"The Catamarans Market was valued at $ 2.0 billion in 2026 and is projected to reach $ 3.1 billion by 2034, growing at a CAGR of 5.6%."

The Catamarans Market has evolved into a diverse marine segment spanning sailing catamarans, power catamarans, luxury cruising platforms, charter vessels, passenger ferries, and selected patrol and special-mission craft. Its appeal is rooted in the catamaran hull form’s stability, space efficiency, shallow draft, and fuel-conscious operating profile, which make it attractive across leisure, tourism, transport, and niche commercial applications. The strongest end uses today include private cruising, yacht charter, resort and island tourism, premium liveaboard travel, commuter and inter-island ferry services, and high-comfort motor yachting. Recent market direction shows clear momentum toward larger luxury platforms, more refined interior-volume concepts, and a rising wave of electric, hybrid, and eco-navigation solutions. New product launches from Lagoon and Fountaine Pajot, along with continued investment in eco-focused platforms from Sunreef, show that innovation is spreading across both mainstream and premium catamaran categories.

Growth is being driven by rising interest in experiential marine leisure, stronger charter demand for spacious multihulls, expanding premium power-catamaran ownership, and increasing use of catamaran platforms in clean passenger transport. The competitive landscape is led by established leisure builders, custom luxury shipyards, and specialized ferry manufacturers competing on design, performance, range, onboard comfort, sustainability, and application-specific engineering. A notable trend is the widening split between cruising and charter-oriented leisure models on one side and electric or high-speed passenger catamarans on the other, with both segments benefiting from technology-led differentiation. The market outlook remains favorable as builders continue to launch fresh platforms, upgrade propulsion options, and align catamaran design with sustainability, passenger comfort, and operational efficiency. Recent developments from Aquila, Incat, and other multihull specialists reinforce that the market is moving from a niche preference toward a broader, innovation-led marine category.

Regional Analysis

North America Catamarans Market

The North America Catamarans Market is being driven by a mix of premium leisure boating, charter activity, coastal cruising, fishing-oriented multihulls, and growing interest in cleaner passenger-water transport. Market dynamics increasingly favor companies that can deliver power catamarans with greater onboard volume, easier handling, longer-range comfort, and lifestyle-oriented layouts, while commercial opportunities are emerging around electric ferry and resort-transfer applications. The latest trend is the widening appeal of power catamarans beyond niche buyers, supported by fresh model launches, stronger show visibility, and product expansion by brands such as Aquila and Leopard, alongside early commercial-electric ferry adoption in places such as Lake Tahoe. The forecast remains favorable as buyers continue to value stability, space efficiency, and fuel-conscious cruising, while companies that combine premium leisure design with lower-emission propulsion and strong dealer reach are likely to find the most attractive opportunities in the region.

Asia Pacific Catamarans Market

The Asia Pacific Catamarans Market is evolving through a dual growth path that combines leisure and tourism demand with a strong commercial-ferry and island-connectivity opportunity. Market dynamics are being shaped by inter-island passenger transport, resort mobility, coastal tourism, and a rising willingness to adopt electric and hybrid catamaran platforms where operating efficiency and sustainability matter. The latest trend is the acceleration of advanced ferry programs, with Thailand positioned for electric hydrofoil ferry deployment and Australia reinforcing its role as a leader in large catamaran and electric-ferry construction through Incat’s latest battery-electric and hybrid-electric programs. The forecast remains highly positive, in our view, because the region offers both scale in passenger transport and increasing appetite for innovative marine platforms, creating lucrative openings for builders, propulsion suppliers, charging-system providers, and premium leisure-catamaran brands.

Europe Catamarans Market

The Europe Catamarans Market remains one of the most advanced and diversified regional markets, supported by strong sailing and charter culture, premium private ownership, and accelerating innovation in low-emission passenger catamarans. Market dynamics favor companies that can serve both the leisure and transport sides of the market, with attractive opportunities in next-generation cruising catamarans, upscale power catamarans, and electric commuter or coastal ferry platforms. The latest trend is the clear split between lifestyle-led model innovation from established builders such as Fountaine Pajot, Lagoon, and Jeanneau, and the commercialization of cleaner public-transport catamarans, highlighted by Candela’s expanding Stockholm ferry service and record electric sea voyage from Sweden to Oslo. The forecast remains robust as Europe continues rewarding technical sophistication, sustainability, and premium onboard design, making it a key region for companies that can align comfort, efficiency, and low-emission marine mobility.

Middle East & Africa Catamarans Market

The Middle East & Africa Catamarans Market is developing through luxury-yachting demand in the Gulf and a strong production and export base in South Africa, creating a regional profile that combines premium consumption with manufacturing capability. Market dynamics are being shaped by tourism-led yachting demand, marina and boat-show activity, and increasing interest in innovative multihull formats, including electric and hybrid luxury catamarans. The latest trend is the region’s growing visibility as both a showcase market and a build base, with Sunreef expanding its UAE footprint and highlighting catamarans at the Dubai International Boat Show, while Robertson & Caine continues to anchor Africa’s manufacturing role through large-scale catamaran production in Cape Town. The forecast is constructive, especially in the Gulf and South Africa, and the most lucrative opportunities are likely to be in luxury power cats, eco-positioned catamarans, charter fleets, and marine services linked to regional boating infrastructure.

South & Central America Catamarans Market

The South & Central America Catamarans Market is smaller than North America or Europe in leisure-boat depth, but it presents a compelling opportunity through coastal tourism, private cruising, and especially high-profile passenger-ferry deployment. Market dynamics are increasingly influenced by the region’s need for efficient intercity and cross-water transport, which supports the commercial case for larger catamaran ferries, while the leisure side benefits from gradual premiumization and wider awareness of multihull comfort and stability. The latest trend is the strengthening of electric-ferry relevance, led by Buquebus’s upcoming battery-electric catamaran on the Buenos Aires–Colonia route, which signals that clean multihull transport is becoming a serious regional opportunity rather than a distant concept. The forecast is positive but selective, with the best company opportunities likely to emerge in premium leisure catamarans, ferry design and support, and marine services tied to tourism and short-sea passenger connections.

Key Insights

- Leisure cruising remains the structural foundation of the Catamarans Market, with sailing catamarans continuing to attract private owners and charter operators because they offer space, comfort, and easy onboard living. Recent model introductions from Lagoon and Fountaine Pajot show that builders are still investing heavily in this segment, especially in blue-water and family-cruising formats.

- Power catamarans are becoming a stronger growth pillar as buyers seek more volume, easier handling, and luxury motor-yacht comfort without giving up the efficiency and stability advantages of multihulls. This is widening the market beyond sailing enthusiasts and creating stronger demand from premium leisure users, charter operators, and owners focused on long-range comfort.

- Electrification is emerging as one of the most important long-term technology themes in the market. From Sunreef’s eco-focused luxury concepts to VisionF’s delivered electric catamaran and Incat’s major battery-electric ferry program, suppliers are clearly pushing the hull format as a natural fit for lower-emission marine transport and leisure innovation.

- Passenger ferry applications continue to strengthen the commercial side of the market because catamarans provide speed, deck area, and ride stability that are well suited to commuter and inter-island transport. Recent electric-ferry developments from Incat and EV Maritime show that catamarans are becoming increasingly relevant to clean public transport and short-route marine mobility.

- Premiumization is reshaping product strategy across the market, with builders moving toward larger layouts, more lifestyle-oriented deck plans, and stronger luxury positioning. This is visible in recent and upcoming launches from Fountaine Pajot and Lagoon, which are expanding further into upscale cruising and high-end yacht territory.

- Hybrid propulsion and eco-navigation are becoming more visible differentiators even in leisure-oriented models. Aquila’s hybrid sailing entry and broader eco-branding from premium multihull builders suggest that future competition will increasingly depend on how well builders combine performance, onboard comfort, and lower-impact propulsion strategies.

- The market is broadening into multiple distinct product pathways rather than following a single demand pattern. Sailing cruisers, power cats, luxury eco-yachts, commuter ferries, and special-mission multihulls now operate as parallel opportunities, which benefits manufacturers that can serve more than one use case through adaptable design and engineering capability.

- Competitive advantage is shifting toward builders that can refresh model ranges quickly, support sustainability narratives credibly, and align design with specific user profiles such as charter guests, private cruisers, and ferry operators. The strongest future positions are likely to belong to companies combining brand strength, technical innovation, and clear segmentation strategy across leisure and commercial multihull demand.

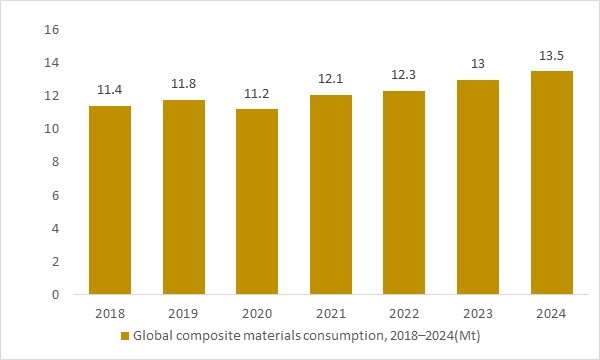

Global composite materials consumption, 2018–2024(Mt)

Figure: Global composite materials consumption increased from about 11.4 million tonnes in 2018 to an estimated 13.5 million tonnes in 2024, reflecting rising demand for lightweight, high-strength fiberglass and carbon-fiber systems. These materials form the core structural base for modern catamaran hulls, decks and superstructures, enabling improved performance, reduced vessel weight and enhanced fuel efficiency. OG Analysis estimates, derived from global composites industry data, highlight how expanding composites availability directly supports production capacity, innovation and long-term growth potential in the catamarans market.

- Global composite materials consumption rose steadily from 2018 to 2024, highlighting the expanding availability of lightweight, high-strength FRP and carbon-fiber systems widely used in modern catamaran hulls and superstructures. This consistent upstream growth supports enhanced design efficiency, weight reduction and performance improvements, reinforcing the positive production outlook for the global catamarans market.

Report Scope

| Parameter | Catamarans Market |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Catamarans Market Segmentation

By Product

- Sailing Catamarans

- Powered Catamarans

By Size

- Small (below 15m)

- Medium (15m-30m)

- Large (above 30m)

By Application

- Leisure

- Commercial

- Defense

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Companies Analysed

African Cats B V, Voyage Yachts Ltd., Bavaria Yachtbau GmbH, Catana Group SA, Seawind Group Holdings Pty Ltd., Outremer Catamarans, Fountaine Pajot SA, LeisureCat & AussieCat, Robertson & Caine Ltd., Matrix Yachts Ltd., Catathai Co. Ltd., Lagoon Catamarans, Incat Crowther Pty Ltd., Craig Loomes Design Group ltd., Aresa Shipyard SL, Leopard Catamarans, Beneteau SA, Nautitech Catamaran, Privilege Catamarans, Antares Catamarans, Gemini Catamarans, Kinetic Catamarans, Aquila Inc., Baraca Planet S.L., Pedigree Cats Inc., Scape Yachts, The Matrix, Travelopia Group, Nichols Brothers Boat Builders LLC, Corinthian Yachts Inc., World Cat Ltd., Alumarine Shipyard, iXblue SAS .

Recent Industry Developments

March 2026 – Aquila Catamarans: Aquila announced the European debut of its new 50 Sail at the International Multihull Show, alongside a broader display of power catamarans. The move is important because it strengthens Aquila’s expansion from power-only platforms into sail catamarans and broadens competitive options in the cruising multihull segment.

February 2026 – Sunreef Yachts: Sunreef unveiled its “Beyond 2030” strategy, pairing strong 2025 performance with a major industrial expansion program across Gdańsk and Ras Al Khaimah. This matters for the catamarans market because it signals added production capacity, continued premiumization, and stronger long-term investment in luxury multihulls.

February 2026 – Groupe Beneteau: Groupe Beneteau acquired Sailing Atlantic Services and confirmed development of a new service center in Les Sables d’Olonne focused in part on Lagoon and Excess catamarans. The development is notable because it expands commissioning, customization, and after-sales capacity for catamaran customers and charter fleets.

February 2026 – Austal: Austal began construction of Gotlandsbolaget’s 130-meter hydrogen-ready Horizon X high-speed catamaran at its Philippines shipyard. The project is important because it advances next-generation low-emission ferry catamarans and raises the scale of sustainable commercial multihull construction.

January 2026 – Aquila Catamarans: Aquila announced world debuts for the new 50 Sail and 45 Sport at the Miami International Boat Show. This is a major market development because it expands Aquila’s product reach across both sail and sport-oriented power catamarans, increasing competition in premium recreational multihulls.

January 2026 – Incat: Incat said the world’s largest battery-electric catamaran ferry began harbour trials in Hobart under its own electric propulsion. The milestone is significant because it moves large electric catamarans closer to commercial deployment and demonstrates growing technical maturity in zero-emission fast-ferry design.

January 2026 – Groupe Beneteau: Groupe Beneteau said it was accelerating catamaran-related launches, highlighting the Lagoon 38 and Excess 13, while JEANNEAU formally entered the motor multihull segment with the TH33 and TH38. The move matters because it expands product choice across both sailing and motor catamarans and signals deeper investment by a leading global boat group.

December 2025 – Incat: Incat announced the first successful e-motor trial for the world’s largest battery-electric catamaran ferry. This is important for the market because it confirms battery-electric propulsion is moving beyond small craft and into high-capacity commercial catamarans.

December 2025 – Incat: Incat and Molslinjen signed a contract for a third battery-electric high-speed ferry, expanding what the companies described as the world’s largest electrification project at sea. The development is notable because repeat ordering validates operator confidence in large electric catamaran ferry economics and performance.

August 2025 – Sunreef Yachts: Sunreef announced construction of a fully custom 49-meter catamaran superyacht, describing it as the most voluminous luxury catamaran ever launched and the largest superyacht built in Poland to date. The move is important because it pushes the size, complexity, and prestige ceiling of the luxury catamaran segment.

July 2025 – Incat: Incat secured a landmark contract from Molslinjen to design and build two 129-meter battery-electric ferries for Denmark. This is a major development because it reinforces demand for large zero-emission catamaran ferries in Europe and strengthens the commercial pipeline for electric multihulls.

FAQ's

The Global Catamarans Market is estimated to generate USD 2.0 billion in revenue in 2026.

The Global Catamarans Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.61% during the forecast period from 2026 to 2034.

The Catamarans Market is estimated to reach USD 3.1 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!