastructure safety solution providers. Companies are focusing on long-range radar detection, all-weather monitoring, automated alerts, integration with weather stations, remote cameras, snowpack sensors, geospatial platforms, and emergency communication systems. Key trends include AI-enabled event classification, cloud-based monitoring dashboards, real-time data transmission, mobile radar deployment, multi-sensor avalanche warning networks, and integration with traffic management and railway control systems. Demand is being driven by the need for proactive risk reduction in avalanche-prone corridors, especially where roads, railways, ski areas, mines, and energy assets operate in high-risk terrain. The market also benefits from public safety investments, disaster preparedness programs, insurance and liability concerns, and the modernization of mountain transport infrastructure. However, adoption can be limited by high installation costs, site-specific calibration needs, maintenance challenges in extreme weather, limited technical expertise, and the requirement for reliable power and communication links in remote locations. Overall, the Avalanche Radar Market is expected to remain a high-value niche within the broader geohazard monitoring industry, supported by the shift toward automated, real-time, and data-driven mountain safety systems.

Regional Analysis

North America Avalanche Radar Market

North America Avalanche Radar Market is supported by strong demand from transportation authorities, ski resorts, railway operators, mining companies, hydropower facilities, and public safety agencies operating in avalanche-prone mountain corridors. Market dynamics are shaped by the need for real-time hazard detection, road closure automation, worker safety, winter tourism protection, and resilience of critical infrastructure across alpine and remote terrain. Lucrative opportunities exist for radar technology providers, geohazard monitoring specialists, system integrators, AI analytics firms, and communication network providers offering automated warning and decision-support platforms. Latest trends include integration of avalanche radar with weather stations, traffic systems, cameras, snowpack sensors, and emergency alert networks. The forecast outlook remains positive as infrastructure owners and government agencies increase investment in automated mountain safety systems to reduce risk, improve response speed, and protect high-value assets.

Asia Pacific Avalanche Radar Market

Asia Pacific Avalanche Radar Market is developing steadily across mountainous countries with exposure to snow-slide risks, expanding road networks, hydropower assets, railway corridors, border infrastructure, and winter tourism destinations. Market dynamics are influenced by infrastructure development in high-altitude regions, increasing disaster preparedness, climate-driven snow instability, and the need to protect communities, workers, and transport corridors. The region offers opportunities for companies providing rugged radar systems, remote monitoring platforms, weather-linked warning networks, and integrated geohazard solutions suited to challenging terrain. Latest trends include deployment of multi-sensor avalanche warning systems, use of cloud-based monitoring dashboards, and growing interest in automated detection for road, rail, and hydropower projects. The forecast remains favorable as governments and infrastructure operators strengthen mountain risk management and adopt technology-led safety systems.

Europe Avalanche Radar Market

Europe Avalanche Radar Market is relatively advanced due to the region’s mature alpine infrastructure, high winter tourism activity, established mountain transport networks, and strong public safety culture. Market dynamics are supported by demand from ski resorts, road agencies, railway operators, tunnel authorities, hydropower facilities, and disaster management organizations across avalanche-prone areas. Lucrative opportunities exist for suppliers offering high-accuracy radar detection, AI-based event classification, integrated warning platforms, maintenance services, and consulting support for avalanche risk management. Latest trends include combining radar with infrasound, seismic sensors, weather data, cameras, and traffic control systems to improve alert reliability and operational decision-making. The forecast outlook remains strong as European operators continue upgrading avalanche protection systems, modernizing monitoring networks, and prioritizing safer winter mobility.

Middle East & Africa Avalanche Radar Market

Middle East & Africa Avalanche Radar Market remains a niche but emerging segment, with opportunities concentrated in snow-prone mountain areas, high-altitude transport routes, selective tourism destinations, border zones, and critical infrastructure corridors. Market dynamics are shaped by limited but location-specific avalanche risk, growing need for disaster preparedness, infrastructure protection, and safer mountain access in areas exposed to seasonal snow instability. Companies can find opportunities in compact radar systems, remote sensing, early warning networks, rugged communication solutions, and geohazard monitoring services tailored to isolated or difficult-access environments. Latest trends include broader use of environmental monitoring, climate-risk assessment, and infrastructure safety technologies in mountainous regions. The forecast remains selective, with adoption likely to be project-driven and focused on locations where avalanche risks threaten transport reliability, tourism activity, or public safety.

South & Central America Avalanche Radar Market

South & Central America Avalanche Radar Market is supported by avalanche exposure in mountainous corridors, mining regions, hydropower sites, ski areas, cross-border routes, and remote infrastructure zones across the Andes and other snow-prone terrain. Market dynamics are influenced by the need to protect workers, travelers, energy assets, mining operations, and tourism infrastructure from sudden snow-slide events. The region offers opportunities for radar suppliers, geohazard specialists, remote monitoring firms, and system integrators that can provide durable, low-maintenance solutions for high-altitude environments. Latest trends include adoption of automated avalanche detection for road safety, integration with weather and slope-monitoring systems, and demand for remote alert platforms in mining and infrastructure projects. The forecast outlook remains positive in targeted high-risk locations as companies and authorities prioritize risk reduction, operational continuity, and worker safety.

Key Insights

- The avalanche radar market is gaining importance as mountain safety agencies, transport authorities, ski resorts, and infrastructure operators increasingly require real-time detection systems capable of monitoring avalanche activity during snowstorms, darkness, fog, and low-visibility conditions.

- With mountain roads, tunnels, railways, and border corridors exposed to sudden snow-slide risks, avalanche radar systems are becoming essential for automated warning, route closure decisions, controlled avalanche operations, and safer movement of vehicles and passengers through high-risk terrain.

- Ski resorts and winter tourism operators are adopting avalanche radar to improve slope monitoring, guide ski patrol decisions, manage backcountry access, and strengthen guest safety across exposed mountain areas where manual observation alone is not sufficient.

- Changing snowfall patterns, freeze-thaw cycles, rain-on-snow events, and unstable snowpack behavior are increasing the need for continuous avalanche monitoring, making radar-based detection a valuable tool for climate-resilient mountain risk management.

- The integration of avalanche radar with weather stations, snow-depth sensors, seismic systems, infrasound detectors, cameras, and geospatial platforms is becoming a major trend, enabling operators to build more accurate and responsive avalanche warning networks.

- AI-enabled analytics and automated event classification are improving the performance of avalanche radar systems by helping distinguish actual avalanche movement from weather noise, wildlife, falling rocks, and other environmental disturbances.

- Remote installation environments remain a key market challenge, as avalanche radar systems must operate reliably in high-altitude locations exposed to extreme cold, heavy snowfall, strong winds, limited power supply, and difficult maintenance access.

- Government disaster management agencies and public safety authorities are increasingly investing in avalanche radar systems to reduce casualties, protect infrastructure, support emergency response, and improve documentation of avalanche-prone zones.

- Hydropower facilities, mountain pipelines, transmission lines, mining sites, and remote industrial assets are creating niche opportunities for avalanche radar providers as companies seek to protect workers, equipment, access roads, and critical infrastructure.

- The competitive landscape is shifting toward integrated geohazard monitoring solutions, with customers preferring vendors that can provide radar hardware, software dashboards, installation, calibration, communication systems, maintenance, and expert risk-management support.

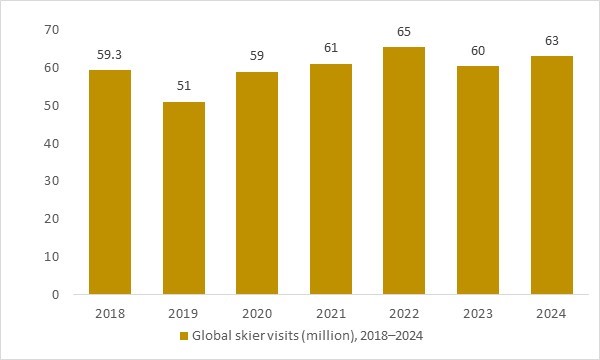

skier visits (million), 2018–2024

Figure: Global skier visits have risen steadily between 2018 and 2024, reflecting expanding participation in winter sports and growing human exposure to avalanche-prone mountain environments. As ski resorts, backcountry areas and mountain transport corridors handle increasing traffic each season, operators face heightened safety, monitoring and risk-management requirements—driving accelerated adoption of radar-based avalanche detection and early-warning systems worldwide. OG Analysis estimates, derived from international winter tourism indicators and mountain safety infrastructure studies, illustrate how rising global skier activity strengthens long-term demand for automated avalanche monitoring networks, supports investment in real-time sensing technologies, and enhances overall preparedness across high-altitude regions.

The Avalanche Radar Market is increasingly shaped by the steady rise in global skier visits between 2018 and 2024e, which expands human activity across avalanche-prone mountain regions. Growing winter tourism, heavier slope utilization and intensified backcountry access elevate the need for real-time monitoring and automated early-warning systems. As resorts and mountain authorities prioritize safety, radar-based avalanche detection technologies gain prominence for their accuracy, range and rapid response capability. This sustained global increase in skier traffic strengthens long-term investment momentum in advanced sensing infrastructure and integrated mountain-safety solutions.

Report Scope

| Parameter | Avalanche Radar Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Application, By End User, By Technology, and By Distribution Channel |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Avalanche Radar Market Segmentation

By Type

- Long Range

- Short Range

By Component

- Transmitter

- Antennas

- Receiver

- Display

By End-User

- Military And Defense

- Government

- Weather Monitoring

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Analysed

Geobrugg AG, Wyssen Avalanche Control AG, L.B. Foster Company, Hexagon AB, Recco AB, Trimble Inc., Swiss Radar Technologies AG, Vaisala Oyj, Defense Research and Development Organization, Leica Geosystems, ARVA Equipment, IDS GeoRadar, Laser Components Detector Group Inc, GEOPRAEVENT AG, Swiss Avalanche Warning Service, Technoalpin S.p.A., Defense Advanced Research Projects Agency (DARPA), Raytheon Company, Northrop Grumman Corporation, Lockheed Martin Corporation, Thales Group, Saab AB, Leonardo S.p.A., Rheinmetall AG, Israel Aerospace Industries Ltd., Harris Corporation, FLIR Systems Inc., Elbit Systems Ltd., BAE Systems plc, General Dynamics Corporation

Recent Industry Developments

April 2026 - Wyssen Avalanche Control reported that its Avalanche Detection Network in British Columbia provided real-time avalanche data during the season’s largest natural avalanche cycle, supporting forecasting and operational decisions in Glacier National Park.

April 2026 - Wyssen Canada announced a leadership transition, appointing Lisa Dreier as CEO while Walter Steinkogler moved to a group-level role to strengthen Wyssen Avalanche Control’s international operations.

February 2026 - Wyssen Avalanche Control installed an avalanche detection system in Livigno for the Milano Cortina Winter Olympics, combining seismic and infrasound sensors, cameras, and WAC.3 Cockpit to support road safety and automated warning measures.

January 2026 - Wyssen Avalanche Control highlighted its site-specific avalanche warning work for Tromsø municipality, where its forecasting service supported evacuation planning and local safety decisions during a complex avalanche cycle.

December 2025 - Wyssen Avalanche Control began construction of its new Hall D facility in Switzerland to expand assembly, storage, and production capacity for avalanche detection, control, and monitoring technologies.

September 2025 - GEOPRAEVENT announced a monitoring system for the Karrat Fjord rock-avalanche area in West Greenland, expanding its natural hazard monitoring solutions for unstable Arctic slopes and related tsunami risks.

June 2025 - GEOPRAEVENT announced a monitoring system in Brienz/Brinzauls, Switzerland, designed to track slope instability risks affecting alpine settlements and critical infrastructure.

May 2025 - GEOPRAEVENT developed a sophisticated monitoring system at the Simplon Pass in Switzerland, supporting hazard detection and warning capabilities for one of the country’s key alpine transport routes.

May 2025 - Wyssen Norge and Sweco supported emergency reconstruction work on damaged power lines in Skjomen, Norway, by providing daily avalanche warnings and on-site avalanche expertise until repairs were completed.

January 2025 - Fraunhofer announced a passive radar-based avalanche detection approach using existing communication signals, highlighting a potential low-infrastructure monitoring method for avalanche-prone mountain regions.

FAQ's

The Global Avalanche Radar Market is estimated to generate USD 8.4 billion in revenue in 2026.

The Global Avalanche Radar Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 39.44% during the forecast period from 2026 to 2034.

The Avalanche Radar Market is estimated to reach USD 119.9 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!