"The Connected Mining Market was valued at $13.4 billion in 2024 and is projected to reach $44.0 billion by 2034, growing at a CAGR of 12.36%."

The Connected Mining market is undergoing a transformative shift as mining operations increasingly embrace interconnected technologies to optimize productivity, enhance safety, and promote sustainability. Connected mining leverages the Internet of Things (IoT), automation, and data analytics to create a more intelligent and efficient mining ecosystem. By connecting equipment, vehicles, and infrastructure through a network of sensors and communication systems, mining companies gain unprecedented visibility into their operations. This allows them to make data-driven decisions that improve resource allocation, reduce operational costs, and significantly enhance worker safety in inherently hazardous environments. In 2024, the industry witnessed a growing adoption of autonomous haulage systems (AHS), where driverless trucks and other automated vehicles became more prevalent in mine sites, improving productivity and worker safety. Advancements in remote monitoring and control technologies enabled operators to manage operations from centralized control rooms, further streamlining processes and optimizing resource utilization.

The Connected Mining market is projected to experience accelerated growth in 2025, propelled by a variety of factors. The increasing need to enhance worker safety and minimize risks within mining operations is a crucial driver, pushing mining companies to embrace technologies that can mitigate hazards and improve overall safety. Furthermore, the growing pressure to improve operational efficiency and optimize resource utilization is compelling mining companies to adopt connected solutions that can reduce costs, minimize waste, and maximize resource extraction. The development of advanced analytics and artificial intelligence (AI) capabilities is creating new opportunities to extract valuable insights from operational data, leading to more informed decision-making, predictive maintenance, and optimized resource allocation. The anticipated growth in 2025 emphasizes the industry's commitment to leveraging technology to create safer, more efficient, and more sustainable mining operations.

The Global Connected Mining Market Analysis Report will provide a comprehensive assessment of business dynamics, offering detailed insights into how companies can navigate the evolving landscape to maximize their market potential through 2034. This analysis will be crucial for stakeholders aiming to align with the latest industry trends and capitalize on emerging market opportunities.

Key Insights

- Connected mining initiatives initially focused on fleet management and dispatch systems for trucks and shovels, but have expanded to include drilling, blasting, loading, crushing, conveying and back-office processes, reflecting a long-term shift toward end-to-end digital integration across the mining value chain.

- Surface and underground communications are the backbone of connected mining, with mines deploying robust Wi-Fi meshes, private LTE and increasingly 5G-ready networks to support video, telemetry and control traffic for mobile equipment, sensors and personnel in challenging, dynamic environments.

- Safety use cases remain a strong driver, including proximity detection, collision avoidance, geofencing, fatigue monitoring and real-time location of workers and assets. By combining sensors, analytics and alerts, connected systems help reduce incidents and support compliance with stringent occupational safety standards.

- Asset performance and predictive maintenance are key growth applications, where sensors on haul trucks, drills, crushers and conveyors feed data into analytics platforms that detect anomalies early, reduce unplanned downtime and extend component life, directly impacting operating costs and production reliability.

- Automation and autonomy are gaining traction, especially in large open-pit operations where autonomous haul trucks, remote-controlled drills and robotic inspections rely on low-latency connectivity and centralized control. Connected mining platforms provide the data and command layer needed to coordinate mixed fleets of automated and conventional equipment.

- Environmental monitoring and ESG reporting are emerging as important connected mining segments, with networked instruments tracking air quality, dust, noise, water usage and tailings dam conditions, enabling more transparent reporting to regulators, investors and communities while supporting early risk detection.

- Integrated operations centers and remote-control rooms are becoming the nerve centers of connected mines, consolidating data, video and controls from dispersed sites into centralized hubs where multidisciplinary teams can coordinate planning, execution and maintenance in near real time.

- The competitive landscape is increasingly collaborative, with mining companies, OEMs and technology providers co-developing open, interoperable platforms rather than closed proprietary systems. This enables easier integration of new applications and reduces vendor lock-in as digital roadmaps evolve.

- Cybersecurity and data governance are rising priorities as more mission-critical functions are connected and controlled over digital networks. Mining firms are investing in secure architectures, network segmentation and continuous monitoring to protect operations from cyber threats and to safeguard sensitive operational data.

- Looking ahead, the connected mining market is expected to deepen its use of AI, digital twins and edge analytics, enabling simulation-driven planning, real-time optimization and more autonomous decision-making. Operators that align technology investments with workforce skills, change management and clear business cases are best positioned to capture long-term value from connectivity at scale.

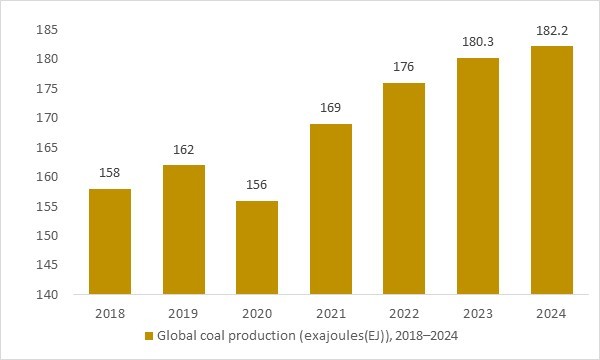

Global coal production (exajoules(EJ)), 2018–2024

Figure:Global coal production (exajoules), 2018–2024 – illustrating how persistent, near-record coal output from large open-pit and underground mines continues to push operators toward connected mining platforms, including private LTE/5G networks, IoT-based safety systems and autonomous equipment

- Global coal production has remained at near-record levels between 2018 and 2024, underscoring the scale and intensity of mining operations worldwide. Large open-pit and underground coal mines are under constant pressure to improve safety, productivity and cost efficiency, which is accelerating investment in connected mining solutions. Private LTE/5G networks, IoT-based gas and dust monitoring, real-time fleet management and autonomous equipment are increasingly deployed across these sites. As a result, sustained coal output is a key macro driver supporting long-term growth in the connected mining market.

Regional Insights

North America Connected Mining Market Analysis

The North America Connected Mining market experienced notable advancements in 2024, driven by the rapid adoption of cutting-edge technologies, increasing demand for sustainable and energy-efficient solutions, and robust investments in industrial modernization. The shift towards automation and digital transformation across manufacturing and logistics sectors is anticipated to drive significant growth from 2025 onwards, supported by stringent environmental regulations and government incentives promoting cleaner technologies. The competitive landscape remains dynamic, with key players focusing on R&D, product innovation, and strategic collaborations to gain a competitive edge. Moreover, the integration of smart technologies, such as IoT and AI, in industrial operations continues to reshape market dynamics, presenting lucrative opportunities for companies aiming to optimize productivity and sustainability.

Europe Connected Mining Market Outlook

In 2024, the Europe Connected Mining market witnessed substantial growth fueled by the region's emphasis on renewable energy adoption, circular economy practices, and green manufacturing initiatives. With a strong policy framework supporting carbon neutrality goals and increasing investments in advanced production technologies, the market is poised for accelerated growth from 2025 onwards. Leading players are prioritizing sustainable product development and regional expansion to meet evolving consumer and industrial demands. Furthermore, the integration of automation in manufacturing and logistics, coupled with advancements in material engineering, is expected to drive innovation and bolster market competitiveness across the region.

Asia-Pacific Connected Mining Market Forecast

The Asia-Pacific Connected Mining market demonstrated robust progress in 2024, underpinned by rapid industrialization, infrastructural development, and rising adoption of advanced manufacturing solutions across key economies like China, India, and Japan. Anticipated growth from 2025 will be supported by increasing foreign investments, a burgeoning middle class, and government initiatives to boost domestic manufacturing capabilities. The region's competitive landscape is characterized by the presence of both global and regional players focusing on cost-effective innovations and strategic partnerships to expand their footprint. Key drivers include the rising demand for energy-efficient systems, advancements in material science, and the growing emphasis on digitalization in industrial operations.

Middle East, Africa, Latin America Connected Mining Market Overview

The Middle East, Africa, Latin America Connected Mining market displayed steady growth in 2024, primarily driven by infrastructural development and industrial modernization in emerging economies across Latin America, the Middle East, and Africa. From 2025 onwards, growth is anticipated to gain momentum, propelled by rising investments in sustainable industrial solutions and the increasing adoption of automation to enhance operational efficiency. The competitive landscape is evolving, with regional players leveraging partnerships and technological advancements to cater to local demands. Key factors supporting market expansion include government initiatives aimed at industrial diversification, the rising focus on energy-efficient systems, and advancements in supply chain technologies.

Connected Mining Market Research Scope

| Parameter | Connected Mining Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Connected Mining market sales data at the global, regional, and key country levels with a detailed outlook to 2034 allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Connected Mining market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Connected Mining market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Connected Mining business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Connected Mining Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below –

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Connected Mining Pricing and Margins Across the Supply Chain, Connected Mining Price Analysis / International Trade Data / Import-Export Analysis,

Supply Chain Analysis, Supply – Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Connected Mining market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days

Connected Mining Market Segmentation

By Solution Type

-

Asset Tracking & Fleet Management

-

Remote Monitoring & Control Systems

-

Predictive Maintenance & Asset Performance Management

-

Safety & Security Solutions (Personnel Tracking, Collision Avoidance, Proximity Detection)

-

Production Monitoring & Optimization

-

Environmental Monitoring & Compliance

-

Integrated Operations & Control Center Solutions

-

Other Connected Mining Solutions

By Component

-

Hardware (Sensors, RFID Tags, Wearables, Cameras, Drones, Edge Devices, Networking Equipment)

-

Software (IoT Platforms, Analytics, Digital Twin, SCADA, MES, Fleet Software)

-

Services (Consulting, System Integration, Managed Services, Support & Maintenance, Training)

By Mining Type

-

Surface Mining

-

Underground Mining

By Application / Process

-

Drilling & Blasting

-

Load, Haul & Dump (LHD) Operations

-

Crushing, Conveying & Material Handling

-

Mine Planning & Scheduling

-

Safety & Workforce Management

-

Maintenance & Repair Operations

-

Exploration & Surveying

-

Port, Rail & Logistics Operations

By Connectivity / Network Technology

-

Wi-Fi / Mesh Networks

-

Private LTE / 4G Networks

-

Private 5G Networks

-

LPWAN (LoRaWAN, NB-IoT and Others)

-

Satellite Communication

-

Wired Networks (Fiber, Ethernet and Others)

By Deployment Model

-

On-Premise

-

Cloud-Based

-

Hybrid

By End User

-

Large-Scale Mining Companies

-

Medium & Small Mining Operators

-

Mining Contractors & Service Providers

By Geography

-

North America (USA, Canada, Mexico)

-

Europe (Germany, UK, France, Spain, Russia, Rest of Europe)

-

Asia-Pacific (China, India, Australia, Indonesia, Japan, Rest of APAC)

-

The Middle East and Africa (GCC Countries, South Africa, Rest of MEA)

-

South and Central America (Brazil, Chile, Peru, Rest of SCA)"

Key Companies

-

ABB Ltd.

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Hitachi Construction Machinery Co., Ltd.

-

Sandvik AB

-

Epiroc AB

-

Hexagon AB (Mining Division)

-

Cisco Systems, Inc.

-

Schneider Electric SE

-

Siemens AG

-

SAP SE

-

Rockwell Automation, Inc.

-

Trimble Inc.

-

Symboticware Inc.

FAQ's

The Global Connected Mining Market is estimated to generate USD 14.9 billion in revenue in 2025

The Global Connected Mining Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 12.36% during the forecast period from 2025 to 2034.

The Connected Mining Market is estimated to reach USD 44.0 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!