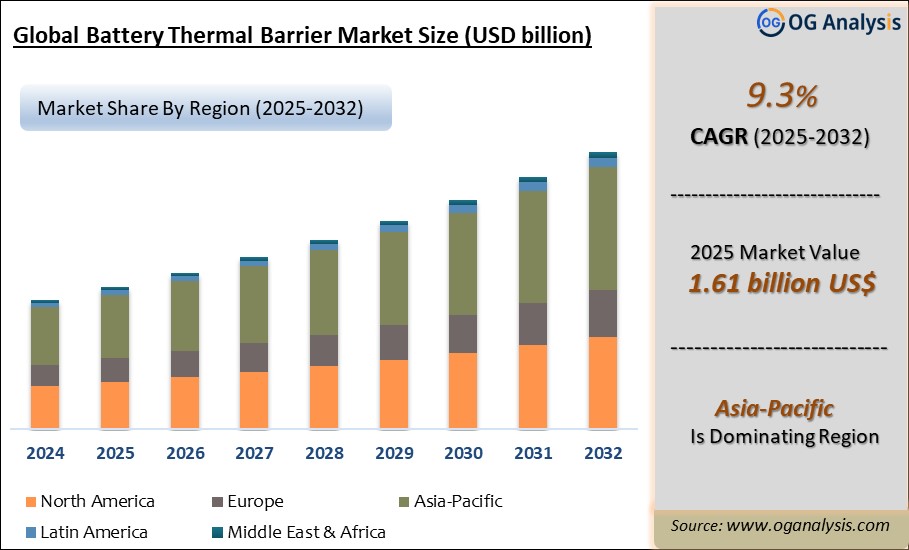

"The Global Battery Thermal Barrier Market Size is valued at USD 1.61 Billion in 2025. Worldwide sales of Battery Thermal Barrier Market are expected to grow at a significant CAGR of 9.3%, reaching USD 3.01 Billion by the end of the forecast period in 2032."

The battery thermal barrier market plays a crucial role in enhancing the safety and efficiency of energy storage systems, particularly in electric vehicles (EVs) and renewable energy applications. Battery thermal barriers are specially designed materials or structures that mitigate the risks of thermal runaway, a phenomenon where a cell’s temperature rapidly increases and can trigger a chain reaction in neighboring cells. By containing heat and preventing it from spreading, these barriers ensure greater stability, prolong battery life, and improve overall performance. With the accelerating adoption of EVs and the increasing reliance on energy storage solutions for renewable sources, manufacturers have focused on developing advanced thermal barriers that combine lightweight, durable, and cost-effective properties. As a result, the market has witnessed significant innovation, creating opportunities for both established players and emerging startups.

The market is driven by the need to meet stringent safety standards, address consumer concerns over battery reliability, and support advancements in battery chemistries. Battery thermal barriers are now more than just safety components; they are integral to enabling high-energy-density batteries that can sustain long ranges and fast-charging capabilities. From traditional materials like ceramic composites to next-generation aerogels and phase-change materials, the spectrum of available solutions is expanding rapidly. This innovation is complemented by growing collaboration among automotive OEMs, battery manufacturers, and material science companies. With the increasing push toward sustainable transportation and renewable energy, battery thermal barriers are set to remain a critical component of the evolving energy storage ecosystem.

Asia Pacific is the leading region in the battery thermal barrier market, propelled by the rapid expansion of electric vehicle production, strong government incentives for battery safety, and the growing presence of lithium-ion battery manufacturers. The passenger EV segment is the dominating segment in the market, fueled by rising consumer demand, advancements in battery technology, and stringent thermal management safety standards.

Trade Intelligence battery thermal barrier market

| Global Articles of stone or mineral substances n.e.s. Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 2,416 | 2,999 | 2,074 | 1,652 | 1,629 |

| United States of America | 187.5 | 242.7 | 311.1 | 254.8 | 239.7 |

| Japan | 192.7 | 224.6 | 214.8 | 159.0 | 136.2 |

| United Arab Emirates | 13.2 | 13.8 | 11.2 | 10.3 | 92.8 |

| China | 682.8 | 865.9 | 40.1 | 36.7 | 75.0 |

| Germany | 82.9 | 106.6 | 91.7 | 82.5 | 69.7 |

| Source: OGAnalysis | |||||

- United States of America , Japan , United Arab Emirates , China and Germany are the top five countries importing 37.6% of global Articles of stone or mineral substances n.e.s. in 2024

- Global Articles of stone or mineral substances n.e.s. Imports decreased by 32.6% between 2020 and 2024

- United States of America accounts for 14.7% of global Articles of stone or mineral substances n.e.s. trade in 2024

- Japan accounts for 8.4% of global Articles of stone or mineral substances n.e.s. trade in 2024

- United Arab Emirates accounts for 5.7% of global Articles of stone or mineral substances n.e.s. trade in 2024

| Global Articles of stone or mineral substances n.e.s. Export Prices, USD/Ton, 2020-24 |

| |

| Source: OGAnalysis |

Battery Thermal Barrier Market Key Takeaways

- Battery thermal barriers prevent thermal runaway and enhance battery safety and longevity.

- Advanced materials like aerogels and phase-change solutions offer higher efficiency and reduced weight.

- Growing EV adoption drives demand for thermal barriers that support long-range and fast-charging batteries.

- Collaboration among automakers, battery producers, and material companies accelerates innovation in thermal barrier technologies.

- Regulatory pressure to improve battery safety standards encourages the use of advanced thermal management solutions.

- Increased renewable energy storage applications create new opportunities for battery thermal barriers.

- Battery manufacturers are prioritizing thermal management systems to improve performance and consumer confidence.

- Next-generation batteries with higher energy densities require more efficient and durable thermal barriers.

- Regional markets with aggressive EV adoption targets, such as China and the European Union, are at the forefront of thermal barrier technology integration.

- Sustainability trends are pushing for the development of recyclable and eco-friendly thermal barrier materials.

- R&D investments focus on creating cost-effective, lightweight, and scalable solutions for large-scale battery production.

- Thermal barriers enhance overall vehicle safety, making them a critical factor in EV development strategies.

- Customizable barrier solutions allow manufacturers to address different cell chemistries and module designs.

- Emerging startups are challenging traditional players with innovative approaches to thermal barrier materials.

- Future advancements may integrate intelligent thermal management systems, combining sensors with barrier materials.

Market Scope

| Parameter | battery thermal barrier market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User, By Technology and By Distribution Channel |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Battery Thermal Barrier Market Segmentation

By Product

- Foam

- Coatings

- Fabrics

By Application

- Electric Vehicles

- Consumer Electronics

- Renewable Energy Storage

By End User

- Automotive

- Aerospace

- Electronics

By Technology

- Passive

- Active

By Distribution Channel

- Online

- Offline

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Top 15 Companies Operating in the Battery Thermal Barrier Market

- 3M Company

- Asahi Kasei Corporation

- BASF SE

- Covestro AG

- DuPont

- Evonik Industries AG

- Henkel AG & Co. KGaA

- Kaneka Corporation

- LG Chem

- Saint-Gobain Performance Plastics

- Solvay S.A.

- Sika AG

- Sumitomo Chemical Company, Limited

- Thermo Fisher Scientific Inc.

- Toray Industries, Inc.

Recent Developments

June 2025 — Alkegen began full-scale commercial production of its fiber-enhanced aerogel insulation (AlkeGel) for EV battery fire protection, including thermal barriers, wraps, and cell-spacer components, offering a low-dust version that simplifies integration.

June 2025 — Huntsman launched a new intumescent polyurethane coating system (POLYRESYST EV5005) for EV battery enclosures, suitable for both metal and composite substrates; designed to improve passive fire protection without imposing strict thickness or design constraints.

FAQ's

The Battery Thermal Barrier Market is estimated to reach USD 3.01 Billion by 2032.

The Global Battery Thermal Barrier Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.3% during the forecast period from 2025 to 2032.

The Global Battery Thermal Barrier Market is estimated to generate USD 1.61 Billion in revenue in 2025.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!