"The Coriolus Versicolor Extract Market was valued at $ 576.1 million in 2025 and is projected to reach $ 888.5 million by 2034, growing at a CAGR of 5.56%."

The Coriolus Versicolor Extract Market is gaining strong momentum, propelled by rising consumer demand for immune-supportive natural supplements and expanding applications across pharmaceutical, nutraceutical, and functional food industries. Coriolus versicolor, also known as Turkey Tail mushroom, is renowned for its rich content of polysaccharopeptides (PSP and PSK), which exhibit immunomodulatory and potential anti-tumor properties. With growing interest in integrative and alternative medicine, this extract is being widely promoted for cancer adjuvant therapy, chronic fatigue syndrome, and immune enhancement. The market has seen increasing adoption in both developed and emerging economies, driven by shifting consumer preferences toward plant-based health solutions and supportive scientific studies demonstrating bioactive efficacy. As a result, manufacturers and suppliers are scaling production, ensuring organic sourcing, and enhancing extract purity to meet evolving regulatory and consumer expectations.

The market landscape is also influenced by increasing investments in research and clinical validation, enabling product standardization and broader acceptance among health practitioners and end-users. In North America and Europe, rising popularity of functional mushroom supplements is fueling demand for Coriolus versicolor extract in capsule, powder, and liquid formulations. Asia Pacific—particularly China and Japan—continues to dominate supply due to the ingredient’s long-standing use in traditional medicine and established cultivation infrastructure. The extract’s versatility in blending with other botanicals has opened up new opportunities in personalized wellness formulations. However, regulatory compliance, supply chain integrity, and the need for high bioavailability remain key challenges. Companies are responding with innovations in extraction technology, sustainable harvesting methods, and clinical-backed branding to differentiate their offerings. As awareness grows and integrative health trends accelerate, the Coriolus Versicolor Extract Market is expected to register stable growth, appealing to both preventive health consumers and therapeutic supplement users.

Key Market Insights

-

Growing interest in immune health and cancer support therapies is driving demand for Coriolus versicolor extract across global nutraceutical and integrative medicine sectors. Consumers are increasingly turning to natural remedies backed by traditional use and emerging scientific studies.

-

The extract’s active components—PSP and PSK—are under research for their immunomodulatory and anti-tumor properties, with supportive roles noted in chemotherapy recovery and chronic disease management. This is boosting its use in complementary and alternative medicine.

-

Asia Pacific, especially China and Japan, leads both production and consumption due to a long history of traditional medicinal use, well-established mushroom farming practices, and favorable government backing for natural therapeutics.

-

North America and Europe are experiencing fast-growing adoption driven by consumer preference for clean-label, plant-based supplements and heightened awareness of functional mushroom benefits through retail and e-commerce platforms.

-

Product innovation is expanding beyond supplements into functional foods, teas, and wellness beverages, enabling manufacturers to tap into younger, health-conscious demographics that prefer natural immune boosters in convenient forms.

-

Regulatory scrutiny is intensifying in many regions, prompting companies to improve standardization, transparency in sourcing, and bioactive concentration in their extracts. Certifications such as organic, non-GMO, and GMP are becoming market differentiators.

-

Clinical research partnerships are rising as companies seek scientific validation to build trust with both consumers and healthcare professionals. This is leading to more targeted products for immune health, fatigue reduction, and inflammation control.

-

The mushroom’s extract is also being incorporated into pet wellness products, particularly in immune supplements for dogs, signaling a niche growth area within the broader veterinary supplement market.

-

Sustainability is emerging as a key theme, with brands emphasizing wild harvesting, traceability, and environmentally responsible cultivation to appeal to eco-conscious consumers.

-

Market entry barriers remain moderate, with opportunities for small and mid-sized players to offer branded formulations, proprietary blends, and customized delivery systems for wellness-focused consumers globally.

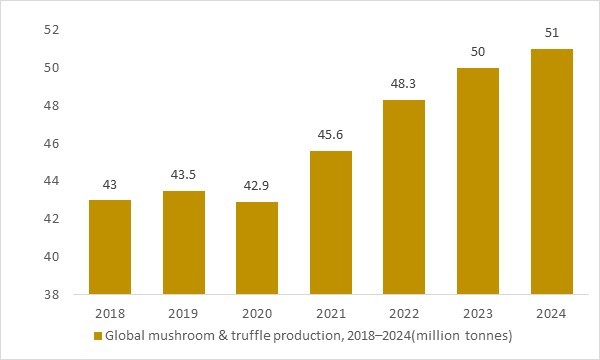

Global mushroom & truffle production, 2020–2024(million tonnes)

Figure: Global mushroom and truffle production increased from around the low-40 million tonne range in 2018–2020 to approximately 50 million tonnes in 2023 and is estimated to exceed this level in 2024e, providing a rapidly expanding fungal biomass base. As commercial mushroom cultivation scales in Asia and other regions, the availability of raw material for medicinal species, including Coriolus versicolor, improves significantly. OG Analysis estimates, derived from FAO mushroom statistics and recent academic studies, illustrate how rising global mushroom output underpins the long-term growth potential of Coriolus versicolor extracts used in immune-support supplements and functional health products.

The global mushroom and truffle production has grown significantly, from around 43 million tonnes in 2018–2019 to roughly 50 million tonnes in 2023, providing a large and expanding fungal biomass base for medicinal mushrooms including Coriolus versicolor. This increasing output supports growing availability of raw material for PSK/PSP extraction, fuelling rising global demand for immune-support, wellness, and nutraceutical products built on turkey-tail extracts. Continued growth in mushroom cultivation capacity — especially in major producers — underpins scalability and supply security for extract manufacturers. As consumers place greater emphasis on natural, functional, and plant-based health solutions, the expanding global mushroom harvest strengthens the long-term foundation of the Coriolus versicolor extract market.

North America Coriolus Versicolor Extract Market Analysis

The Coriolus Versicolor Extract Market in North America is experiencing robust growth, fueled by increasing consumer preference for natural immune-boosting supplements and functional health products. The region’s expanding wellness culture and high awareness of integrative oncology are encouraging the use of mushroom extracts like Coriolus versicolor in daily regimens. Health retailers and e-commerce platforms are boosting product visibility, while demand from naturopathic practitioners supports clinical acceptance. Companies are capitalizing on trends such as clean-label, vegan, and non-GMO certifications to differentiate their offerings. The U.S. leads regional growth, with rising innovation in capsule, powder, and blend formats tailored to personalized wellness.

Asia Pacific Coriolus Versicolor Extract Market Analysis

Asia Pacific remains the dominant region in the Coriolus Versicolor Extract Market due to its traditional use in Chinese and Japanese medicine and an established infrastructure for mushroom cultivation and extraction. The ingredient’s historical association with immune modulation and cancer adjunct therapy drives consistent demand in herbal pharmacies and health food sectors. Regulatory frameworks in countries like China support the inclusion of such extracts in formal medicinal systems, offering companies long-term growth stability. Opportunities are rising in South Korea, India, and Southeast Asia as the functional mushroom trend gains ground in urban health-conscious populations. Regional players are expanding into international markets with export-quality formulations.

China dominates the Coriolus Versicolor Extract Market, supported by its long-standing use of the mushroom in traditional Chinese medicine, extensive cultivation infrastructure, and strong domestic demand for immune-enhancing natural remedies across both therapeutic and preventive healthcare applications.

Europe Coriolus Versicolor Extract Market Analysis

In Europe, the market is expanding steadily as consumers shift toward natural and botanical-based wellness products. Germany, the UK, and France are key hubs where holistic and integrative health practices are mainstreaming mushroom extracts. EU regulatory emphasis on product quality and safety has driven innovation in extraction methods and bioactive standardization. The market also benefits from growing interest in adaptogenic supplements and immune support formulations, particularly in light of post-pandemic health awareness. Companies are entering partnerships with research institutions to support clinical studies, aiming to legitimize product claims and increase acceptance among mainstream healthcare providers.

Report Scope

| Parameter | Coriolus Versicolor Extract Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Coriolus Versicolor Extract Market Segmentation

By Product

- Powder

- Liquid

- Capsule

By Application

- Nutraceuticals

- Pharmaceuticals

- Food & Beverage

By End User

- Health-conscious Consumers

- Healthcare Providers

- Food Manufacturers

By Technology

- Extraction Methods

- Fermentation Processes

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Companies in the Market

- Host Defense

- NutraCap Labs

- Real Mushrooms

- Nammex (North American Medicinal Mushroom Extracts)

- Hawlik Gesundheitsprodukte GmbH

- Mushroom Science

- Xi’an Sost Biotech Co., Ltd.

- Botanic Healthcare

- Hunan Nutramax Inc.

- Organic Herb Inc.

- Bio-Botanica, Inc.

- Naturalin Bio-Resources Co., Ltd.

- Fungi Perfecti LLC

- Shaanxi Jiahe Phytochem Co., Ltd.

- MycoNutri Ltd.

Recent Developments

July 2025 – A leading Chinese herbal ingredient manufacturer reported increased exports of Coriolus versicolor extract to European nutraceutical brands, driven by demand for immune-support ingredients with clinical backing.

June 2025 – An Indian phytochemical company commissioned a continuous-flow production line for Coriolus versicolor extract to improve purity consistency and meet regulatory standards for pharmaceutical applications.

June 2025 – Xi’an-based botanical extract companies launched a new line of PSP-enriched Coriolus versicolor powders targeting capsule and beverage formulations in the U.S. and European wellness markets.

May 2025 – A U.S.-based natural health company expanded its functional mushroom supplement line by introducing Coriolus versicolor extract products focused on immune modulation and gut health synergy.

What You Receive

• Global Coriolus Versicolor Extract market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Coriolus Versicolor Extract.

• Coriolus Versicolor Extract market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Coriolus Versicolor Extract market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Coriolus Versicolor Extract market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Coriolus Versicolor Extract market, Coriolus Versicolor Extract supply chain analysis.

• Coriolus Versicolor Extract trade analysis, Coriolus Versicolor Extract market price analysis, Coriolus Versicolor Extract Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Coriolus Versicolor Extract market news and developments.

The Coriolus Versicolor Extract Market international scenario is well established in the report with separate chapters on North America Coriolus Versicolor Extract Market, Europe Coriolus Versicolor Extract Market, Asia-Pacific Coriolus Versicolor Extract Market, Middle East and Africa Coriolus Versicolor Extract Market, and South and Central America Coriolus Versicolor Extract Markets. These sections further fragment the regional Coriolus Versicolor Extract market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Coriolus Versicolor Extract market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Coriolus Versicolor Extract market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Coriolus Versicolor Extract market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Coriolus Versicolor Extract business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Coriolus Versicolor Extract Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Coriolus Versicolor Extract Pricing and Margins Across the Supply Chain, Coriolus Versicolor Extract Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Coriolus Versicolor Extract market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

FAQ's

The Global Coriolus Versicolor Extract Market is estimated to generate USD 576.1 million in revenue in 2025.

The Global Coriolus Versicolor Extract Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.56% during the forecast period from 2025 to 2034.

The Coriolus Versicolor Extract Market is estimated to reach USD 888.5 million by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!