"The Global Bioplastic Market was valued at $11.61 billion in 2026 and is projected to reach $ 45.8 billion by 2034, growing at a CAGR of 16.47%."

The bioplastic market has moved from a specialty sustainability segment into a strategically important materials category within the broader plastics industry, driven by the need to reduce fossil-feedstock dependence, expand circularity options, and offer lower-impact material choices across consumer and industrial applications. Bioplastics today span both bio-based and biodegradable material families, including PLA, PHA, starch blends, compostable compounds, and selected bio-based drop-in polymers that can serve packaging, food serviceware, shopping and organic-waste bags, agricultural films, fibers, hygiene products, consumer goods, and increasingly selected durable and technical applications. Packaging remains the leading end-use anchor, but the market is broadening as material innovation improves performance, processing flexibility, and end-of-life positioning across films, coatings, molded parts, and specialty applications. Current market trends are defined by stronger material diversification, faster development of PLA and PHA platforms, wider interest in compostable solutions for food-contaminated packaging streams, and growing use of bioplastics in fibers, 3D printing, paper coating, and other application-specific formats. Demand is being reinforced by corporate packaging commitments, tightening scrutiny of conventional plastics, demand for compostable and bio-based alternatives in selected use cases, and the wider push for materials that can align functionality with circular economy goals. As a result, the market is no longer being shaped only by the idea of renewable content; it is increasingly driven by application fit, end-of-life logic, processing efficiency, and the ability of bioplastics to solve specific performance and sustainability challenges in real commercial settings.

From a competitive standpoint, the market is defined by a mix of established biopolymer producers, compostable-material specialists, global chemical companies, and emerging PHA innovators competing on feedstock strategy, processing performance, certifications, application development, and scale-up capability. Competition is no longer based only on offering a bio-based resin; it increasingly depends on whether suppliers can deliver material solutions that run on existing converting lines, meet compostability or recyclability expectations where relevant, and support customer goals in packaging, food service, agriculture, and specialty durable uses. The competitive landscape is being shaped by ongoing capacity expansion, regional manufacturing investment, new grades for biaxially oriented films, extrusion coatings, paper coatings, and 3D printing, as well as broader efforts to position bioplastics within more credible end-of-life systems. Recent developments underline this shift clearly: NatureWorks has continued advancing new PLA grades and its integrated Thailand manufacturing platform, BASF continues positioning ecovio in compostable applications, while CJ Biomaterials and other innovators are widening the role of PHA in coatings, packaging, and new specialty formats. Looking ahead, the market outlook remains favorable because bioplastics are increasingly being evaluated not as universal replacements for all plastics, but as targeted materials for applications where renewable content, compostability, lower carbon positioning, or circular-system compatibility can create clear commercial value. Companies that can combine scale, technical support, application-specific performance, and end-of-life credibility are likely to strengthen their position as the market matures.

Key Market Insights

-

Packaging remains the most influential end-use segment in the bioplastic market, continuing to anchor demand across rigid packaging, films, food serviceware, coated paper, and compostable formats. This keeps application development strongly tied to brand sustainability targets and packaging circularity strategies.

-

PLA continues to hold a central commercial role because it combines renewable feedstock positioning with expanding usability in films, paper coatings, fibers, food service products, and 3D printing. Ongoing grade development is widening its relevance beyond conventional single-use applications.

-

PHA is emerging as one of the most important innovation themes in the market, especially for coatings, packaging, and applications that need biodegradability with stronger performance tuning. This is making PHA a growing strategic complement to PLA rather than just a niche alternative.

-

Compostable applications continue to gain traction where food contamination or organic-waste collection makes conventional recycling less practical. This keeps compostable bags, food serviceware, coffee pods, and selected coated-paper uses highly relevant to market development.

-

End-of-life positioning is becoming a decisive competitive factor, with suppliers increasingly expected to explain whether a product is recyclable, industrially compostable, or suited to another circular pathway. Market success is therefore increasingly tied to system compatibility, not just bio-based content.

-

Manufacturing scale-up remains a major structural theme, as new plants, financing support, and regional distribution partnerships are shaping how quickly bioplastics can move from premium niches into broader commercial supply. Scale and supply reliability are becoming more important competitive differentiators.

-

Application diversification is expanding the market beyond packaging into fibers, agriculture, consumer goods, durable items, and additive manufacturing. This reduces dependence on a single outlet and supports more resilient long-term market development.

-

Competition is increasingly shifting toward solution-based value, where suppliers win through formulation support, processing ease, certification readiness, and fit-for-purpose performance. Companies that solve specific customer challenges are likely to lead the next phase of bioplastics adoption.

Regional Insights

North America Bioplastic Market

North America remains an innovation-led bioplastic market, with demand shaped by sustainable packaging, foodservice applications, specialty films, coffee capsules, and a growing interest in compostable and high-performance bio-based materials. Market dynamics are being influenced by brand pressure to replace selected fossil-based plastics, the gradual buildout of composting-linked use cases, and stronger attention to application-specific materials such as PLA and PHA rather than broad one-size-fits-all substitution. Lucrative opportunities for companies are strongest in compostable food-contact packaging, certified serviceware, barrier applications, and specialty compounds that can run on existing converting lines. The latest trends point to more focused commercialization around performance-proven formats, while the forecast remains favorable as recent developments such as the launch of Ingeo-based compostable coffee pods for the North American market and Teknor Apex’s acquisition of Danimer Scientific reinforce the region’s shift toward more consolidated, application-driven bioplastics growth.

Asia Pacific Bioplastic Market

Asia Pacific remains the strongest regional growth engine for the bioplastic market, supported by large-scale packaging demand, expanding manufacturing ecosystems, and increasing regional investment in bio-based polymer capacity. Market dynamics are shaped by the region’s role as both a major converter base and an increasingly important production hub for PLA, bio-based polyethylene, and emerging specialty biopolymers. Lucrative opportunities for companies are strongest in flexible packaging, food-contact applications, fibers, coated paper, and new downstream uses that benefit from scalable local supply. The latest trends indicate stronger vertical integration and feedstock partnerships, while the forecast remains highly positive as regional manufacturing platforms continue to expand; recent developments such as financing progress for NatureWorks’ integrated PLA facility in Thailand and Braskem Siam’s ethanol-supply agreement for a planned bio-ethylene project in Thailand underline Asia Pacific’s growing importance in bioplastics scale-up.

Europe Bioplastic Market

Europe is the most regulation-driven and policy-sensitive bioplastic market, where demand is increasingly shaped by packaging compliance, compostable application logic, and the broader circular economy agenda. Market dynamics are influenced by stricter packaging rules, closer scrutiny of end-of-life claims, and continued interest in bioplastics for applications where compostability or renewable content can provide a clear system benefit. Lucrative opportunities for companies are strongest in food packaging, paper coatings, organic-waste collection formats, specialty films, and premium consumer applications that require both performance and regulatory alignment. The latest trends point toward more selective, fit-for-purpose adoption rather than undifferentiated substitution, and the outlook remains constructive as Europe tightens packaging rules and rewards materials with clearer circular-use cases; recent developments such as the entry into force of the Packaging and Packaging Waste Regulation and BASF’s continued push for ecovio in modern packaging applications reinforce this direction.

Middle East & Africa Bioplastic Market

The Middle East & Africa bioplastic market is still emerging, but it is becoming increasingly relevant as regional players move from downstream packaging demand toward local material production and more structured sustainability initiatives. Market dynamics are being shaped by growing interest in sustainable packaging, import substitution opportunities, and early investments in regional biopolymer capacity, especially in Gulf markets. Lucrative opportunities for companies are strongest in PLA-based packaging, foodservice items, retail packaging, and future partnerships that combine regional converting capacity with locally available or imported bio-based feedstocks. The latest trend is a transition from market exploration to industrial execution, and the forecast remains positive as the region builds a stronger manufacturing base; recent developments such as Emirates Biotech’s launch of its Embio PLA product range and its selection of a contractor for a PLA plant in the UAE point to a more credible long-term regional growth story for bioplastics.

South & Central America Bioplastic Market

South & Central America remains a strategically important region for the bioplastic market because of its strong bio-based feedstock position, especially sugarcane-linked chemistry, and its established role in renewable-polymer innovation. Market dynamics are shaped by feedstock availability, regional packaging demand, and growing efforts to connect bio-based and circular plastics more closely with mainstream commercial applications. Lucrative opportunities for companies are strongest in bio-based polyethylene, flexible packaging, personal care and household packaging, and regional partnerships that can translate agricultural strength into higher-value polymer output. The latest trends point to deeper commercialization of plant-based plastics and broader sustainability positioning across the packaging value chain, and the forecast remains favorable as South America continues to leverage renewable feedstocks and circular-material innovation; recent developments such as Braskem’s first sale of circular PE in South America and its unveiling of new bio-based packaging innovations at K 2025 highlight the region’s continued leadership in commercially visible bioplastic platforms.

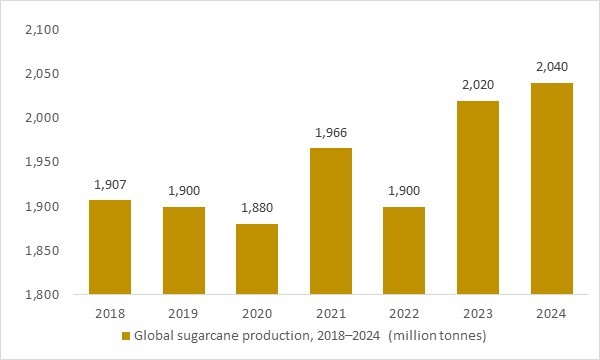

Global sugarcane production, 2018–2024 (million tonnes)

Figure: Global sugarcane production increased from providing a massive and expanding carbohydrate feedstock base for bioplastics. OG Analysis estimates, derived from FAO data, show how this abundant sugarcane supply underpins bio-PE, bio-PET, PLA and other bio-based polymers used in packaging, consumer goods and industrial components. The same bio-based materials increasingly feature in sustainable housings, enclosures and logistics packaging for radiation-detection, monitoring and security applications, aligning decarbonization goals with safety and compliance.

Global sugarcane production has risen from about 1,900 million tonnes in 2018 to an estimated 2,040 million tonnes by 2024, providing a massive and expanding carbohydrate feedstock base. This abundant supply underpins the growth of bioplastics made via sugar/ethanol routes to bio-PE, bio-PET, PLA and other bio-based polymers used in packaging, consumer goods and industrial components. As brands and regulators push for lower-carbon materials, sugarcane-derived bioplastics increasingly replace fossil plastics in housings, enclosures and logistics packaging. In radiation-detection, monitoring and security applications, this same bio-based material base supports more sustainable instrument casings, cable jackets and transport packs for radiopharmaceuticals, aligning safety infrastructure with decarbonization goals.

Report Scope

| Parameter | bioplastic market scope Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type ,By Distribution Channel ,By Application |

|

Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Bioplastic Market Segments Covered In The Report

By Type

- Biodegradable

- Non-Biodegradable

By Distribution Channel

- Online

- Offline

By Application

- Rigid Packaging

- Flexible Packaging

- Textile

- Agriculture And Horticulture

- Consumer Goods

- Automotive

- Electronics

- Building And Construction

- Other Applications

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Covered

Lonza Group AG, Fujifilm Diosynth Biotechnologies USA Inc., Thermo Fisher Scientific Inc., Samsung BioLogics Co. Ltd., WuXi Biologics Co. Ltd., Lonza Ltd., JRS Pharma Group, CMC Biologics AS, Catalent Inc., Boehringer Ingelheim GmbH, Rentschler Biopharma SE, AGC Biologics Inc., Abzena Ltd., AbbVie Inc., AstraZeneca plc, Bayer AG, Biogen Inc., Bristol-Myers Squibb Co., Eli Lilly and Company, Gilead Sciences Inc., GlaxoSmithKline plc, Johnson & Johnson, Merck & Co., Novartis AG, Pfizer Inc., Roche Holding Ag, Sanofi SA, Takeda Pharmaceuticals Co., Teva Pharmaceutical Industries Ltd., Vertex Pharmaceuticals Company, Moderna BioTechnology Company

Recent Industry Developments

- August 2025: Scientists at Washington University unveiled a novel bioplastic—named LEAFF—that biodegrades at room temperature, can be printed on, resists air and water, and offers significantly improved strength over conventional petroplastics.

- June 2025: Braskem inaugurated its $20 million Renewable Innovation Center in Massachusetts to advance research in converting bio-based feedstocks into next-generation bioplastics, aiming to scale biopolymer production toward one million tons annually by 2030.

- June 2025: A leading U.S. packaging manufacturer launched a new product line made entirely from compostable bioplastics for food service packaging, reinforcing its strategy to reduce landfill waste through sustainable packaging alternatives.

- June 2025: Danimer Scientific introduced a next-generation biodegradable resin with enhanced moisture resistance, tailored for food packaging applications, signifying technological progress in bioplastic performance.

- May 2025: An American biopolymer startup revealed an innovative algae-based bioplastic that offers improved biodegradability and moisture resistance, marking progress in eco-friendly material development.

- May 2025: Intec Bioplastics launched EarthPlus® Hercules Bioflex™ Stretch Wrap—a sustainable, high-performance packaging material incorporating 35% renewable plant-based content and notable stretch properties, designed for pallet and food-wrapping use.

FAQ's

The Global Bioplastic Market is estimated to generate $ 11.61 billion in revenue in 2026.

The Global Bioplastic Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 16.47% during the forecast period from 2026 to 2034.

The Bioplastic Market is estimated to reach $ 45.8 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!