"The Carbonated Beverage Processing Equipment Market was valued at $ 9.29 billion in 2025 and is projected to reach $ 21.55 billion by 2034, growing at a CAGR of 9.8%."

The carbonated beverage processing equipment market sits at the core of modern soft drinks, sparkling water, flavored carbonated drinks, energy beverages, mixers, and emerging “better-for-you” carbonated formulations. Equipment demand is primarily tied to beverage producers, contract packers, and brand owners expanding capacity or upgrading lines to improve hygiene, uptime, and packaging flexibility. Core process areas include water treatment and deaeration, syrup and ingredient handling, blending, carbonation systems, hygienic transfer, and downstream filling, capping/seaming, pasteurization or microbial control steps, labeling, and end-of-line packaging. Buyers increasingly evaluate solutions as an integrated line rather than isolated machines, prioritizing consistent carbonation accuracy, taste stability, fast changeovers, sanitation performance, and line efficiency across glass, cans, and plastic formats. Aftermarket support, availability of spares, operator training, and commissioning capability often weigh as heavily as equipment specifications, particularly where plants run high utilization and cannot afford unplanned stoppages.

Recent market momentum reflects a combination of product innovation and operational reinvention. Producers are leaning into modular and scalable line designs, higher automation, and digital tools that improve visibility into quality parameters such as dissolved gas control, blend precision, and in-line monitoring, while also reducing water, chemical, and energy intensity through smarter cleaning cycles and recovery practices. Packaging shifts toward cans, lightweight bottles, and multipack formats are pushing investments in flexible filling and packaging blocks, quicker format change parts, and better integration between process and packaging controls. Key drivers include expanding consumption of sparkling beverages, faster new-product launches that require agile manufacturing, stricter food safety expectations, and persistent labor constraints that favor automated, easier-to-run systems. Competition is led by global turnkey line suppliers and specialist process OEMs, alongside strong regional integrators; differentiation centers on hygienic design, throughput stability, lifecycle cost, service footprint, and controls/software that translate plant data into higher overall equipment effectiveness.

Key Market Insights

-

Packaging-led line investments (historic → current → future) The long-term shift from returnable glass toward PET and, more recently, cans has steadily reshaped equipment choices. Producers are prioritizing filler flexibility, faster format changeovers, and tighter integration between process and packaging. Future line designs increasingly favor “one line, many SKUs” capability. This reinforces demand for modular blocks and quick-change parts. End-of-line automation becomes a larger share of project scope.

-

Rise of sparkling water and flavored carbonation (current → future) Sparkling water growth and flavor innovation are driving more frequent recipe switches and shorter runs. This elevates the importance of precise blending, dosing, and carbonation control to maintain taste consistency. Equipment that supports rapid flavor change and minimal flavor carryover is gaining preference. Plants are adopting more hygienic, low-hold-up manifolds and smarter CIP sequencing. Applications expand beyond classic CSDs into premium and functional sparkling formats.

-

Carbonation accuracy and product stability as key differentiators Brands increasingly compete on mouthfeel, “bite,” and sensory consistency, pushing tighter control over CO₂ dissolution and temperature management. Deaeration performance, in-line measurement, and closed-loop control systems are becoming standard requirements. Future improvements focus on real-time quality monitoring and reduced variability across shifts. This benefits advanced carbonation skids, inline sensors, and more stable process control architectures. It also increases the value of OEM process know-how and commissioning expertise.

-

Hygienic design and food-safety expectations accelerating upgrades Over time, hygiene standards have moved from compliance to brand protection, influencing equipment materials, surface finishes, drainability, and validation. Today’s buyers emphasize sanitary construction, dead-leg minimization, and robust CIP coverage. Future regulatory and customer audits will further reward traceable, data-backed sanitation performance. This drives demand for hygienic valves, fittings, inline filtration, and validated cleaning systems. It also strengthens the aftermarket for audits, retrofits, and hygiene optimization.

-

Automation and digitalization shifting from optional to essential Historically, many plants relied on manual checks and operator experience; modern operations increasingly require automated control and dashboards. Current investments target OEE improvement, downtime reduction, and faster troubleshooting through connected sensors and analytics. Future systems will expand predictive maintenance, remote support, and recipe governance across multi-site networks. Integration between PLC/SCADA, MES, and quality systems becomes a differentiator. Cybersecurity and data integrity rise as key selection criteria.

-

Energy, water, and chemical efficiency reshaping total cost of ownership Operating efficiency has become a stronger decision factor as utilities and sustainability targets tighten. Producers are focusing on optimized CIP cycles, water reuse, heat recovery, and compressed-air management. Future projects will embed resource-efficiency metrics into line acceptance and KPI frameworks. Equipment suppliers that can guarantee repeatable cleaning outcomes with less resource use gain advantage. This especially influences water treatment, CIP skids, and utility-intensive packaging equipment.

-

Speed-to-market driving agile manufacturing and flexible asset design The market has evolved from stable, high-volume SKUs to frequent launches and limited editions. Current projects prioritize modular mixing systems, scalable syrup rooms, and faster changeovers to reduce time between product concepts and shelf-ready output. Future competitiveness depends on rapid commissioning, validated recipes, and minimal ramp-up losses. This supports compact, standardized platforms that can be replicated across plants. Co-packers benefit disproportionately due to multi-brand complexity.

-

Functional and “better-for-you” formulations complicating processing needs Reduced sugar, natural flavors, acid systems, and functional ingredients can increase sensitivity to shear, oxygen, or temperature. Equipment must handle diverse ingredients while protecting quality and minimizing foaming or flavor degradation. Going forward, more complex formulations will raise the importance of gentle handling, precise dosing, and robust inline monitoring. This boosts demand for high-accuracy metering, hygienic ingredient handling, and improved filtration. It also increases validation and change-control requirements.

-

Competitive landscape favoring full-line capability plus strong service networks Historically, local integrators competed on cost; today, global OEMs and top regional players win on turnkey execution, standardized platforms, and lifecycle support. Buyers increasingly prefer suppliers that can deliver end-to-end integration—process, filling, and packaging—with performance guarantees. Future competition will intensify around service responsiveness, spares availability, and remote diagnostics. The aftermarket (retrofits, upgrades, line audits) becomes a strategic battleground. Partnerships between process specialists and packaging OEMs continue to strengthen.

-

Regional investment patterns and localization of spares/services shaping vendor selection Mature markets often emphasize upgrades, efficiency, and automation, while emerging markets drive greenfield capacity and cost-optimized lines. Local compliance, utilities reliability, and workforce skill levels influence equipment robustness and automation depth. Future growth will favor vendors that localize service teams, training, and parts depots while maintaining global quality standards. This improves uptime and reduces commissioning risk for customers. It also encourages platform standardization with region-specific configurations.

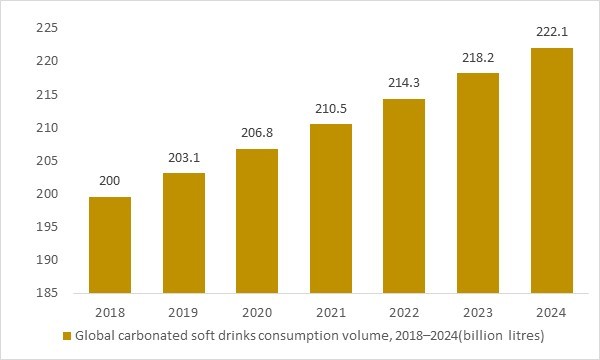

Global carbonated soft drinks consumption volume, 2018–2024(billion litres)

Figure: Global carbonated soft drink consumption increased from about 200 billion litres in 2018 to more than 220 billion litres in 2024, indicating sustained throughput growth across carbonation, blending, filling and packaging lines. This rising CSD volume directly supports investments in high-speed processing equipment, including automated carbonation systems, advanced PET and can filling lines, and integrated quality-control solutions, shaping the long-term expansion of the carbonated beverage processing equipment market.

- Global demand for carbonated soft drinks has steadily increased from around 199.6 billion litres in 2018 to more than 218 billion litres in 2023, with volumes expected to exceed 222 billion litres in 2024. This sustained rise in production and consumption directly expands throughput requirements across carbonation, mixing, filling, capping and packaging lines. As beverage manufacturers introduce more low-sugar, flavoured and premium CSD variants, the need for flexible, high-speed and hygienic processing equipment grows further. These structural volume and SKU trends create a strong, long-term demand base for carbonated beverage processing equipment worldwide.

Regional Insights

North America

North America’s carbonated beverage processing equipment market is driven by strong consumption of soft drinks, sparkling water, energy drinks, and flavored carbonated beverages, alongside continuous product innovation by major beverage brands. Market dynamics emphasize high-speed production efficiency, hygiene compliance, automation, and flexibility to handle multiple SKUs and packaging formats. Manufacturers prioritize advanced carbonation systems, mixing and blending units, filtration equipment, pasteurization systems, and automated filling lines that ensure consistent taste and quality. Lucrative opportunities are strongest in plant modernization projects, craft and premium beverage startups, and health-oriented sparkling drink segments. Latest trends include integration of IoT-enabled monitoring systems, energy-efficient compressors, reduced water usage technologies, and modular equipment designs that enable rapid product changeovers. The outlook remains steady as demand for diversified carbonated offerings continues, with recent developments focused on digital production controls, predictive maintenance solutions, and sustainable processing technologies.

Asia Pacific

Asia Pacific represents the fastest-growing region due to rising urbanization, expanding middle-class consumption, and strong beverage manufacturing capacity. Market dynamics prioritize scalable production lines, cost optimization, and adaptability to regional flavor variations. Lucrative opportunities lie in new bottling plants, expansion of ready-to-drink carbonated beverages, and private-label production serving both domestic and export markets. Trends include increased adoption of fully automated processing lines, investment in compact carbonation systems for mid-sized manufacturers, and growing focus on hygiene and safety standards. The forecast remains robust as beverage consumption grows across emerging economies, with recent developments centered on capacity expansion, advanced mixing technologies, and partnerships between equipment suppliers and regional beverage producers.

Europe

Europe’s carbonated beverage processing equipment market is shaped by mature consumption patterns, strong regulatory standards, and growing demand for low-sugar and functional sparkling beverages. Market dynamics emphasize sustainability, energy efficiency, and compliance with food safety and environmental regulations. Lucrative opportunities are concentrated in plant upgrades to reduce carbon footprint, expansion of premium sparkling water brands, and equipment tailored for reduced sugar and natural ingredient formulations. Latest trends include development of low-energy carbonation systems, closed-loop water recycling solutions, and enhanced process automation for traceability. The outlook is steady and innovation-driven as beverage companies focus on product differentiation and operational efficiency, with recent developments centered on eco-friendly processing solutions, digital integration, and flexible manufacturing systems.

Middle East & Africa

Middle East & Africa demand is influenced by expanding urban populations, rising disposable incomes, and growth in hospitality and retail sectors. Market dynamics emphasize durability in high-temperature environments, water efficiency, and reliable high-capacity bottling systems. Lucrative opportunities are strongest in new beverage production facilities, regional expansion of multinational brands, and growth in flavored sparkling drinks tailored to local tastes. Trends include adoption of robust carbonation and filling technologies suited to harsh climates, increased investment in modern processing plants, and stronger distributor partnerships for equipment servicing. The outlook remains positive as consumer demand for carbonated beverages grows, with recent developments focused on plant automation, improved energy management systems, and localized equipment assembly.

South & Central America

South & Central America’s carbonated beverage processing equipment market is supported by strong regional beverage brands, expanding bottling operations, and increasing demand for soft drinks and sparkling beverages. Market dynamics highlight cost efficiency, reliability, and scalability to serve both domestic consumption and export markets. Lucrative opportunities exist in modernization of aging bottling lines, growth of private-label beverage production, and expansion into flavored and functional carbonated drinks. Latest trends include greater adoption of automated blending and carbonation systems, improved hygienic design standards, and investment in energy-efficient processing technologies. The outlook remains steadily positive as beverage production capacity expands, with recent developments centered on production optimization, improved quality control systems, and integration of digital monitoring across processing operations.

Market Scope

| Parameter | Carbonated Beverage Processing Equipment Market Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Diagnostic Method, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Carbonated Beverage Processing Equipment Market Segments Covered In The Report

By Equipment Type

- Sugar Dissolvers

- Carbonation Equipment

- Blender And Mixers

- Heat Exchangers

- Silos

- Filtration Equipment

By Beverage Type

- Flavored Drinks

- Functional Drinks

- Club Soda And Sparkling Water

By Distribution Channel

- Original Equipment Manufacturer

- Aftermarket Sales

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Covered

Tetra Laval International SA, GEA Group AG, Alfa Laval Group, Krones AG, SPX flow inc., KHS GmbH, A Due Di Squeri Donato & Cspa, Van Der Molen GmbH, Seppelec SL, TCP Pioneer Co. Ltd., A Water System srl, Pentair plc, Shreeji Projects, Roquette Frères, Mitsui Sugar Co.Ltd., Archer-Daniels-Midland Company, Tate & Lyle plc, Pyure Brands LLC, PureCircle, Ajinomoto Health & Nutrition North America Inc., Goma Engineering Pvt. Ltd., Tetra Pak International S.A., PepsiCo Inc., The Coca-Cola Company, Keurig Dr Pepper Inc., Britvic plc, National Beverage Corp., Parle Agro Private Limited, The Pepsi Bottling Group, The Dr. Pepper Snapple Group .

Recent Industry Developments

- August 2025: Beverage industry veterans launched Pittston Co-Packers, a 403,000 sq.ft. contract manufacturing and packaging facility in Pennsylvania, designed to support large-scale production for carbonated beverages and ready-to-drink products.

- February 2025: Equipment manufacturers introduced new-generation processing systems equipped with enhanced automation, smart monitoring features, and IoT integration to meet growing demand for diversified carbonated beverage formulations.

- June 2024: Rotarex Solutions released the BubbleBox Carbo Pro, an advanced inline carbonation system targeting hospitality venues, offering consistent and scalable sparkling water production with minimal installation footprint.

What You Receive

• Global Carbonated Beverage Processing Equipment market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Carbonated Beverage Processing Equipment.

• Carbonated Beverage Processing Equipment market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Carbonated Beverage Processing Equipment market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Carbonated Beverage Processing Equipment market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Carbonated Beverage Processing Equipment market, Carbonated Beverage Processing Equipment supply chain analysis.

• Carbonated Beverage Processing Equipment trade analysis, Carbonated Beverage Processing Equipment market price analysis, Carbonated Beverage Processing Equipment Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Carbonated Beverage Processing Equipment market news and developments.

The Carbonated Beverage Processing Equipment Market international scenario is well established in the report with separate chapters on North America Carbonated Beverage Processing Equipment Market, Europe Carbonated Beverage Processing Equipment Market, Asia-Pacific Carbonated Beverage Processing Equipment Market, Middle East and Africa Carbonated Beverage Processing Equipment Market, and South and Central America Carbonated Beverage Processing Equipment Markets. These sections further fragment the regional Carbonated Beverage Processing Equipment market by type, application, end-user, and country.

FAQ's

The Global Carbonated Beverage Processing Equipment Market is estimated to generate USD 9.29 billion in revenue in 2025.

The Global Carbonated Beverage Processing Equipment Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% during the forecast period from 2025 to 2034.

The Carbonated Beverage Processing Equipment Market is estimated to reach USD 21.55 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!