"Global Canola Meal Market is valued at USD 528 billion in 2025. Further, the market is expected to grow at a CAGR of 6.8% to reach USD 952.8 billion by 2034."

The canola meal market is a vital segment within the animal feed industry, offering a high-quality protein source that supports livestock nutrition and productivity. Derived as a byproduct of canola oil extraction, canola meal is widely used in feeds for poultry, swine, cattle, and aquaculture species. With its favorable amino acid profile and digestibility, it has become a valuable component in the global feed supply chain.

Over the years, advancements in processing techniques have enhanced the nutritional quality of canola meal, making it an attractive alternative to other protein sources such as soybean meal. Additionally, ongoing research into optimizing feed formulations has highlighted canola meal’s role in improving growth rates and overall health in livestock. This increased focus on efficient and sustainable feeding solutions continues to drive market growth.

The market is particularly strong in regions with significant livestock and aquaculture industries, including North America, Europe, and Asia-Pacific. Canada, as one of the largest producers of canola, plays a central role in supplying high-quality meal to global markets. As demand for sustainably produced animal proteins grows, the canola meal market is poised to expand further, supported by innovations in production and increasing awareness of its benefits.

Key Insights

- Canola meal has evolved from a by-product of oil production into a strategically important protein ingredient in compound feeds. Its nutritional profile supports high performance in ruminants and non-ruminants when properly formulated, helping feed manufacturers reduce reliance on a single dominant protein source. This diversification is particularly valuable in periods of tight supply or price volatility for competing meals.

- The market’s development is closely tied to canola acreage, crop yields, and crushing capacity in key producing regions. When oil demand and crush margins are strong, meal availability rises, supporting wider use in feed rations. Conversely, weather-driven crop stress, disease pressure, or shifts in planting decisions can constrain meal supply and influence regional pricing dynamics.

- Dairy feed remains a cornerstone application, where canola meal is valued for its contribution to milk yield and protein content in well-balanced rations. Nutritionists increasingly integrate it into precision feeding models that optimize rumen function and nitrogen efficiency. Strong adoption in high-output dairy systems has helped build a robust base of performance data and formulation know-how.

- In poultry and swine, canola meal is typically used as part of a multi-protein strategy rather than a sole source, complementing soybean meal and other ingredients. Advances in processing and enzyme technology have improved digestibility and allowed higher inclusion rates without compromising growth performance. This supports feed cost management while maintaining carcass quality and health outcomes.

- Aquaculture represents a growing opportunity, as the sector seeks to reduce dependence on marine proteins and balance sustainability with growth needs. Canola meal, when combined with other plant proteins and appropriate amino acid supplementation, can support diets for species such as salmonids and warm-water fish. Work continues to fine-tune formulations that manage palatability, digestibility, and water quality.

- Sustainability narratives are gaining importance, with canola meal often positioned as part of lower-impact livestock production systems. Life-cycle assessments, carbon footprint calculations, and regenerative agriculture initiatives increasingly consider the role of oilseed meals in resource use efficiency. Crushers and feed companies highlight local sourcing, reduced land pressure, and alignment with climate and biodiversity targets.

- Technological innovation in plant breeding and processing is reshaping the quality profile of canola meal. New varieties targeting improved oil and protein characteristics, combined with optimized crushing conditions, enhance meal amino acid availability and reduce unwanted components. These improvements support more consistent performance and unlock higher-value applications in sensitive species and life stages.

- Trade flows and policy frameworks heavily influence regional market balances, as major exporting countries supply meal to deficit regions with intensive livestock sectors. Tariffs, sanitary and phytosanitary rules, and biotechnology regulations can affect competitiveness and market access. Logistics performance in rail, barge, and port operations is a key differentiator in meeting just-in-time feed mill requirements.

- Feed formulators are increasingly using digital tools and modelling software to evaluate canola meal’s role within cost and performance optimization scenarios. These platforms integrate up-to-date ingredient analyses, nutrient matrices, and animal response curves, enabling dynamic adjustments as prices and quality parameters shift. Such capabilities make it easier to justify and monitor higher or lower inclusion rates over time.

- Looking ahead, the canola meal market is expected to benefit from continued intensification of livestock production, growing scrutiny of feed sustainability, and the search for resilient protein supply chains. Opportunities are strongest in markets where technical support, transparent nutrition data, and reliable quality are available. Suppliers that invest in customer education, collaborative research, and differentiated product offerings are well positioned to capture future growth.

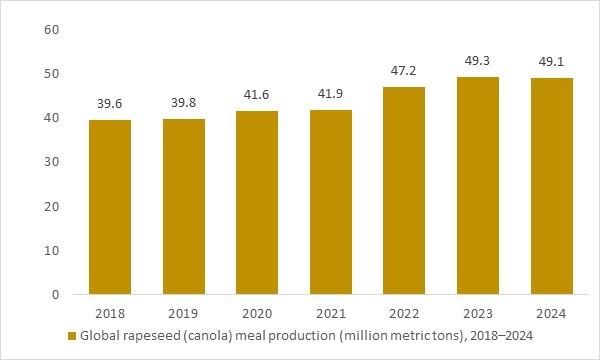

Global rapeseed (canola) meal production (million metric tons), 2018–2024

Figure : Global rapeseed (canola) meal production (million metric tons), 2018–2024. The steady increase in global canola meal output highlights the expanding protein meal base that underpins growth in the global canola meal market, especially across livestock and aquaculture feed applications.

- The chart highlights the steady increase in global rapeseed (canola) meal production from 2018 to 2024, reflecting the robust expansion of the raw material base supporting the canola meal market. This upward trend underscores the growing role of canola meal as a high-quality protein source across livestock and aquaculture feed applications, ultimately strengthening long-term market growth potential.

Regional Insights

North America Canola meal market

In North America, the canola meal market is anchored by Canada’s large canola crushing industry and strong feed demand in the United States and domestic Canadian livestock sectors. Meal is widely adopted in high-producing dairy rations, as well as in beef, poultry, and swine feed, supported by a robust evidence base and technical work from industry bodies and research groups. Growth in U.S. canola acreage, partly driven by biofuel-related oil demand, is increasing regional seed availability and underpins crush expansion, which in turn supports meal supply. Trade flows are evolving as Canadian exporters respond to shifting access in key Asian markets and diversify into other destinations. Large agribusinesses and crushing companies leverage integrated supply chains, rail and port logistics, and feed-technical support to maintain North America’s leadership in canola meal exports and utilization.

Europe Canola meal market

In Europe, canola (rapeseed) meal is an important protein source in compound feeds, particularly for dairy, beef, and monogastric animals in countries with strong oilseed crushing sectors. Demand is closely linked to broader animal feed market growth and the push to optimize protein use under tightening environmental regulations. Feed formulators increasingly consider greenhouse gas emissions, land use, and nutrient efficiency when selecting protein ingredients, which supports interest in locally available oilseed meals. Ongoing reforms in agricultural and sustainability policy encourage more efficient nutrient management and may favor balanced rations using regional oilseed meals over imported proteins in some markets. European feed companies emphasize consistent quality, contaminant control, and traceable supply chains, creating opportunities for canola meal where it can match or complement established protein sources.

Asia-Pacific Canola meal market

Asia-Pacific is a strategically important demand center for canola meal, driven by intensive dairy, poultry, swine, and aquaculture production in China, Southeast Asia, and parts of South Asia. Historically, China has been a major importer of Canadian canola and rapeseed meals, but recent trade measures and tariffs are reshaping sourcing patterns and opening space for alternative suppliers such as Australia and for re-exports to other regional buyers. Feed producers in countries like Vietnam and other Southeast Asian markets are capitalizing on competitively priced canola meal to diversify protein bases and manage feed costs. At the same time, aquafeed producers across the region are evaluating canola meal as a sustainable plant-protein option in fish diets, supported by ongoing research into digestibility, growth performance, and life-cycle impacts. As governments and industry stakeholders seek resilient, lower-footprint feed systems, Asia-Pacific is expected to remain a key growth region for canola meal usage.

Market Scope

| Parameter | Canola meal Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Poultry

- Swine

- Ruminants

- Aquatic animals

By Nature

- Organic

- Conventional

By Application

- Feed

- Fertilizer

- Food Additive

- Industrial Chemical

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Cargill Incorporated

- Archer Daniels Midland Company

- BASF SE

- Wilmar International Ltd.

- Bunge Global SA

- Louis Dreyfus Company

- Bayer AG

- CHS Inc.

- Charoen Pokphand Foods PCL

- Perdue Farms Inc.

- Koninklijke DSM N.V.

- Richardson International Limited

- Parrish & Heimbecker Limited

- MSM Milling

- LaBudde Group Inc.

- Sunora Foods Inc.

- AGRIM PTE LTD

- Aggarwal Impex Pvt. Ltd.

- Sunrise Foods Inc.

- East Coast Stockfeeds

- Annachtra International Organisation LLP

- Energrow Inc.

- Manishankar Oils Pvt. Ltd.

- Resaca Sun Feeds LLC

- Parkar Enterprise

FAQ's

The Global Canola Meal Market is estimated to generate USD 528 billion in revenue in 2025.

The Global Canola Meal Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period from 2025 to 2034.

The Canola Meal Market is estimated to reach USD 952.8 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!