"Cranberries Market is valued at $2.9 billion in 2025. Further, the market is expected to grow at a CAGR of 4.2% to reach $4.3 billion by 2034."

The Cranberries Market is witnessing steady growth driven by rising global demand for functional and natural food ingredients with health benefits. Cranberries are widely used in the food and beverage industry for juices, concentrates, dried snacks, sauces, bakery products, and confectionery due to their tart flavour, rich colour, and antioxidant properties. Increasing consumer awareness of cranberries’ role in urinary tract health, cardiovascular health, and immunity boosting is expanding their adoption in functional foods and dietary supplements. Major producers, particularly in the US and Canada, are investing in expanding production capacities and enhancing processing technologies to cater to the rising domestic and international demand. Additionally, innovations in product formats such as sweetened dried cranberries, cranberry powders, and flavoured extracts are expanding application possibilities across sectors.

The market is characterised by strong exports, especially from North America to Europe and Asia Pacific, driven by the rising popularity of superfruits among health-conscious consumers. Companies are focusing on developing organic and sustainably sourced cranberry products to address growing environmental concerns and regulatory requirements. The foodservice and bakery sectors are increasingly incorporating cranberries into recipes to align with consumer preferences for natural and healthier ingredients. However, market challenges include yield fluctuations due to climatic conditions, high production costs, and regulatory complexities in export markets. Moving forward, the market is poised for expansion with trends favouring clean-label, functional, and organic products while companies prioritise strategic partnerships, brand differentiation, and product innovation to strengthen market positions globally.

By Product Type, the largest segment is Fresh Fruits. This is because fresh cranberries are widely used in the production of juices, sauces, and bakery products, and they are preferred by food processors for their natural taste, high nutrient retention, and versatility in applications across food and beverage sectors globally.

By Nature, the fastest-growing segment is Organic. The rising consumer demand for clean-label, chemical-free, and sustainably sourced products is driving rapid growth in organic cranberries, as consumers perceive them to be healthier and environmentally friendly, encouraging manufacturers to expand organic cultivation and certified product offerings.

Key Insights

- The cranberries market is growing steadily due to increasing demand for functional foods and beverages as consumers seek natural ingredients that offer antioxidant and anti-inflammatory benefits, promoting heart health, urinary tract health, and immunity enhancement globally.

- Cranberries are widely used in juices, concentrates, sweetened dried cranberries, sauces, bakery items, and confectionery, with manufacturers innovating formats such as infused cranberries, powders, and extracts to diversify product portfolios and applications across food and beverage segments.

- North America dominates global cranberry production with major cultivation in the United States and Canada, supported by favourable climatic conditions, established farming infrastructure, and significant investments by growers to enhance yields and processing capabilities.

- Europe and Asia Pacific are witnessing growing consumption driven by increasing awareness of cranberries as superfruits, rising incorporation in functional foods, and expanding distribution networks by North American producers targeting international markets.

- Key companies in the market are focusing on expanding production capacities, investing in sustainable farming practices, and adopting advanced processing technologies to ensure high-quality, preservative-free, and nutrient-retained cranberry products for global consumers.

- Rising trends of clean-label, organic, and non-GMO products are encouraging manufacturers to launch certified organic cranberries and develop transparent supply chains that appeal to environmentally and health-conscious consumers worldwide.

- The foodservice and bakery industries are increasingly using cranberries in salads, sauces, pastries, and desserts, aligning with consumer preferences for natural, nutrient-rich ingredients that enhance flavour and provide functional health benefits.

- Market challenges include price volatility due to climatic fluctuations affecting crop yields, high production and harvesting costs, and strict regulatory standards in export markets, impacting profitability for growers and processors globally.

- Companies are adopting strategic partnerships, branding initiatives, and marketing campaigns highlighting the health benefits of cranberries to drive consumer demand and strengthen their competitive positioning in domestic and export markets.

- Future market growth will be driven by innovations in flavoured extracts, infused cranberries, and dietary supplements, supported by rising consumer focus on preventive healthcare and functional nutrition trends across developed and emerging economies.

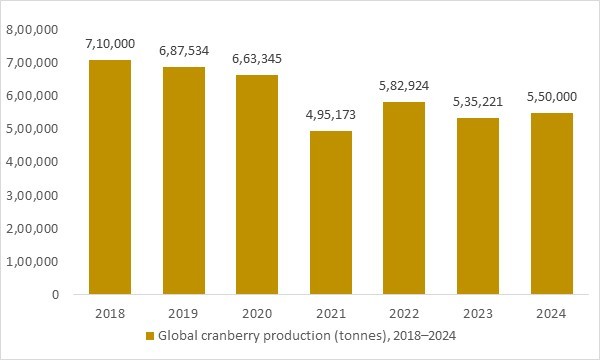

Global cranberry production (tonnes), 2018–2024

Figure: Global cranberry production between 2018 and 2024 shows a sizeable yet concentrated raw material base that underpins juice, concentrate, dried cranberry and nutraceutical demand while highlighting year-to-year volatility that influences supply stability, pricing and value chain competitiveness.Global cranberry production (tonnes), 2018–2024

- Global cranberry production fluctuated between roughly 0.5 and 0.7 million tonnes from 2018 to 2024, reflecting a sizeable yet geographically concentrated raw material base. As cranberries are increasingly processed into juice, concentrates, sweetened dried cranberries and nutraceutical ingredients, this production trend underpins long-term growth in the cranberries market. OG Analysis estimates, derived from international crop statistics and industry sources, highlight how supply volatility, yield swings and regional concentration can influence pricing, export flows and investment decisions across the cranberry value chain.

Regional Insights

North American Cranberries market

North America dominates the global cranberries market as the primary producer, with extensive cultivation concentrated in the U.S. (notably Wisconsin, Massachusetts) and Canada (mainly Quebec and British Columbia). Processed cranberries form the core of industrial demand, powering strong sales in juices, sauces, sweetened dried cranberries, nutraceuticals, and bakery ingredients. Seasonal consumption spikes during holiday periods are being complemented by year-round demand fueled by the fruit’s recognized health and antioxidant benefits. Cooperative structures and advanced bog management ensure high production efficiency, although growers continue to face challenges from climate variability and pricing pressure. Ongoing product innovation and marketing around immunity and urinary tract health further position the region as a leader in premium and functional cranberry products.

Europe Cranberries market

Europe is a demand-driven market with a high dependency on imports to meet its cranberry consumption needs, especially for industrial processing. Dried cranberries remain the fastest-growing form due to rising use in breakfast cereals, snacks, confectionery, and bakery products. Health and wellness positioning supports strong traction for clean-label, organic, and reduced-sugar offerings. Retailers and manufacturers are actively promoting cranberries in superfruit-themed product lines, broadening consumer exposure beyond seasonal windows. Trade dynamics continue to influence procurement strategies, while diversified food formats such as flavored, chopped, and infused cranberries enhance product differentiation across European markets.

Asia-Pacific Cranberries market

Asia-Pacific represents the most dynamic growth opportunity for the cranberries market, driven by rising incomes, Western-style diets, and increasing interest in functional foods. China, Japan, South Korea, India, and Southeast Asian nations show rapid adoption of dried cranberries in bakery goods, snacks, and beverages. Imports dominate supply, with expanding cold-chain logistics and online grocery channels boosting market accessibility. Cranberry juices and concentrates are gaining relevance in health-focused consumption trends, while supplements and extracts are building presence in nutraceutical categories. With limited domestic production, promotional efforts by global suppliers continue to accelerate demand and boost market penetration.

Reort Scope

| Parameter | Cranberries Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Product Type

- Fresh Fruits

- Freeze Dried

- Air Dried

- Other Product Types

By Nature

- Conventional

- Organic

By End-User

- Bakery

- Confectionaries

- Dairy Products

- Beverages

- Cereals

- Other End Users

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Del Monte Foods Inc.

- Ocean Spray Cranberries Inc.

- Mariani Packing Co. Inc.

- Sun-Maid Growers of California

- Traina Foods Inc.

- Meduri Farms Inc.

- Decas Cranberry Products Inc.

- Eden Foods

- Citadelle Camp Coop

- Fruit d'Or Inc.

- Sisters Fruit Company

- Royal Nut Company

- Graceland Fruit Inc.

- Rostaa Superfoods

- Stoneridge Orchards

- Sundance Vitamins LLC

- Fresh Meadows Cranberries

- Honestly Cranberry

- Michigan Cranberry Co.

- Muskoka Lakes Farm and Winery

- New England Cranberry

- Cape Blanco Cranberries Inc.

- Habelman Bros. Co.

- Sun Organic Industries Pvt. Ltd.

- Mitthi Foods

Recent Industry Developments

-

Sep 2025 – Ocean Spray Ingredients: Showcased expanded cranberry-ingredient solutions for bakery and snack applications at a major industry event, highlighting broader use of dried cranberries, blends, and ingredient formats beyond traditional retail products.

-

Jun 2025 – Ocean Spray: Launched new Craisins flavor variants (including sour and “swicy” profiles) and refreshed select packaging, aiming to drive higher snacking occasions and modernize the brand’s dried-cranberry portfolio.

-

Feb 2025 – Fruit d’Or: Announced the acquisition of Decas Cranberry Products (U.S.), expanding Fruit d’Or’s North American footprint and strengthening its supply base and processing scale for cranberry ingredients and dried formats.

-

Dec 2024 – Ocean Spray: Partnered to launch on-the-go powdered drink mixes made with real cranberry juice powder, extending cranberry consumption into convenient single-serve beverage formats with broad retail rollout plans.

-

Oct 2024 – Fruit d’Or: Introduced a new organic wild blueberry + cranberry powder blend positioned for clean-label, antioxidant-focused food, beverage, and supplement applications, expanding value-added cranberry ingredient offerings.

-

Jun 2024 – Ocean Spray & Brightseed: Expanded their partnership to use AI-led discovery and validation of cranberry bioactives, strengthening science-backed positioning for cranberry-derived ingredients and functional nutrition applications.

What You Receive

• Global Cranberries market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Cranberries.

• Cranberries market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Cranberries market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Cranberries market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Cranberries market, Cranberries supply chain analysis.

• Cranberries trade analysis, Cranberries market price analysis, Cranberries Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Cranberries market news and developments.

The Cranberries Market international scenario is well established in the report with separate chapters on North America Cranberries Market, Europe Cranberries Market, Asia-Pacific Cranberries Market, Middle East and Africa Cranberries Market, and South and Central America Cranberries Markets. These sections further fragment the regional Cranberries market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Cranberries market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Cranberries market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Cranberries market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Cranberries business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Cranberries Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Cranberries Pricing and Margins Across the Supply Chain, Cranberries Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Cranberries market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

FAQ's

The Global Cranberries Market is estimated to generate USD 2.9 billion in revenue in 2025.

The Global Cranberries Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.2% during the forecast period from 2025 to 2034.

The Cranberries Market is estimated to reach USD 4.3 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!