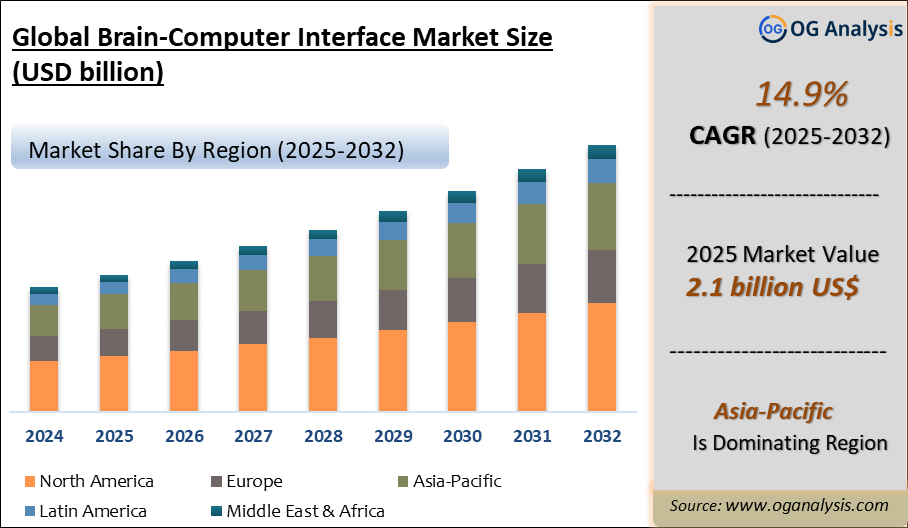

"The Brain Computer Interface Market Size was valued at $ 2.4 billion in 2026. Worldwide sales of Brain Computer Interface are expected to grow at a significant CAGR of 14.9%, reaching $ 7.7 billion by the end of the forecast period in 2034."

The Brain Computer Interface Market is gaining strong attention as healthcare, neurotechnology, assistive devices, gaming, defense, rehabilitation, and human-machine interaction applications move toward more direct communication between the brain and external devices. Brain computer interfaces enable users to control computers, robotic limbs, wheelchairs, communication tools, prosthetics, and digital systems through neural signals. Demand is supported by rising interest in neurological rehabilitation, treatment support for paralysis and motor impairment, non-invasive wearable neurotechnology, and advanced assistive communication systems. These solutions are increasingly being explored for patients with spinal cord injuries, stroke-related disabilities, neurodegenerative conditions, and severe mobility limitations. Developers are focusing on improving signal accuracy, device comfort, processing speed, safety, and ease of use.

Market development is also being shaped by advances in artificial intelligence, machine learning, neural sensors, implantable electrodes, electroencephalography devices, wireless communication, miniaturized electronics, and real-time signal interpretation. Non-invasive systems are gaining wider commercial interest due to lower risk and easier adoption, while invasive systems remain important for high-precision medical and research applications. Companies and research institutions are working to improve neural decoding, reduce training time, enhance user experience, and expand practical applications beyond clinical environments. However, adoption faces challenges related to safety, regulatory approval, data privacy, ethical concerns, high development cost, clinical validation, and long-term reliability. Overall, brain computer interfaces are evolving from experimental neurotechnology toward practical tools for restoring function, enhancing interaction, and supporting next-generation human-machine communication.

Regional Analysis

North America Brain Computer Interface Market

North America remains the leading market for brain computer interfaces, supported by advanced neuroscience research, strong medical-device innovation, venture funding, rehabilitation technology adoption, and active clinical development. The United States leads demand through implantable BCI trials, non-invasive neurotechnology platforms, assistive communication systems, prosthetic control research, and AI-enabled neural decoding. Companies such as Synchron, Neuralink, Precision Neuroscience, Paradromics, Blackrock Neurotech, and academic medical centers are strengthening the region’s commercial and clinical ecosystem. Recent FDA clearance for Precision Neuroscience’s Layer 7-T cortical electrode interface and ongoing Synchron trials for paralysis-related communication highlight strong regional momentum.

Europe Brain Computer Interface Market

Europe is a significant market for brain computer interfaces, driven by neuroscience research, medical rehabilitation, assistive technology development, neuroprosthetics, digital health, and human-machine interaction studies. Germany, the UK, France, Switzerland, the Netherlands, Italy, and Nordic countries are key contributors due to strong university research networks, healthcare systems, and medical technology capabilities. European adoption is strongest in clinical research, stroke rehabilitation, neurofeedback, prosthetic control, cognitive monitoring, and non-invasive EEG-based systems. However, strict medical-device regulation, data protection rules, ethical review, and reimbursement complexity influence commercialization timelines. The region is also highly focused on neuroethics, mental privacy, patient safety, and responsible development of implantable BCI systems.

Asia-Pacific Brain Computer Interface Market

Asia-Pacific is emerging as a high-growth region for brain computer interfaces, supported by large patient populations, expanding digital health investment, electronics manufacturing, AI capability, and government interest in advanced neurotechnology. China, Japan, South Korea, India, Australia, and Singapore are important markets for BCI research, rehabilitation devices, wearable EEG platforms, neurogaming, education technology, and assistive communication systems. China has become especially active, with government-backed efforts to promote BCI innovation and achieve technical breakthroughs in the coming years. The region also benefits from strong hardware manufacturing, robotics, sensors, and consumer electronics ecosystems, which support lower-cost non-invasive BCI development.

Middle East & Africa Brain Computer Interface Market

The Middle East & Africa market is at an early stage, with demand concentrated in medical research, rehabilitation centers, universities, specialty hospitals, defense training, and assistive technology programs. Gulf countries such as the UAE, Saudi Arabia, and Qatar are potential adopters due to investment in advanced healthcare, AI, smart hospitals, and digital transformation. South Africa also offers selective opportunities through neuroscience research, rehabilitation care, and academic partnerships. Adoption remains limited by high device costs, shortage of specialized clinicians, limited reimbursement, lower clinical trial activity, and dependence on imported neurotechnology. Long-term opportunities are likely to improve as healthcare modernization and AI-enabled medical technology investment expand.

South & Central America Brain Computer Interface Market

South & Central America is an emerging market for brain computer interfaces, led by Brazil, Mexico, Chile, Argentina, and Colombia. Demand is mainly linked to university research, rehabilitation medicine, assistive communication, prosthetic control, neurofeedback, and wearable EEG-based applications. Brazil has the strongest potential due to its larger healthcare and academic research base, while Mexico and Chile are developing opportunities through medical technology and digital health adoption. Commercial growth is expected to remain gradual because of limited funding, regulatory complexity, affordability constraints, and weaker local manufacturing capacity. However, rising interest in neurorehabilitation and low-cost non-invasive BCI systems can support future adoption.

Key Insights

- Brain computer interface demand is supported by rising interest in assistive technologies for people with severe motor limitations. These systems can help users communicate, control devices, and regain functional independence.

- Healthcare and rehabilitation remain major application areas for brain computer interfaces. Technologies are being developed to support stroke recovery, spinal cord injury rehabilitation, prosthetic control, and neurological therapy.

- Non-invasive brain computer interfaces are gaining wider attention due to easier use and lower safety risk. Wearable EEG-based systems are suitable for research, wellness, gaming, training, and early commercial applications.

- Invasive brain computer interfaces offer higher signal precision for advanced medical use cases. These systems are mainly focused on severe paralysis, prosthetic control, and direct neural communication applications.

- Artificial intelligence is improving the performance of brain computer interface platforms. AI helps decode neural signals, reduce errors, personalize responses, and improve real-time device control.

- Prosthetics and robotic control are important growth areas for the market. Brain-controlled limbs and assistive robots can improve mobility, independence, and quality of life for users.

- Gaming and consumer neurotechnology are creating emerging commercial opportunities. Brain-based interaction, focus tracking, immersive control, and adaptive experiences are attracting interest from entertainment and wellness sectors.

- Data privacy and neuroethics are becoming critical market considerations. Brain signal data requires strong protection because it may reveal sensitive information about user intent, cognition, or health.

- Regulatory approval and clinical validation remain key barriers to wider adoption. Developers must prove safety, reliability, long-term performance, and meaningful user benefit before broad commercialization.

- Future growth will depend on comfort, accuracy, affordability, and practical usability. Solutions that combine reliable neural decoding with simple interfaces and strong safety standards are likely to gain stronger acceptance.

Report Scope

| Parameter | Brain Computer Interface Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Application, By End-User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Invasive BCI

- Non-invasive BCI

- Partially invasive BCI

By Application

- Healthcare

- Smart Home Control

- Communication & Control

- Entertainment & Gami

By End User

- Residential

- Commercial

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, South Korea, Rest of APAC)

- The Middle East and Africa (Saudi Arabia, UAE, Iran, South Africa, Rest of MEA)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

1. NeuroSky, Inc.

2. Emotiv Systems

3. Advanced Brain Monitoring, Inc.

4. Natus Medical Incorporated

5. OpenBCI

6. g.tec medical engineering GmbH

7. Brain Products GmbH

8. Neuroelectrics

9. Blackrock Microsystems LLC

10. Compumedics Limited

11. Medtronic PLC

12. Cadwell Industries, Inc.

13. InteraXon Inc.

14. MindMaze

15. Mind Solutions Inc.

Recent Developments

April 2026: China approved the NEO implantable brain-computer interface for market use, making it one of the first commercially approved BCI medical devices for restoring hand function in patients with paralysis. The device was developed by Neuracle Medical Technology with academic support from Tsinghua University and is designed for patients with spinal cord injury.

April 2026: Motif Neurotech received FDA approval for an Investigational Device Exemption to begin the RESONATE Early Feasibility Study for its therapeutic BCI targeting treatment-resistant depression. The device is designed as a small, wirelessly powered implant positioned in the skull above the dura.

January 2026: Neuralink reported that it had 21 participants enrolled globally in its brain implant trials, marking continued expansion of its human BCI testing program. The company’s trials focus on enabling people with severe paralysis to control digital and physical devices through thought.

January 2026: University College London Hospitals reported that seven patients were participating in the GB-PRIME study involving Neuralink’s BCI technology. The study aims to improve independence for people living with paralysis.

November 2025: Paradromics received FDA clearance to begin a U.S. clinical study of its Connexus BCI for speech restoration. The trial is designed to evaluate whether the implant can help people with paralysis communicate through text or synthesized speech.

June 2025: Neuralink raised Series E funding to expand patient access, support clinical trials, and develop new brain-interface devices. The funding strengthened investor confidence in implantable BCI commercialization and scaling.

May 2025: Neuralink received FDA Breakthrough Device Designation for its speech restoration technology. The designation is intended to accelerate development and review of medical devices that may provide significant benefit for patients with severe speech impairment.

May 2025: Synchron announced native BCI integration plans for iPhone, iPad, and Apple Vision Pro, enabling users with severe motor impairment to interact with Apple devices using brain signals. This development supports broader accessibility-focused BCI adoption.

April 2025: Precision Neuroscience announced FDA clearance for its Layer 7 Cortical Interface, a high-resolution cortical electrode array used for recording, monitoring, and stimulation of brain activity. The clearance strengthened the company’s position in minimally invasive neural interface development.

FAQ's

The Global Brain Computer Interface Market is estimated to generate USD 2.4 billion in revenue in 2026.

The Global Brain Computer Interface Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 14.9% during the forecast period from 2026 to 2034.

The Brain Computer Interface Market is estimated to reach USD 5.8 billion by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!