"The Global Counter-UAS (C-UAS) Technology Market was valued at $5.8 billion in 2025 and is projected to reach $14.4 billion by 2034, growing at a CAGR of 12.1%."

The Counter-Unmanned Aerial Systems (C-UAS) market is rapidly expanding as the global threat landscape evolves with the increasing proliferation of drones across commercial, defense, and insurgent operations. These systems are designed to detect, track, identify, and neutralize unauthorized or hostile drones through a variety of technologies such as radar, RF jamming, directed energy weapons, and kinetic interceptors. As drones become smaller, faster, and more autonomous, counter-drone systems are evolving in sophistication and modularity to address multi-domain threats. Governments, critical infrastructure operators, and event security providers are actively investing in C-UAS solutions to protect sensitive airspace and assets. The market is supported by rising geopolitical tensions, drone-enabled smuggling incidents, and increased security needs across borders, airports, and public venues. Technological innovation, regulatory support, and defense modernization programs are collectively pushing the C-UAS sector into mainstream security infrastructure.

The year 2024 saw significant momentum in the C-UAS space, driven by increased procurement from defense agencies and accelerated deployments at commercial airports and power plants. Notably, NATO members expanded joint counter-drone drills, leading to demand for interoperable and scalable C-UAS platforms. Startups introduced AI-enhanced detection algorithms capable of classifying drone swarms based on behavioral signatures, while larger players upgraded RF sensing systems with directional geolocation capabilities. Directed energy solutions, such as high-powered microwave and laser weapons, moved from testing to initial deployment, especially in Middle Eastern military programs. The market also saw strong M&A activity, with radar specialists, AI analytics providers, and software-defined radio companies joining forces to offer integrated detection-to-defeat chains. Regulatory bodies in the U.S. and EU advanced discussions to create standardized U-Space integration protocols, reinforcing commercial uptake of C-UAS systems. Overall, 2024 marked a transition from pilot deployments to broader field implementations with emphasis on mobility, multi-threat response, and software integration.

Looking ahead to 2025 and beyond, the C-UAS market is expected to mature into a key pillar of urban and national airspace security frameworks. Development is shifting toward AI-driven, autonomous response systems capable of real-time threat classification and precision engagement with minimal human oversight. As drone technology advances, next-generation C-UAS platforms will emphasize multi-layered defenses combining kinetic, electronic, and cyber effectors. Civilian and industrial markets will account for a larger share, with stadiums, ports, and VIP zones adopting lightweight, rapid-deployment C-UAS kits. International standards on drone traffic management and airspace defense coordination are anticipated to emerge, improving cross-border collaboration. Meanwhile, ongoing conflicts and gray-zone warfare will fuel defense spending on tactical and long-range C-UAS units. Innovations in quantum radar, directed energy miniaturization, and 5G-enabled sensor fusion are poised to transform the detection and interdiction landscape, ensuring the market’s strong growth through the next decade.

Key Market Trends, Drivers and Challenges

-

Escalating incidents of hostile and unauthorized drone activity around battlefields, borders, and critical infrastructure remain the single most important historic and current catalyst for C-UAS deployment, pushing governments and private operators to move from ad hoc trials to programmatic, multi-site rollouts of counter-drone architectures.

-

While defence and national security use cases still dominate spending, commercial and civil demand is expanding rapidly across airports, energy and utilities, industrial plants, logistics hubs, correctional facilities, and major event venues, creating new addressable segments and favouring scalable, configurable product portfolios over bespoke military-only solutions.

-

Multi-sensor detection with advanced analytics has become the key technical differentiator, as customers prioritise systems that can reliably detect, track, and classify small, low-observable drones in cluttered environments by fusing radar, radio-frequency, electro-optical, infrared, and acoustic inputs with artificial intelligence and machine learning algorithms.

-

Soft-kill mitigation techniques such as jamming, spoofing, and protocol takeover continue to anchor most deployments due to their flexibility and cost profile, but there is growing investment in hard-kill and directed-energy interceptors for high-value sites and contested theatres where drones are weaponised and lethality, swarming, or stand-off tactics demand decisive neutralisation.

-

Ground-based fixed and transportable C-UAS systems currently represent the backbone of the market, yet there is clear momentum towards mobile, vehicle-mounted, naval, and airborne platforms that can accompany manoeuvre forces, secure convoys, protect maritime assets, and plug gaps in wider air-defence networks with agile counter-drone coverage.

-

Open systems architecture, modular hardware, and software-defined functionality are becoming critical purchasing criteria, as customers seek future-proof platforms that can integrate with existing command-and-control, surveillance, and air-traffic systems, accept new sensors and effectors, and receive continuous software upgrades against evolving drone tactics and signatures.

-

Regulatory and legal constraints around electronic attack and kinetic engagement, especially in civilian airspace, shape solution design and go-to-market strategies, prompting strong demand for detection-only deployments, airspace awareness services, and carefully governed mitigation capabilities reserved for authorised defence and homeland security operators.

-

Regionally, markets with large defence budgets and active security threats are leading early adoption, while emerging economies accelerate local industry development, offset agreements, and co-production partnerships, reshaping the supplier landscape and creating opportunities for technology transfer, joint ventures, and locally assembled C-UAS product lines.

-

Business models are shifting beyond one-off hardware sales toward recurring revenue based on software licences, analytics subscriptions, managed airspace security services, and long-term support contracts, encouraging vendors to prioritise lifecycle performance, system availability, and continuous capability enhancement over purely initial procurement metrics.

-

Intense innovation from start-ups and dual-use technology firms, combined with strategic investments by established defence contractors, is driving rapid product refresh cycles, ecosystem partnerships, and selective mergers and acquisitions, consolidating capabilities across sensing, electronic warfare, command-and-control, and effectors into more comprehensive C-UAS solution stacks.

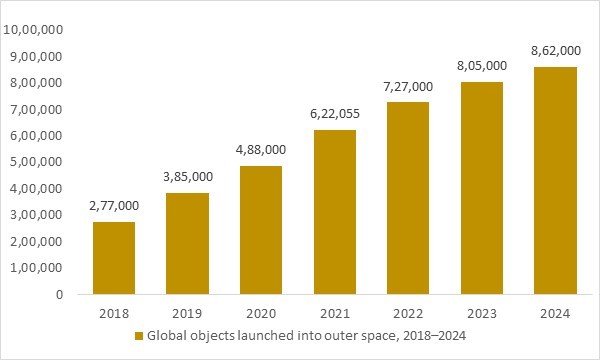

Global Commercial small UAS fleet, 2018–2024

Figure: Commercial small UAS fleet expanded from around 277,000 registered drones in 2018 to more than 860,000 units by 2024, reflecting rapid adoption of unmanned aircraft across inspection, logistics, agriculture and public-safety missions. As low-altitude drone activity intensifies around airports, borders, critical infrastructure and dense urban areas, airspace managers and security agencies face rising operational complexity and exposure to deliberate misuse. OG Analysis estimates, derived from global civil aviation and drone registration statistics, highlight how the steep growth in commercial small UAS deployments is a core structural demand driver for advanced Counter-UAS (C-UAS) detection, tracking and mitigation technologies.

commercial small UAS fleet expanded strongly registered drones, reflecting rapid adoption across inspection, logistics, agriculture and public-safety missions.

This sustained rise in low-altitude drone activity greatly increases the complexity of airspace management around airports, borders, critical infrastructure and dense urban corridors.

At the same time, the growing number of legitimate drones heightens the risk of misuse, including espionage, contraband delivery and potential kinetic or CBRN attacks.

As a result, the rapid build-up of the commercial small UAS fleet is a key structural driver for investment in advanced Counter-UAS technologies and radiation detection, monitoring and security solutions.

Report Scope

| Parameter | Counter-Unmanned Aerial Systems (C-UAS) market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Counter-UAS (C-UAS) Technology Market Segmentation

By Product

- Radars

- Lasers

- Electronic Warfare

By Application

- Military

- Homeland Security

- Commercial

By End User

- Government

- Private Sector

By Technology

- Detection

- Interception

- Neutralization

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Raytheon Technologies Corporation

- Lockheed Martin Corporation

- Leonardo S.p.A.

- Thales Group

- Northrop Grumman Corporation

- Dedrone Holdings Inc.

- DroneShield Ltd

- Elbit Systems Ltd.

- Saab AB

- Anduril Industries

- BAE Systems

- Rheinmetall AG

- Israel Aerospace Industries (IAI)

- Liteye Systems Inc.

- Black Sage Technologies

What You Receive

• Global Counter-UAS (C-UAS) Technology market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Counter-UAS (C-UAS) Technology.

• Counter-UAS (C-UAS) Technology market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Counter-UAS (C-UAS) Technology market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Counter-UAS (C-UAS) Technology market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Counter-UAS (C-UAS) Technology market, Counter-UAS (C-UAS) Technology supply chain analysis.

• Counter-UAS (C-UAS) Technology trade analysis, Counter-UAS (C-UAS) Technology market price analysis, Counter-UAS (C-UAS) Technology Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Counter-UAS (C-UAS) Technology market news and developments.

The Counter-UAS (C-UAS) Technology Market international scenario is well established in the report with separate chapters on North America Counter-UAS (C-UAS) Technology Market, Europe Counter-UAS (C-UAS) Technology Market, Asia-Pacific Counter-UAS (C-UAS) Technology Market, Middle East and Africa Counter-UAS (C-UAS) Technology Market, and South and Central America Counter-UAS (C-UAS) Technology Markets. These sections further fragment the regional Counter-UAS (C-UAS) Technology market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Counter-UAS (C-UAS) Technology market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Counter-UAS (C-UAS) Technology market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Counter-UAS (C-UAS) Technology market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Counter-UAS (C-UAS) Technology business prospects by region, key countries, and top companies' information to channel their investments.

FAQ's

The Global Counter-UAS (C-UAS) Technology Market is estimated to generate USD 5.8 billion in revenue in 2025.

The Global Counter-UAS (C-UAS) Technology Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 12.1% during the forecast period from 2025 to 2034.

The Counter-UAS (C-UAS) Technology Market is estimated to reach USD 14.4 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!