"The Doming Resin Market was valued at $1.5 billion in 2025 and is projected to reach $2.9 billion by 2034, growing at a CAGR of 8.1%."

The Doming Resin Market serves a niche but steadily expanding segment within the adhesives and coatings industry, driven by its use in product labeling, promotional materials, and protective coatings for graphics and badges. Doming resins, typically composed of two-part polyurethane or epoxy systems, create a raised, glossy, and durable surface on printed materials, enhancing both aesthetics and durability. These resins are valued for their clarity, UV stability, non-yellowing characteristics, and resistance to abrasion. The market is being supported by the increasing demand for product differentiation in branding and labeling, especially in consumer electronics, automotive accessories, promotional items, and retail merchandise. Moreover, customization in small batches, enabled by digital printing and on-demand doming applications, is boosting adoption among SMEs and designers worldwide.

In 2024, the Doming Resin Market experienced steady innovation focused on sustainability and operational ease. Leading manufacturers introduced bio-based and low-VOC resin variants to align with environmental regulations and green branding trends. There was a visible rise in demand from emerging economies, particularly in Southeast Asia and Latin America, where SME-led promotional industries are flourishing. Automation in doming processes has become a focal point, with companies launching dispensing systems and robotic applicators that ensure uniform resin flow and bubble-free finishes. Additionally, UV-curable doming resins gained traction due to their faster curing times and improved temperature resistance. Industry collaborations with label and badge manufacturers were also prominent as vendors sought to offer integrated end-to-end branding solutions, combining printing, coating, and finishing systems.

Looking forward to 2025 and beyond, the Doming Resin Market is expected to witness deeper penetration into luxury and lifestyle sectors such as cosmetics, jewelry, fashion accessories, and high-end packaging. Eco-friendly innovations will become increasingly standard, with more suppliers launching solvent-free and biodegradable options. Digital automation will play a larger role in streamlining workflows, especially for custom applications requiring precision and repeatability. Additionally, advances in nanotechnology may introduce self-healing or anti-microbial doming surfaces. Strategic investments from chemical companies into R&D and partnerships with graphic design software firms are also anticipated to enhance the integration between creative design and application technologies. As customer expectations for visual appeal and durability rise, doming resins will continue evolving toward smarter, greener, and more versatile solutions.

Trade Intelligence Of Doming Resin Market

| Global Epoxide resins, in primary forms Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 5,874.6 | 8,753.4 | 8,710.2 | 6,673.1 | 6,467.7 |

| China | 1,254.5 | 1,460.4 | 1,122.8 | 682.2 | 654.4 |

| United States of America | 352.0 | 693.7 | 983.2 | 594.4 | 582.8 |

| Germany | 495.3 | 701.4 | 691.4 | 558.6 | 491.9 |

| Korea, Republic of | 144.8 | 201.7 | 200.2 | 183.0 | 288.2 |

| Mexico | 166.3 | 217.9 | 267.8 | 254.4 | 275.1 |

|

| |||||

| Source: OGAnalysis | |||||

- China, United States of America, Germany, Korea, Republic of and Mexico are the top five countries importing 35.4% of global Epoxide resins, in primary forms in 2024

- China accounts for 10.1% of global Epoxide resins, in primary forms trade in 2024

- United States of America accounts for 9% of global Epoxide resins, in primary forms trade in 2024

- Germany accounts for 7.6% of global Epoxide resins, in primary forms trade in 2024

| Global Epoxide resins, in primary forms Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

Key Insights

-

Doming resins emerged from traditional casting and coating technologies, but their use in labels and nameplates has elevated them into a distinct specialty segment focused on optical performance and durability. The historical association with premium badges and emblems continues to drive their positioning as value-adding finishes even in cost-sensitive markets.

-

Polyurethane doming systems dominate many applications due to their superior UV resistance, flexibility, and long-term clarity, especially for outdoor and automotive uses. Epoxy systems remain relevant in indoor, budget-conscious, or high-adhesion environments, and are increasingly being modified to reduce yellowing and improve mechanical properties.

-

Domed graphics are heavily used in branding for appliances, tools, consumer electronics, and automotive accessories, where the three-dimensional lens effect enhances legibility and creates a tactile, high-quality impression. This makes doming an effective way to uplift perceived value without major changes to the underlying product.

-

The rise of digital printing has significantly broadened the addressable base for doming resins, enabling short runs, personalized designs, and rapid prototyping. Print service providers and converters can now offer domed finishes on demand, integrating doming into existing workflows with automated dispensers and compact curing units.

-

Environmental and worker-safety considerations are prompting a gradual shift toward low-VOC, low-odor and reduced-hazard formulations, along with better ventilation and handling practices. Suppliers that can balance ease of use, lower hazard profiles, and robust performance are increasingly favored by converters and brand owners.

-

Processability factors such as controlled viscosity, long but predictable pot life, bubble-free curing, and good self-levelling behavior are critical selection criteria for doming resins. Stable mixing ratios and forgiving application windows reduce waste and rework, which is crucial for converters operating high-SKU, short-run businesses.

-

Outdoor and automotive applications require resins with strong resistance to ultraviolet exposure, temperature cycling, moisture, fuels, and detergents. Continuous improvements in light stabilizers and aliphatic resin backbones are extending service life in these demanding environments, supporting wider adoption in vehicle branding and exterior signage.

-

Automation is becoming more common in medium and large converters, with robotic or CNC-guided doming lines delivering precise dosing, consistent lens height, and repeatable quality. This trend favours resins that are compatible with automated metering and mixing systems and can maintain consistent performance over extended production runs.

-

The market is seeing increased use of doming in promotional items, e-commerce packaging, and customized products, where visually striking, durable logos help brands stand out. This aligns doming resins with broader trends in personalization, limited editions, and experiential marketing.

-

Looking ahead, doming resin demand is expected to track growth in industrial labelling, branded hardware, and digitally printed graphics, while being shaped by regulatory, sustainability, and design trends. Suppliers that combine robust chemistry, application know-how, and support for automation and safer operations are best positioned to capture future opportunities.

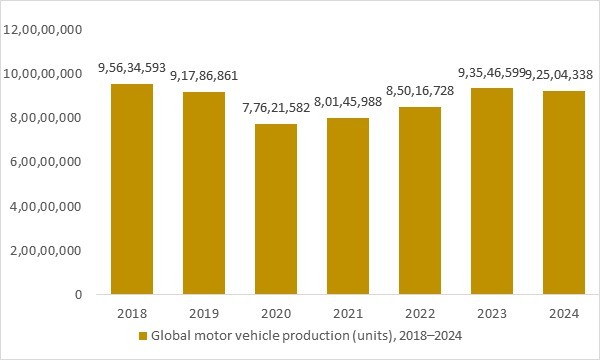

Global motor vehicle production (units), 2018–2024

Figure: Global motor vehicle production (units), 2018–2024. Rising vehicle output underpins demand for domed badges, emblems, and labels, supporting growth in the global doming resin market.

- Global motor vehicle production recovered from the 2020 downturn and remained above 92 million units in 2024. As automotive OEMs and aftermarket brands expand the use of durable, 3D domed labels, emblems, and nameplates, doming resin demand closely tracks vehicle output trends. This reinforces automotive as a key end-use segment in the Global Doming Resin Market.

Regional Insights

North America Doming resin market

In North America, the doming resin market is driven by strong demand from promotional products, automotive badging, electronics, and industrial labelling, where clear 3D coatings enhance both aesthetics and durability. Brand owners use epoxy and polyurethane doming systems on decals, nameplates, key fobs, control panels, and outdoor signage to improve scratch, UV, and chemical resistance while delivering a premium look. A dense base of printers, converters, and specialty label makers across the U.S. and Canada supports consistent offtake, with many shifting from older solvent-heavy systems toward low-VOC, low-yellowing, and faster-curing doming formulations. Innovation in UV-curable and fast-cycle systems is important for high-throughput shops supplying automotive, power tools, consumer electronics, and sports equipment. Sustainability expectations from major OEMs are also encouraging the development of more eco-friendly doming resins and improved waste-handling practices.

Europe Doming resin market

Europe’s doming resin market benefits from a sophisticated signage, automotive, and industrial graphics ecosystem, with high quality standards and strong design focus. Domed labels and badges are widely used in white goods, machinery, instruments, and premium consumer goods, where clarity, long-term UV stability, and weatherability are critical. European converters increasingly favour polyurethane and advanced epoxy systems with low yellowing, reduced free monomer content, and compliance with stringent chemical and worker-safety regulations. Suppliers in Germany, Italy, France, and the Nordics are active in tailoring formulations for automated dispensing, rapid curing, and compatibility with diverse substrates such as vinyl, polycarbonate, and metals. Growing attention to circularity and eco-design is pushing the region toward lower-VOC chemistries and more transparent supply chains, while the expansion of e-commerce packaging and branded logistics further supports demand for durable, high-impact domed branding.

Asia-Pacific Doming resin market

Asia-Pacific is the manufacturing and growth hub for doming resins, supported by a large base of electronics, automotive, motorcycle, and consumer-goods production. Reports highlight the region—particularly China, Taiwan, and South Korea—as a leading producer of doming resins and related materials, leveraging robust chemical infrastructure and a dense network of label and nameplate converters. Domed labels are widely used on appliances, IT equipment, scooters, e-bikes, and promotional items, as well as in solar and industrial electronics where durable protective coatings are essential. Local formulators supply a full range of epoxy, polyurethane, and UV-curable doming systems, often at competitive cost, while global players invest in regional plants and technical centres to support OEMs and export-oriented printers. As branding, customization, and aftermarket accessories grow across the region, demand for high-gloss, abrasion-resistant domed graphics is expected to rise further, especially in mid- to high-value product segments.

Report Scope

| Parameter | Doming Resin Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Diagnostic Method, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Doming Resin Market Segmentation

By Product

- Epoxy

- Polyurethane

- Acrylic

By Application

- Labels

- Crafts

- Automotive

- Electronics

By End User

- Manufacturing

- Retail

- Consumer Goods

By Technology

- UV Curing

- Heat Curing

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- DECO-TECH

- Polymer Chemie

- Siltech Corporation

- Heraeus Noblelight

- Intertronics

- Resinlab

- Electrolube

- EpoxySet

- Alchemie Ltd

- Permabond

- Decorative Resins

- CHEMIBOND

- Epoxies Etc.

- Master Bond Inc.

- Ellsworth Adhesives

Recent Industry Developments

-

Dec 2025 – COLOR-DEC: Showcased its latest doming solutions and PU-resin label finishing capabilities around major print/trade events, emphasizing automated dispensing systems for faster throughput and more consistent dome quality in industrial label production.

-

Feb 2025 – Liquid Lens & GJS Group Australia: Introduced the Roland DG BN2-20A printer/cutter into “domed resin” production bundles and starter-kit offerings, strengthening end-to-end workflows from printing to polyurethane resin doming for labels and decals.

-

Mar 2025 – COLOR-DEC: Announced demonstrations of its DOMES 4100GP automated doming system at industry exhibitions, highlighting higher-speed resin dispensing and production efficiency for 3D domed labels.

-

Jan 2025 – Liquid Lens: Increased technical outreach and training content for polyurethane doming resin application, reflecting rising customer focus on process control (temperature/humidity, viscosity/flow) to reduce rejects and improve optical clarity.

-

Nov 2024 – Liquid Lens: Launched a new e-commerce platform to expand global access to doming equipment, consumables, and resin cartridges, aiming to simplify ordering and accelerate adoption among small and mid-sized label producers.

-

Sep 2024 – Liquid Lens: Announced availability of the Roland VersaStudio BN2-20 print-and-cut solution within its doming ecosystem, targeting higher-quality output and faster production for businesses combining printed graphics with domed resin finishes.

What You Receive

• Global Doming Resin market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Doming Resin.

• Doming Resin market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Doming Resin market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Doming Resin market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Doming Resin market, Doming Resin supply chain analysis.

• Doming Resin trade analysis, Doming Resin market price analysis, Doming Resin Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Doming Resin market news and developments.

The Doming Resin Market international scenario is well established in the report with separate chapters on North America Doming Resin Market, Europe Doming Resin Market, Asia-Pacific Doming Resin Market, Middle East and Africa Doming Resin Market, and South and Central America Doming Resin Markets. These sections further fragment the regional Doming Resin market by type, application, end-user, and country.

FAQ's

The Global Doming Resin Market is estimated to generate USD 1.5 billion in revenue in 2025.

The Global Doming Resin Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 8.1% during the forecast period from 2025 to 2034.

The Doming Resin Market is estimated to reach USD 2.9 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!