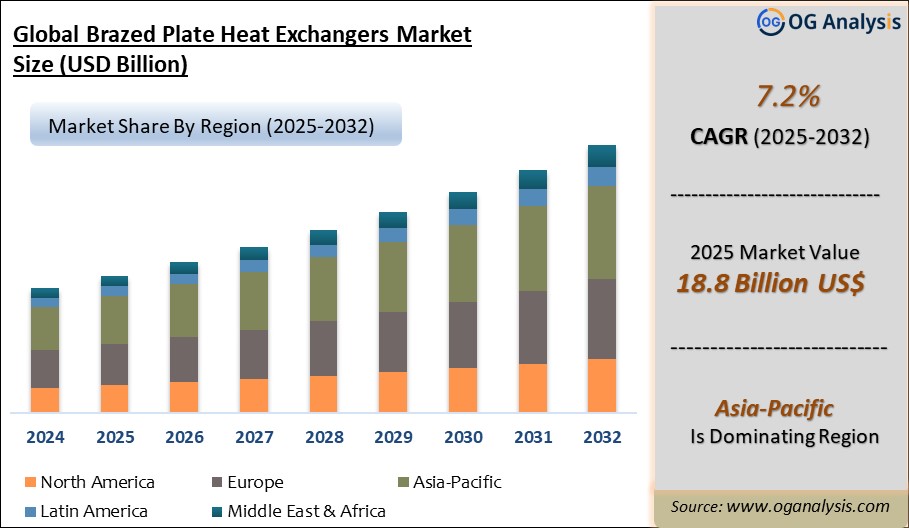

The Brazed Plate Heat Exchangers Market is estimated at USD 15.3 billion in 2022. Further, the market is expected to grow from USD 16.03 billion in 2023 to USD 23.02 billion in 2030 at a CAGR of 7.2%.

Brazed Plate Heat Exchangers Market Market Overview

A Brazed Plate Heat exchanger system is engineered to stop a fire from growing and spreading. With the use of Brazed Plate Heat exchanger systems, fires can be extinguished, kept under control, or avoided. Either heat, smoke, or a combination generally activates the suppression systems. Many Brazed Plate Heat Exchanger systems come with fire detection mechanisms and signaling systems that alert occupants to the problem and direct them to take further suppression action.

The benefits of Brazed Plate Heat Exchanger systems include improved site & personal safety, safe & ease to use, early fire detection, fast & effective, and suitable for most sites. The common Brazed Plate Heat Exchanger types include gas-based, water-based, and wet and dry chemical suppression. Water, foam, CO2, steam, inert gases, and dry chemical powders are fire control agents or media. Inert gases such as nitrogen and aragonite are useful fire suppressants.

Asia-Pacific is the leading region in the brazed plate heat exchangers market, powered by stringent energy efficiency regulations, widespread adoption of renewable heating systems, and strong demand from the HVAC and industrial sectors. The HVAC segment is the top segment in the market, fueled by rising urbanization, increasing commercial infrastructure, and the growing focus on compact and efficient thermal management solutions.

Brazed Plate Heat Exchangers Market Latest Trends ,Driving and Challenges

Technological advancements in Brazed Plate Heat Exchanger systems:

One of the most in-demand Brazed Plate Heat Exchangers systems is the FM200 Brazed Plate Heat Exchangers system, which uses no water to provide fire protection. Globally, modern trends and developments in fire-detection & suppression systems are based on three segments: sensors, signage, and communication. In the field of sensors, the most notable development has been the addition of combined visible smoke and carbon monoxide (CO) sensors to the NFPA code.

In recent years, the most significant trend in signage has been integrating voice evacuation systems with fire detection systems. Another factor that determines the development of fire-detection systems is legislation in the form of standards and certifications. The other advancements include IoT in Fire Safety Systems & connected detectors: The IoT has resulted in much of the world evolving smarter & more connected. With IoT, now safety alerts can be sent to many people quickly & effectively. Many leading organizations are rendering connected smoke detectors for residential use because they can communicate with the Thermostat, which can close the furnace during a fire.

Mass Notification System: Most facility owners & managers are coming to know the benefits of integrating all the building systems, including mass notification and security systems. Wireless Technology: At present, wireless smoke detectors come in more compact and streamlined designs, which can be more appealing. Voice Alert Systems: Systems announcing danger with pre-recorded messages continue to gain traction and, at present, will keep their demand high soon. Machine Learning: The fastest-growing application for ML in the building segment is for improving maintenance. While Machine Learning technologies are implemented for swift maintenance of fire alarm systems, Machine learning applications are highly automated, embedded & self-modifying.

Strict government regulations for the adoption of Brazed Plate Heat Exchangers systems:

Government authorities across the globe have been taking new initiatives and launching directives regarding implementing Brazed Plate Heat Exchangers systems & protection systems at offices and buildings along with buses. Developing countries' governments are expanding the categories of buildings that need a Brazed Plate Heat Exchanger system. With more and more buildings coming under the categories that need mandatory fire protection, there is an increase in demand for modern fire sprinkler systems.

A global coalition of over 80 fire-safety leadership organizations has launched a new Decade of Action for Fire Safety 2022-2032 to ensure an internationally consistent approach to the safety and management of buildings, infrastructure, and more to save lives by reducing risk and preventing devastating fires. Also, in India, the Ministry of Road Transport and Highways began the installation of fire alarms, fire protection systems, and suppression systems in school and passenger buses.

In 2021, in the U.S., nearly 1.3 million fire incidences were reported and caused over 3000 deaths. Due to this, NFPA has enacted guidelines for commercial business infrastructures to implement Brazed Plate Heat exchanger systems such as sprinklers and clean agent suppression systems.

High installation & maintenance costs of Brazed Plate Heat exchanger systems:

A high initial investment is required for the deployment of Brazed Plate Heat exchanger systems. According to NFPA, the average fire sprinkler installation costs around $1.35 per square foot of protected space. In general, larger suppression systems require more points of delivery, sensors, alarms, pull stations, piping, and other complicated control units. For example, a simple water sprinkler system installation in new construction can cost around $1 to $2 per square foot.

An annual inspection of a Brazed Plate Heat Exchangers system with fewer than 30 detectors will cost around $880 to $1,000. Larger suppression systems take longer to inspect and require more skilled technicians, costing around $1,800 to $4,000. The high costs are due to the complexity of networks and the need to develop sophisticated tools to counter a fire situation. Due to this, solution vendors need to upgrade their solutions and develop new technologies constantly.In addition to establishing general codes and safety standards, the NFPA also mandated the installation of fire protection systems in new commercial construction projects. In older buildings, they mandated the replacement of obsolete fire alarms, sprinklers, and detectors. As older properties update fire safety systems to adhere to new policies, remodeling activities are expected.

Companies Mentioned

Johnson Controls

Halma PLC.

Hochiki Corp.

Honeywell International Inc

Siemens AG

Robert Bosch GmbH

Firefly AB

Market Scope

|

Parameter |

Detail |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Market Size-Units |

USD billion |

|

Market Splits Covered |

By Product Type, By Application, By End User |

|

Countries Covered |

North America (USA, Canada, Mexico) |

|

Analysis Covered |

Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

|

Customization |

10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

|

Post-Sale Support |

4 analyst hours, available up to 4 weeks |

|

Delivery Format |

The Latest Updated PDF and Excel Data file |

Market Segmentation

|

Market Split |

Detail |

|

By Product Type |

|

|

By End User |

|

|

By Application |

|

|

By Geography |

|

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!