"The Buses And Coaches Market was valued at $ 44.5 billion in 2026 and is projected to reach $ 66.7 billion by 2034, growing at a CAGR of 5.2%."

The Buses And Coaches Market is a core pillar of public mobility, intercity transport, school transportation, tourism, employee commuting, airport shuttles, and long-distance passenger movement. It spans city buses, intercity buses, school buses, mini and midi buses, and full-size coaches used by public authorities, fleet operators, private mobility companies, and tourism providers. The market is increasingly shaped by the need to combine affordability, safety, passenger comfort, emissions reduction, and digital fleet efficiency in one operating model. Recent market direction shows a clear shift toward battery-electric city buses, the early commercialization of electric intercity buses and coaches, wider use of alternative fuels in selected coach applications, and growing attention to connected services, over-the-air software support, and smarter vehicle uptime management.

Growth is being supported by urban transit modernization, school and shuttle fleet renewal, tourism recovery, stricter safety expectations, and policy pressure to reduce emissions from public transport. At the same time, the competitive landscape is broadening as established global manufacturers compete with scaling players from China, India, Türkiye, and other emerging production bases. A major market trend is the move from simple vehicle procurement toward integrated transport solutions that include charging strategy, depot planning, advanced driver assistance, digital fleet tools, and lifecycle service support. The outlook remains favorable, with city buses leading electrification and coaches moving more gradually through battery-electric, hybrid, and gas-based transition pathways depending on route profile and operating economics.

Regional Analysis

North America Buses And Coaches Market

The North America Buses And Coaches Market is shaped by public-transit fleet renewal, school bus replacement, commuter coach modernization, and rising demand for low- and zero-emission platforms. Market dynamics favor companies that can combine vehicle supply with charging support, telematics, aftersales service, and Buy America-compliant manufacturing, while the most lucrative opportunities remain in transit buses, school transportation, shuttle buses, and commuter coaches serving large metro corridors. The latest trend is the broadening of electrification from city fleets into adjacent segments such as school and commuter applications, alongside consolidation moves that strengthen portfolio breadth and distribution reach. In our view, the regional forecast remains favorable because operators are still prioritizing cleaner fleets, lifecycle support, and dependable domestic production capacity. Recent developments such as New Flyer’s additional low- and zero-emission bus order for the Washington metro region, the reopening and expansion of Canadian manufacturing capability in Winnipeg, and Blue Bird’s full takeover of Micro Bird highlight a market moving toward larger integrated bus platforms with stronger segment coverage.

Asia Pacific Buses And Coaches Market

The Asia Pacific Buses And Coaches Market remains the global center of gravity for both volume demand and technology transition, supported by large urban transit programs, expanding intercity mobility needs, tourism-led coach demand, and deep manufacturing ecosystems in China, India, Japan, and Southeast Asia. Market dynamics are strongest where public authorities and fleet operators are shifting from conventional procurement toward electric buses, smarter fleet operations, and higher-specification intercity vehicles, creating attractive opportunities for companies in city buses, staff transport, school mobility, and premium coaches. The latest trend is the simultaneous rise of large municipal e-bus deployments in India and continued product innovation in China around next-generation city and intercity electric platforms. The forecast remains highly positive, in our view, because the region combines policy-backed fleet electrification with expanding domestic manufacturing depth and export capability. Recent developments such as JBM’s new e-bus deployments under India’s PM e-Bus Sewa program and Yutong’s positioning of the IC12E as a premium battery-electric intercity bus show that Asia Pacific is advancing across both urban bus and coach-related applications.

Europe Buses And Coaches Market

The Europe Buses And Coaches Market is increasingly defined by zero-emission city bus procurement, tightening emissions expectations, and the early but meaningful electrification of intercity and coach segments. Market dynamics favor manufacturers and operators that can deliver battery-electric city buses, emerging electric intercity buses, advanced safety systems, charging strategies, and digital fleet-management support, while lucrative opportunities are strongest in municipal transit, regional routes, school transport, shuttle operations, and premium long-distance coaches. The latest trend is a clear two-speed transition in which city buses are already scaling electrification quickly while coaches and intercity buses are moving from pilot stage toward commercial rollout. In our view, the regional forecast remains strong because regulatory pressure, procurement momentum, and product readiness are now aligned more closely than before. Recent developments including ACEA’s report that electrically chargeable buses continued gaining share in the EU market, Daimler Buses’ presentation of the fully electric Mercedes-Benz eIntouro for intercity and excursion use, and MAN’s launch of its first electric coach confirm that Europe remains the most advanced market for the shift from diesel-led fleets toward a broader electric bus-and-coach mix.

Middle East & Africa Buses And Coaches Market

The Middle East & Africa Buses And Coaches Market is developing through a combination of public-transport modernization in the Gulf, staff and school transport demand, tourism and shuttle activity, and a growing manufacturing role in selected African markets. Market dynamics increasingly favor companies that can provide durable buses for hot-climate operations, flexible fleet formats for urban and intercity services, and localized support for maintenance and assembly, with the strongest opportunities in city buses, airport and staff shuttles, school fleets, and selected coach applications. The latest trend is the move from isolated demonstrations toward larger structured procurements and regional production partnerships, especially around electric buses. In our view, the regional forecast is constructive, led by the Gulf on deployment and by Egypt and selected African hubs on manufacturing and assembly relevance. Recent developments such as Dubai RTA’s receipt of the first batch of new buses including its first large electric-bus procurement, and MCV’s Cairo facility for Volvo electric buses, show a market that is becoming more formalized, more technology-oriented, and more attractive for long-term bus and coach suppliers.

South & Central America Buses And Coaches Market

The South & Central America Buses And Coaches Market is anchored by Brazil and shaped by urban bus renewal, bus rapid transit modernization, growing electrification in major cities, and continuing demand for intercity and charter coaches across regional travel corridors. Market dynamics favor suppliers that can serve high-capacity urban fleets, mid-size city buses, school and staff transport, and long-distance coach operations, while lucrative opportunities are strongest in BRT systems, municipal fleets, export-oriented manufacturing, and fleet replacement programs linked to cleaner mobility goals. The latest trend is the pairing of regional body-building strength with faster electric-bus adoption in leading cities, which is gradually lifting the market from conventional renewal into higher-technology fleet modernization. In our view, the regional forecast remains positive, although momentum will stay concentrated in Brazil, Colombia, Chile, and other markets with stronger institutional procurement and export capacity. Recent developments such as Marcopolo’s push to offset a softer Brazilian market through exports across Latin America, and the rollout in Goiânia of the world’s first regular-service electric bi-articulated bus fleet built with Volvo and Marcopolo, underline the region’s growing importance in both conventional buses and next-generation high-capacity electric systems.

Key Insights

- City bus electrification remains the strongest transformation theme in the market. Public operators are accelerating the move toward battery-electric fleets, while hydrogen remains relevant in selected use cases, making zero-emission deployment a central force in vehicle design, procurement, depot strategy, and supplier competition.

- Coaches and intercity buses are now entering a more serious electrification phase rather than staying limited to urban pilots. Recent product launches show that manufacturers are extending battery-electric platforms into intercity, shuttle, school, and excursion operations, which broadens the market opportunity beyond city transit fleets.

- Safety technology is becoming a more decisive purchasing factor across both buses and coaches. Advanced driver assistance, driver monitoring, braking support, stability systems, and vulnerable-road-user protection are increasingly central to fleet selection, especially for public transport authorities and premium coach operators.

- Digitalization is moving the market beyond the vehicle itself and into connected fleet operations. Over-the-air updates, remote diagnostics, digital fleet portals, and smarter service planning are becoming more important because operators want better uptime, faster maintenance response, and lower operational disruption across large fleets.

- The market is no longer following a single powertrain pathway. Battery-electric buses are advancing quickly, while coaches and regional vehicles are also using gas-based, hybrid, and other transition technologies where route length, refueling needs, and fleet economics still favor a broader technology mix.

- Competitive intensity is increasing as new manufacturing regions scale up and challenge traditional leaders. Industry signals show that suppliers from China, India, Türkiye, and Vietnam are expanding their visibility and capabilities, which is pushing the market toward faster innovation, sharper pricing, and broader global sourcing options.

- Passenger experience and operator economics are becoming more tightly linked in product development. Bus and coach makers are increasingly expected to deliver comfort, accessibility, low noise, energy efficiency, and dependable uptime together, which raises the importance of integrated engineering rather than simple body-and-chassis supply.

- The long-term winners in the Buses And Coaches Market are likely to be companies that combine zero-emission readiness, safety systems, digital support, and strong service networks. As fleets become more complex and technology-rich, competitive advantage is shifting from vehicle sales alone toward full lifecycle transport solutions.

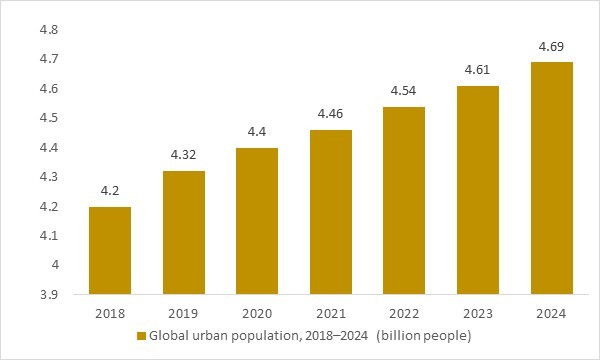

Global urban population, 2018–2024 (billion people)

Figure: Global urban population has increased from around 4.2 billion in 2018 to an estimated 4.7 billion in 2024. This steady rise in urban residents underpins long-term demand for city buses, intercity coaches and school buses as public transport networks expand and modernize. The indicator highlights how urbanization trends structurally support growth opportunities in the global buses and coaches market. OG Analysis, based on international urban population statistics.

- The steady rise in the global urban population—from around 4.2 billion in 2018 to an estimated 4.7 billion in 2024—continues to strengthen long-term demand for buses and coaches. As cities expand, public transport authorities increase investments in fleet renewal, low-emission buses, and high-capacity mobility solutions, making urbanization one of the most consistent structural drivers supporting the global buses and coaches market. OG Analysis.

Market Scope

| Parameter | Buses And Coaches Market |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Buses And Coaches Market Segmentation

By Fuel Type

- Diesel

- Electric And Hybrid

- Other Fuel Types

By Application

- General Transit

- Personal And Recreational

- Tourist

- Other Applications

By Body Built

- Fully Built

- Customizable

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Companies Analysed

Mercedes-Benz Group AG (formerly Daimler AG), Volkswagen AG, CNH, INDUSTRIAL N.V. (IVECO subsidiary of CNH Industrial), YUTONG, Volvo, Hyundai Motor Company, Xiamen King Long United Automotive Industry, Ashok Leyland, Zhongtong Bus, ANKAI, Daimler India, Bharat Benz, Mitsubishi, Fiat Chrysler Automobiles, Scania, UD Trucks Corp., Ford Motor Company, Toyota Motor Corporation, BYD Auto, Shaanxi Automobile Group, Beiqi Foton Motor Co., SAIC Motor Commercial Vehicle Co., MAN Truck & Bus SE, Irizar, Solaris, VDL, Gaz Group, NefAZ (KAMAZ affiliate), UAZ, Elegantbus, Cento Bus, Bus Factory, Pacific Tur, Lux Bus America, Vamoose Bus, Enel X Brazil, PSA, Temsa, Hafilat, Karsan, Otokar, Tata Motors, Cania AB

Recent Developments

Jan 2026 — Daimler Buses (Mercedes-Benz): Signed a new framework agreement for up to 500 battery-electric city buses with Belgium’s De Lijn, alongside an initial call-off order; deliveries are planned to start from 2027.

Dec 2025 — BYD Europe: Announced a new order for 268 electric buses from De Lijn under an existing framework agreement, strengthening its supply position in Belgium’s fleet electrification program.

Dec 2025 — Solaris Bus & Coach: Won Warsaw’s largest tender of the year to deliver 120 articulated buses, with deliveries beginning in H2 2026 and an option for additional units.

Dec 2025 — Solaris Bus & Coach: Secured an order for 20 Trollino trolleybuses for Lublin, with deliveries scheduled to be completed in the first months of 2027.

Dec 2025 — MAN Truck & Bus: Announced its largest-ever bus contract to supply over 3,000 buses to DB Regio in Germany (2027–2032), including a significant share of fully electric units.

Dec 2025 — Volvo Buses: Received an order for 73 new electric buses for operations in and around Borås, Sweden, with entry into service targeted for 2027.

Nov 2025 — Wrightbus: Launched the next generation Electroliner battery-electric bus, emphasizing higher efficiency and suitability for intensive urban duty cycles.

Nov 2025 — Wrightbus: Landed a major coach order (Contour) for Bus Éireann, marking a notable step in its re-entry into the coach segment with a low-emission product focus.

Oct 2025 — IVECO BUS: Signed framework agreements with Île-de-France Mobilités to supply up to 4,000 low- and zero-emission buses and coaches between 2026 and 2032 (battery-electric and CNG included).

Oct 2025 — MAN Truck & Bus: Debuted the Lion’s Coach E as its flagship move into zero-emission touring coaches, highlighting long-distance electrification as a new battleground for European OEMs.

Jul 2025 — NFI / New Flyer: Announced a significant battery-electric order from Ottawa’s OC Transpo for 124 Xcelsior CHARGE NG buses, reinforcing North American transit fleet electrification momentum.

FAQ's

The Global Buses And Coaches Market is estimated to generate USD 44.5 billion in revenue in 2026.

The Global Buses And Coaches Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.19% during the forecast period from 2026 to 2034.

The Buses And Coaches Market is estimated to reach USD 66.7 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!