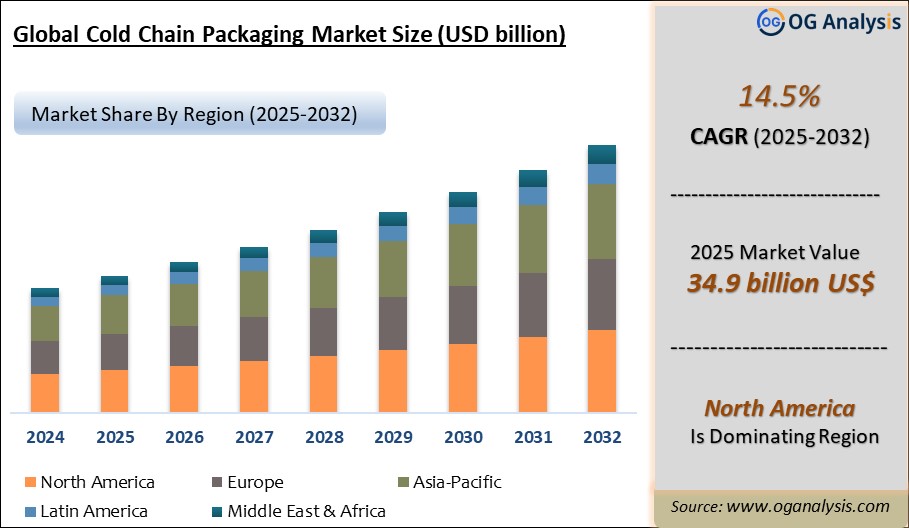

"The Cold Chain Packaging Market is valued at $ 40 billion in 2026 Worldwide sales of Cold Chain Packaging are expected to grow at a significant CAGR of 14.5%, reaching $ 121.4 billion by the end of the forecast period in 2034."

The Cold Chain Packaging Market is a critical segment of temperature-controlled logistics, supporting the safe storage, handling, and transportation of products that require stable thermal conditions across the supply chain. Cold chain packaging includes insulated boxes, thermal shippers, temperature-controlled containers, phase change materials, gel packs, dry ice packaging, vacuum insulated panels, refrigerated packaging systems, pallet shippers, and passive or active temperature-control solutions. These products are widely used in pharmaceuticals, biologics, vaccines, clinical trial materials, cell and gene therapies, diagnostics, specialty chemicals, fresh food, seafood, dairy, meat, frozen foods, and e-commerce grocery delivery. Demand is driven by rising pharmaceutical distribution, biologics commercialization, global vaccine movement, cross-border food trade, online grocery growth, and stricter product safety requirements. As supply chains become more global and quality-sensitive, companies increasingly rely on validated packaging systems that maintain product integrity, reduce spoilage, prevent temperature excursions, and support regulatory compliance.

The competitive landscape of the Cold Chain Packaging Market includes packaging manufacturers, thermal insulation specialists, pharmaceutical logistics providers, temperature-controlled container suppliers, material science companies, reusable packaging providers, and third-party logistics companies. Companies compete through thermal performance, validation support, payload flexibility, sustainability, reusability, cost efficiency, tracking integration, lightweight design, and ability to serve different temperature ranges. Latest trends include reusable thermal packaging, recyclable insulation materials, advanced phase change materials, real-time temperature monitoring, smart packaging, dry ice optimization, sustainable shipper design, and specialized packaging for biologics and cell and gene therapies. Growth is supported by increasing demand for reliable healthcare logistics, stricter food safety standards, expansion of direct-to-patient medicine delivery, and rising need for efficient last-mile temperature control. However, challenges include high packaging cost, reverse logistics complexity for reusable systems, material disposal concerns, dry ice handling limitations, regulatory validation requirements, and the need to balance performance with sustainability. The market outlook remains strong as healthcare, food, and specialty product supply chains continue prioritizing safety, traceability, compliance, and temperature assurance.

Regional Analysis

North America Cold Chain Packaging Market

North America Cold Chain Packaging Market is driven by strong pharmaceutical distribution, biologics commercialization, vaccine logistics, specialty drug delivery, frozen food trade, and expanding e-commerce grocery services. Market dynamics are shaped by strict product safety requirements, advanced healthcare supply chains, high adoption of validated thermal shippers, and increasing demand for reusable and sustainable packaging systems. Lucrative opportunities exist for thermal packaging manufacturers, phase change material suppliers, temperature-monitoring companies, pharmaceutical logistics providers, and reusable container service providers. Latest trends include recyclable insulation, real-time shipment tracking, reusable pallet shippers, dry ice optimization, and direct-to-patient cold chain delivery. The forecast outlook remains favorable as healthcare, food, and life sciences companies continue prioritizing temperature assurance, regulatory compliance, and supply-chain reliability.

Asia Pacific Cold Chain Packaging Market

Asia Pacific Cold Chain Packaging Market is expanding due to rising pharmaceutical manufacturing, growing biologics demand, vaccine distribution, food exports, online grocery growth, and rapid development of temperature-controlled logistics networks. Market dynamics are supported by increasing demand for insulated boxes, gel packs, thermal liners, passive packaging, and active temperature-controlled containers across healthcare and perishable food supply chains. The region presents strong opportunities for packaging suppliers, cold chain logistics providers, material science companies, seafood exporters, dairy processors, and pharmaceutical distribution partners. Latest trends include localized thermal packaging production, sustainable shipper designs, smart temperature indicators, and packaging solutions suited to long-distance and last-mile delivery. The forecast remains positive as regional trade, healthcare access, and quality-sensitive product movement continue increasing.

Europe Cold Chain Packaging Market

Europe Cold Chain Packaging Market is shaped by mature pharmaceutical logistics, strict food safety regulations, sustainability-focused packaging policies, and strong demand for temperature-controlled transport of biologics, clinical trial materials, frozen foods, dairy, seafood, and specialty medicines. Market dynamics are influenced by regulatory compliance, carbon reduction goals, reusable packaging adoption, and growing preference for recyclable or low-waste insulation materials. Lucrative opportunities exist for companies offering reusable thermal containers, advanced phase change materials, validated packaging systems, tracking technologies, and environmentally responsible cold chain solutions. Latest trends include circular packaging models, paper-based insulation, connected temperature monitoring, controlled room temperature packaging, and optimized distribution for high-value healthcare products. The forecast outlook remains steady as companies focus on compliance, sustainability, efficiency, and reliable cold chain performance.

Middle East & Africa Cold Chain Packaging Market

Middle East & Africa Cold Chain Packaging Market is developing through healthcare infrastructure growth, pharmaceutical imports, vaccine distribution, food security initiatives, fresh food trade, seafood logistics, and expansion of modern retail and e-commerce channels. Market dynamics vary across the region, with Gulf countries investing in advanced temperature-controlled logistics and high-quality pharmaceutical distribution, while African markets present opportunities through vaccine programs, fresh produce exports, and improving cold storage networks. Companies can benefit by offering durable, cost-effective, heat-resistant, and easy-to-handle cold chain packaging solutions for challenging climates and long transport routes. Latest trends include insulated pharmaceutical shippers, gel pack systems, reusable containers, temperature monitoring, and packaging for last-mile healthcare delivery. The forecast remains constructive as demand for safe medicines, quality food distribution, and reliable cold chain infrastructure continues to rise.

South & Central America Cold Chain Packaging Market

South & Central America Cold Chain Packaging Market is supported by pharmaceutical distribution, vaccine logistics, meat and seafood exports, fresh produce trade, dairy products, frozen foods, and growing retail modernization. Market dynamics are shaped by the need to reduce spoilage, maintain medicine integrity, improve export quality, and strengthen temperature-controlled transport across diverse climates and long-distance routes. Opportunities exist for thermal packaging manufacturers, logistics companies, food exporters, pharmaceutical distributors, reusable packaging providers, and temperature-monitoring solution suppliers. Latest trends include insulated packaging for perishables, validated healthcare shippers, dry ice and gel pack optimization, reusable packaging trials, and cold chain solutions for regional export corridors. The forecast outlook remains positive as healthcare supply chains, food exports, and modern retail distribution continue advancing across the region.

Key Insights

- The pharmaceutical and biologics sectors are among the strongest drivers of the Cold Chain Packaging Market, as many therapies require strict temperature control from manufacturing to final delivery. Vaccines, insulin, monoclonal antibodies, clinical trial supplies, and specialty drugs depend on validated packaging systems to prevent temperature excursions. This creates sustained demand for high-performance thermal shippers, phase change materials, and temperature-monitoring solutions.

- Reusable cold chain packaging is gaining strong attention as companies seek to reduce packaging waste, improve lifecycle value, and align logistics operations with sustainability goals. Reusable thermal containers and returnable shippers are especially attractive for high-value pharmaceutical and biologics distribution. However, successful adoption depends on reverse logistics, asset tracking, cleaning, inspection, and reliable return-management systems.

- Phase change materials are becoming increasingly important because they offer more stable and predictable temperature control compared with conventional cooling materials. These materials are used to maintain chilled, frozen, controlled room temperature, and ultra-low temperature conditions across different shipment durations. Their adoption is growing in healthcare logistics, specialty chemicals, and premium food distribution.

- E-commerce grocery and meal delivery are expanding demand for cold chain packaging in food and beverage applications. Consumers increasingly expect fresh, frozen, chilled, and ready-to-cook products to arrive safely and in good condition. This trend is encouraging companies to invest in lightweight insulated packaging, recyclable liners, gel packs, and last-mile temperature-control solutions.

- Cell and gene therapy logistics are creating specialized opportunities for advanced cold chain packaging providers. These therapies often require highly controlled, time-sensitive, and ultra-low-temperature shipping conditions with strong chain-of-custody visibility. Packaging suppliers that can support validated performance, secure handling, real-time monitoring, and regulatory documentation are gaining strategic relevance.

- Sustainability is becoming a major purchasing factor as companies face pressure to reduce single-use plastics, foam insulation, and landfill waste. Demand is increasing for recyclable, compostable, paper-based, plant-based, and reusable insulation materials. Vendors that can deliver both strong thermal performance and lower environmental impact are better positioned in food, healthcare, and e-commerce channels.

- Real-time temperature monitoring is increasingly integrated into cold chain packaging to improve shipment visibility and reduce product loss. Data loggers, connected sensors, GPS tracking, and cloud-based monitoring platforms help companies detect excursions and verify compliance. This is particularly important for pharmaceuticals, clinical trials, vaccines, and high-value perishable products.

- Dry ice packaging remains important for frozen and ultra-low-temperature logistics, but handling, availability, safety, and regulatory concerns are encouraging companies to optimize dry ice use. Packaging designs that reduce dry ice consumption while extending temperature hold times are becoming more valuable. This trend is especially relevant for biologics, vaccines, and specialty laboratory shipments.

- Food safety regulations and quality expectations are strengthening demand for reliable cold chain packaging in seafood, meat, dairy, frozen foods, fresh produce, and premium meal kits. Packaging helps reduce spoilage, maintain freshness, and protect brand reputation during distribution. Growth in cross-border food trade further supports demand for validated and durable thermal packaging systems.

- Competition is shifting toward integrated cold chain solutions that combine packaging design, thermal testing, validation, monitoring, reuse programs, and logistics support. Customers increasingly prefer suppliers that can provide complete temperature assurance rather than standalone packaging materials. Companies with strong engineering capabilities, sustainability credentials, global support, and regulatory expertise are expected to gain stronger market positioning.

Reort Scope

| Parameter | Cold Chain Packaging Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Product Type

- EPS Containers

- PUR Containers

- Pallet Shippers

- Vacuum Insulated Panels

- Others

By End User

- Food Packaging

- Healthcare Packaging

- Pharmaceutical packaging

- Industrial Applications

- Other

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

Sonoco ThermoSafe, Cold Chain Technologies, Peli BioThermal, CSafe Global, Envirotainer AB, va-Q-tec AG, Sofrigam Group, Intelsius, Inmark Global Holdings LLC, Cryopak Industries Inc., Sealed Air Corporation, SEE, Smurfit Westrock, DS Smith Plc, Softbox Systems, TemperPack Technologies Inc., Ranpak Holdings Corp., Nordic Cold Chain Solutions, Insulated Products Corporation, EcoCool GmbH, Emball’iso SA

Recent Industry Developments

April 2026 - Envirotainer and Jeena & Company signed an MoU to strengthen pharmaceutical cold chain logistics, improving access to compliant temperature-controlled air-cargo solutions for pharma shippers. The partnership supports rising demand for reliable cold chain packaging and container access across global pharma routes.

March 2026 - Cold Chain Technologies announced the launch of MedAssure at LogiPharma 2026, positioning it as a cold chain orchestration platform for life sciences logistics. The platform supports proactive shipment visibility, risk reduction, data-driven decision-making, and improved coordination across temperature-sensitive supply chains.

March 2026 - Peli BioThermal entered a strategic partnership with Polar Group to expand reusable and single-use cold chain solutions across Brazil. The move strengthens regional access to temperature-controlled packaging for pharmaceutical and life sciences shipments in South America.

February 2026 - va-Q-tec highlighted its vacuum-insulated Thermo Trolley, designed to secure the cold chain without refrigerated vehicles, dry ice, or cold packs. The solution reflects growing demand for passive, energy-efficient cold chain packaging and transport systems.

January 2026 - Envirotainer appointed Aymeric Chandavoine as Chief Executive Officer, effective May 2026. The leadership move is significant for the temperature-controlled pharmaceutical container segment as the company continues expanding its global cold chain logistics and packaging capabilities.

December 2025 - Cold Chain Technologies launched EcoFlex 3, an upgraded reusable insulated shipper for temperature-controlled logistics. The product strengthens the company’s reusable packaging portfolio and supports pharmaceutical and biologics shipments requiring consistent thermal protection and improved handling efficiency.

November 2025 - Sonoco completed the sale of its ThermoSafe business unit to Arsenal Capital Partners. The transaction positioned ThermoSafe as a standalone temperature-assurance business focused on scaling cold chain packaging and logistics solutions for healthcare and life sciences customers.

October 2025 - CSafe launched Silverskin RE, a reusable thermal cover designed as an alternative to single-use thermal covers. The launch supports pharmaceutical companies seeking lower-waste cold chain protection while maintaining temperature-control reliability during transportation.

September 2025 - IAG Cargo approved SkyCell’s temperature-controlled 1500X series containers for use across its network. The approval expanded temperature-controlled shipping options for pharmaceutical customers and strengthened access to reusable, sustainable cold chain packaging for biologics and vaccines.

May 2025 - Cold Chain Technologies expanded its curbside recyclable parcel shipper portfolio with the TRUEtemp Naturals shipper. The launch addressed demand for sustainable single-use cold chain packaging that combines thermal performance, operational efficiency, and easier disposal for temperature-sensitive shipments.

FAQ's

The Global Cold Chain Packaging Market is estimated to generate USD 40 billion in revenue in 2026.

The Global Cold Chain Packaging Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% during the forecast period from 2026 to 2032.

The Cold Chain Packaging Market is estimated to reach USD 91.6 billion by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!