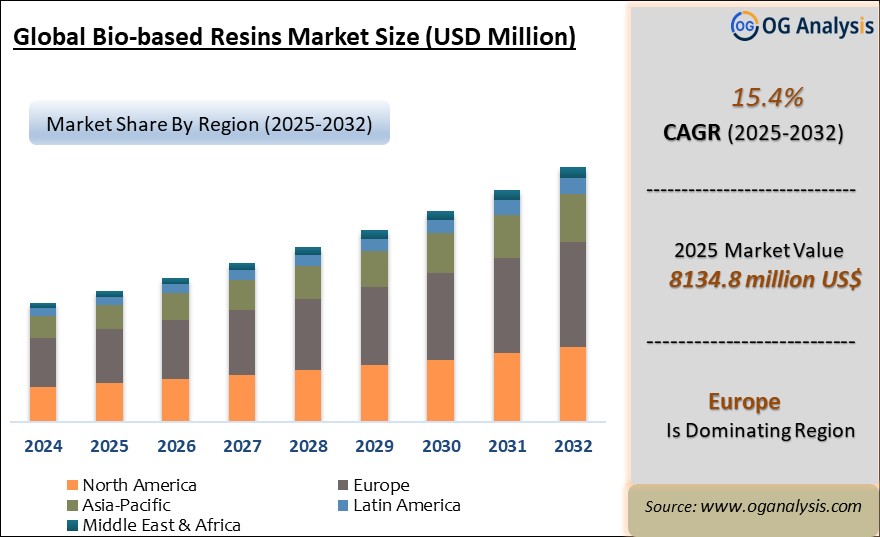

The Bio-based Resins Market is estimated to be USD 7,049.3 million in 2024. Furthermore, the market is expected to grow to USD 19,212.6 million by 2031, with a Compound Annual Growth Rate (CAGR) of 15.4%.

Bio-based Resins Market Overview

The global bio-based resin market is expected to witness substantial growth during the outlook period owing to growing concerns for the environment, sustainability, and the green planet.

Resins can be considered as necessary raw materials constituting various materials in designated proportions used to manufacture a final product with desired attributes. The selection of the correct plastic resin is the most important factor in deciding the success of the end product determining properties to best hold the individual product.

Bio-based resins are the resins that derive some or all of their constituent monomers from biological sources. Major sources for bio-based resins are corn or soybean by-products from bio-diesel fuel refinement, sugar cane, sugar beets, potatoes, lignocellulose, whey, and algae. Bio-based resins are biomaterials that can be biodegradable or non-biodegradable.

Trade Intelligence for bio-based resin market

|

Global Epoxide resins, in primary forms Trade, Imports, USD million, 2020-24 |

|||||

|

|

2020 |

2021 |

2022 |

2023 |

2024 |

|

World |

5,875 |

8,753 |

8,707 |

6,682 |

6,456 |

|

China |

1,255 |

1,460 |

1,123 |

682 |

654 |

|

United States of America |

352 |

694 |

983 |

594 |

583 |

|

Germany |

495 |

701 |

691 |

559 |

492 |

|

Korea, Republic of |

145 |

202 |

200 |

183 |

288 |

|

Mexico |

166 |

218 |

268 |

259 |

275 |

|

Source: OGAnalysis, International Trade Centre (ITC) |

|||||

- China, United States of America, Germany, Korea, Republic of and Mexico are the top five countries importing 35.5% of global Epoxide resins, in primary forms in 2024

- Global Epoxide resins, in primary forms Imports increased by 9.9% between 2020 and 2024

- China accounts for 10.1% of global Epoxide resins, in primary forms trade in 2024

- United States of America accounts for 9% of global Epoxide resins, in primary forms trade in 2024

- Germany accounts for 7.6% of global Epoxide resins, in primary forms trade in 2024

|

Global Epoxide resins, in primary forms Export Prices, USD/Ton, 2020-24 |

|

|

|

Source: OGAnalysis |

Latest Trends in Bio-based Resins Market

Widening End-Use Applications:

A major portion of Bioplastics and Biopolymers are being consumed in manufacturing shopping bags, fruit, and vegetable bags, cutlery, cosmetic packaging, and a few consumer goods. Characteristic limitations of bio-friendly plastic are limiting the use of the product that currently constitutes less than 2% of the total plastic consumption.

However, the pressing need for sustainable products from the government and the public is stimulating companies to invest in extensive research and development activities to widen the applications of bioplastics. The bio-based arena envisions enormous scope to develop new products, access new markets, and develop new applications. Bio-based Resins play a crucial role in improving performance and achieving ambitious targets.

Europe is the leading region in the Bio-based Resins Market, fueled by stringent environmental regulations, strong sustainability initiatives, and increasing demand for eco-friendly materials across packaging and automotive industries.

Packaging is the dominating segment in the Bio-based Resins Market, powered by growing consumer preference for biodegradable alternatives, rising bans on single-use plastics, and supportive government policies promoting circular economy practices.

Driving Factors

Functional Advantages of Bio-Plastics:

Biodegradability is becoming an increasingly popular and lucrative product feature, as in the case of plants and flowers pots that can be placed straight into the soil to biodegrade naturally.

The growing use of bioplastic helps to reduce the amount of waste produced, which in turn has a positive effect on the environment and helps meet different sustainability goals as increasing the percentage of recycled material, reducing waste, minimizing energy consumption, etc. According to the analysis of patent filing data, companies’ priority remains on improving the mechanical properties of bioplastics for mass production.

Market Challenges

Feedstock Availability:

Biobased bioplastics can be made using a wide range of different feedstocks such as starch, sugar, or cellulose. These are the first-generation feedstock and efforts are made to switch to the second generation. The second generation of feedstock can be sugars from bagasse, straw, etc.

Due to the effect of COVID, the input costs across materials and the restricted labor movement are leading to supply disruptions in the value chain and the trade chain.

Prices of raw material biomaterials required for the Bio-based resin market depend on various factors including farmers’ planting decisions, climate, domestic and foreign government policies, imbalances in world grain supplies, and many others. These unpredictable situations deciding the production of crops create a gloomy outlook for the manufacturers.

Report Scope

|

Parameter |

bio-based resin Market scope Detail |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Market Size-Units |

USD million |

|

Market Splits Covered |

By Product type, By Application and By End-User |

|

Countries Covered |

North America (USA, Canada, Mexico) |

|

Analysis Covered |

Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

|

Customization |

10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

|

Post-Sale Support |

4 analyst hours, available up to 4 weeks |

|

Delivery Format |

The Latest Updated PDF and Excel Data file |

Market Segmentation

By Product

- Polylactic Acid (PLA)

- Starch Blends

- bio-based PE

- bio-based PTT

- bio-based PA

- Others

By Type

- Biodegradable

- Non-biodegradable

By Application

- Flexible Packaging

- Rigid Packaging

- Textile

- Agriculture

- Consumer Goods

- Others

By Region

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, South Korea, Indonesia, Malaysia, Vietnam, Rest of APAC)

- The Middle East and Africa (Saudi Arabia, South Africa, UAE, Iran, Egypt, Rest of MEA)

- South and Central America (Brazil, Argentina, Chile, Rest of SCA)

Companies Mentioned

- Akro Plastic Gmbh

- CLARIANT AG (Avient)

- BASF SE

- Koninklijke DSM N.V.

- Archer Daniels midland

- LyondellBasell Industries NV

- DuPont de Nemours, Inc.

- Royal DSM N.V.

- Evonik Industries AG

- Lanxess AG

- Solvay SA

- Mitsubishi Chemical Corporation

- Braskem S.A.

- BioAmber Inc.

- Myriant Corporation

- Tianyi Licocene Technology (Jiangsu) Co., Ltd.

- Chengdu Institute of Bio-industry Technology Co., Ltd.

- Reverdia

Recent Developments

- October 2025: Braskem expanded its I’m green™ bio-based plastics portfolio, showcasing new client partnerships and product lifecycle improvements to advance sustainable packaging and consumer goods.

- September 2025: Michelin’s BioImpulse project achieved commercial scale for a new bio-based monomer used in high-performance adhesive resins, replacing substances of very high concern in industrial formulations.

- September 2025: Cristex Composite Materials introduced a new line of bio-based epoxy resin systems targeting lightweight and sustainable composites for automotive and construction applications.

- August 2025: Solinatra commenced full-scale production of 100% compostable and plastic-free bio-resins designed for seamless integration into existing manufacturing lines across consumer and packaging industries.

- April 2025: Teijin announced Sigma Corporation’s adoption of its biomass-derived polycarbonate resin for precision optical components, marking a transition toward low-carbon, sustainable materials in electronics.

- April 2025: Huntsman unveiled its new I-BOND® bio-based resin range with significant renewable carbon content, enabling reduced emissions and formaldehyde-free performance for wood composite manufacturing.

- April 2025: Verde Bioresins expanded its PolyEarthylene® bio-resin product line to include biodegradable film grades suitable for extrusion coating, stretch wraps, and food-contact packaging.

- March 2025: Arkema advanced development of its N3xtDimension® bio-based UV-curable resins optimized for 3D printing, supporting performance parts and medical device applications with lower environmental impact.

- February 2025: Covestro announced pilot-scale trials of next-generation bio-based polyurethane dispersions aimed at coatings and adhesives, targeting higher durability and lower carbon intensity.

- January 2025: BASF initiated collaborative R&D on new bio-acrylic resin platforms derived from renewable feedstocks to replace fossil-based chemistries in industrial coatings and composites.

FAQ's

The Bio-based Resins Market is estimated to reach USD 22171.4 million by 2032.

The Global Bio-based Resins Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 15.4% during the forecast period from 2025 to 2032.

The Global Bio-based Resins Market is estimated to generate USD 7049.3 million in revenue in 2024.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!