"The Dried Peas Market was valued at $ 7.5 billion in 2026 and is projected to reach $ 13.98 billion by 2034, growing at a CAGR of 8.03%."

The Dried Peas Market is a significant segment of the pulses and plant-based protein industry, supported by rising demand from food processing, animal feed, plant-based foods, snacks, soups, flour milling, protein extraction, and household consumption. Dried peas, including green peas, yellow peas, split peas, and whole peas, are valued for their protein content, fiber, affordability, long shelf life, and versatility across traditional and modern food applications. They are widely used in soups, stews, curries, ready meals, pulse flours, extruded snacks, meat alternatives, bakery formulations, pet food, aquafeed, and livestock feed. Demand is being driven by growing consumer preference for plant-based nutrition, clean-label ingredients, sustainable protein sources, and cost-effective dietary staples. Food manufacturers increasingly use dried peas as a base ingredient for pea protein, pea starch, pea fiber, and functional flour, supporting innovation in vegan foods, protein beverages, meat substitutes, gluten-free products, and high-protein snacks.

The market is evolving with stronger focus on pulse processing, fractionation, traceable sourcing, improved seed varieties, organic dried peas, and value-added pea ingredients. Key trends include rising use of yellow peas in protein extraction, expansion of plant-based meat and dairy alternatives, growing demand for pulse-based snacks, and increased adoption of peas in pet nutrition and animal feed. Growth is supported by food security priorities, affordability compared with animal proteins, expansion of vegetarian and flexitarian diets, and the role of pulses in crop rotation and soil health improvement. However, the market faces challenges from weather-related crop variability, price fluctuations, trade restrictions, quality inconsistencies, competition from lentils, chickpeas, soy, and other protein crops, and changing demand from feed and food processors. The competitive landscape includes pulse growers, grain traders, ingredient processors, pea protein manufacturers, food companies, exporters, and private-label food brands. Future market development will depend on processing capacity, sustainable agriculture, supply chain resilience, and innovation in pea-based food and ingredient applications.

Key Market Insights

- Plant-based protein demand is one of the strongest growth drivers for the Dried Peas Market. Yellow peas are widely used for producing pea protein isolates and concentrates used in meat alternatives, protein drinks, nutrition bars, and functional foods.

- Traditional food consumption remains a stable demand base, especially for split peas and whole dried peas used in soups, stews, curries, porridges, and household meals. Their affordability and long shelf life make them important in both developed and emerging food markets.

- Food processing applications are expanding as dried peas are converted into flour, starch, fiber, and protein ingredients. These derivatives are used in bakery products, snacks, sauces, gluten-free foods, ready meals, and high-protein formulations.

- Animal feed and pet food represent important demand areas, with dried peas used as a protein and energy ingredient in feed formulations. Pea-based ingredients are also gaining attention in premium pet food due to digestibility and plant-based positioning.

- Sustainability is strengthening market appeal because peas support nitrogen fixation, crop rotation, and reduced dependence on synthetic fertilizers. This gives dried peas a strong position in sustainable agriculture and climate-conscious food supply chains.

- Organic and non-GMO dried peas are gaining traction among premium food brands and health-focused consumers. These products are especially relevant in clean-label foods, natural snacks, plant-based meals, and specialty retail channels.

- Supply reliability remains a key market challenge because pea production is influenced by weather, crop disease, harvest quality, and regional growing conditions. Processors and exporters increasingly prioritize diversified sourcing and quality control.

- Pea fractionation capacity is becoming a major competitive factor, as demand shifts from commodity pulses toward higher-value pea protein, starch, and fiber ingredients. Companies with integrated processing capabilities are better positioned.

- Snack innovation is creating new opportunities for dried peas through roasted peas, pea crisps, extruded snacks, pulse chips, and high-protein savory products. This trend supports demand from health-conscious and convenience-oriented consumers.

- Future market growth will be shaped by plant-based food innovation, pulse ingredient processing, sustainable farming systems, global trade flows, and consumer demand for affordable nutrition. Suppliers offering consistent quality, traceability, and value-added formats are expected to remain competitive.

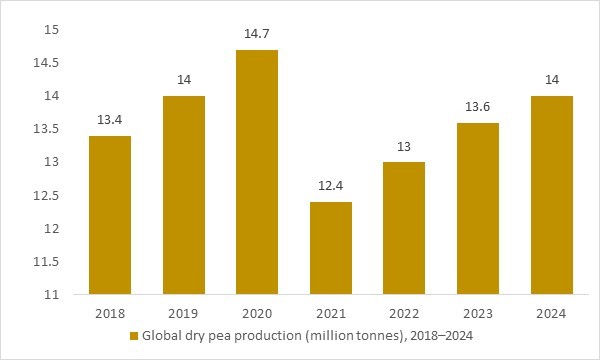

Global dry pea production (million tonnes), 2018–2024

Figure: Global dry pea production (million tonnes), 2018–2024, illustrating the stable raw-material base and long-term supply supporting growth in the dried peas market.

- Global dry pea production has remained relatively stable from 2018 to 2024, with only moderate year-to-year fluctuations. This consistent raw-material base underpins the dried peas market, supporting long-term contracts, expansion into value-added pea ingredients, and reliable supply for food, feed, and nutraceutical applications worldwide.

Regional Analysis

North America Dried Peas Market

The North America Dried Peas Market is supported by strong pulse farming, advanced grain handling infrastructure, plant-based protein processing, animal feed demand, and established export channels. Market dynamics are shaped by the availability of yellow peas for protein extraction, growing demand for pea flour and pea fiber, and increasing use of dried peas in soups, snacks, pet food, and meat alternative formulations. Lucrative opportunities exist for suppliers serving plant-based food manufacturers, protein ingredient processors, clean-label snack brands, and premium pet food producers. Latest trends include expansion of pea protein processing, demand for non-GMO and organic pulses, traceable sourcing, and sustainable crop rotation practices. The forecast outlook remains positive as food manufacturers continue seeking affordable, functional, and sustainable plant protein ingredients. Recent developments are focused on pulse processing capacity, ingredient innovation, export market diversification, and stronger quality control across food and feed applications.

Asia Pacific Dried Peas Market

The Asia Pacific Dried Peas Market is expanding due to rising demand for affordable plant-based protein, traditional pulse consumption, food processing growth, animal feed use, and increasing adoption of pea-derived ingredients. Market dynamics are influenced by population growth, urbanization, changing diets, vegetarian food habits in several markets, and rising demand for convenience foods and pulse-based snacks. Lucrative opportunities are visible in dried pea imports, split peas, pea flour, protein extraction, instant foods, meat alternatives, bakery applications, and pet nutrition. Latest trends include growing use of yellow peas in plant-based foods, expansion of pulse milling, demand for clean-label protein ingredients, and greater interest in healthier savory snacks. The forecast outlook is strong as regional food manufacturers seek cost-effective and versatile ingredients. Recent developments include increased pulse processing activity, stronger trade flows, and broader use of pea ingredients in packaged foods, nutrition products, and feed formulations.

Europe Dried Peas Market

The Europe Dried Peas Market is shaped by strong demand for sustainable proteins, plant-based food innovation, pulse crop development, and increasing use of peas in meat alternatives, bakery products, snacks, pet food, and animal feed. Market dynamics are supported by consumer preference for vegetarian and flexitarian diets, clean-label foods, local sourcing, and reduced reliance on imported protein crops. Lucrative opportunities exist for suppliers offering organic dried peas, pea protein, pea starch, pea fiber, and food-grade pea flour for premium and functional food applications. Latest trends include growth in plant-based meat products, high-protein snacks, gluten-free foods, and sustainable agriculture programs using pulses for crop rotation. The forecast outlook remains favorable as European food companies continue expanding plant protein portfolios. Recent developments are centered on local pea processing, ingredient reformulation, traceability, and investment in pulse-based alternatives for food and feed industries.

Middle East & Africa Dried Peas Market

The Middle East & Africa Dried Peas Market is developing with demand from household consumption, foodservice, institutional catering, packaged foods, animal feed, and imported pulse distribution. Market dynamics are supported by the need for affordable protein sources, long-shelf-life staples, urban retail expansion, and rising consumption of pulses in soups, stews, curries, and processed foods. Lucrative opportunities exist for exporters, traders, pulse millers, private-label food brands, and processors offering split peas, whole dried peas, pea flour, and value-added pulse products. Latest trends include increased demand for affordable plant proteins, growth in packaged dry pulses, and use of peas in animal feed and food aid channels. The forecast outlook is improving as population growth, food security priorities, and modern grocery distribution support pulse demand. Recent developments are focused on import diversification, milling capacity, branded packaged pulses, and stronger demand from foodservice and institutional buyers.

South & Central America Dried Peas Market

The South & Central America Dried Peas Market is supported by demand from household cooking, food processing, animal feed, snacks, soups, and emerging plant-based food applications. Market dynamics are influenced by affordability, dietary diversity, pulse imports, agricultural production potential, and growing interest in sustainable protein sources. Lucrative opportunities exist for suppliers serving packaged pulse brands, pea flour processors, snack manufacturers, pet food producers, and feed formulators. Latest trends include greater use of dried peas in value-added foods, healthier snacks, plant protein blends, and cost-effective feed ingredients. The forecast outlook is moderately positive as food manufacturers look for versatile ingredients that support affordability, nutrition, and clean-label positioning. Recent developments include expansion of pulse distribution, improved processing and packaging formats, and increasing awareness of peas as a sustainable and functional food ingredient.

Report Scope

| Parameter | Dried Peas Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Diagnostic Method, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Green Peas

- Yellow Peas

By Application

- Food & Beverage

- Pharmaceutical & Nutraceutical

- Animal Feed

- Cosmetics & Personal Care

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Covered

Archer Daniels Midland, AGT Food and Ingredients, Ceres Global, Batory Foods, Ingredion, Parakh Agro Industries, Agrocorp International, Blue Sky Organic Farms, Palouse Brand, Goya Foods, BroadGrain Commodities, Simpson Seeds, Woodland Foods, Marrow Fine Foods, Viterra

Recent Industry Developments

Jan 2026 – Roquette: Highlighted scale-up progress at its Manitoba pea-processing complex, designed to process up to ~125,000 metric tons of yellow peas per year at full run. The update reinforces continued investment in large-volume pea ingredient manufacturing capacity tied to food and nutrition demand.

Nov 2024 – Roquette Canada: Announced investment in new equipment to improve efficiency and reliability at its Portage la Prairie pea processing site. The upgrade supports higher uptime and more consistent throughput for yellow-pea processing operations.

Nov 2024 – Ingredion & Lantmännen: Formed a strategic partnership to accelerate yellow pea protein isolate development in Europe, with Lantmännen committing €100M+ toward a new Swedish plant targeted for completion in 2027. The move signals long-term pull for dried peas as a key raw material.

Jun 2024 – Louis Dreyfus Company (LDC): Started construction of a pea protein isolate plant in Yorkton, Saskatchewan, with operations targeted by end-2025. The facility expands North American processing capacity for pea-based ingredients.

Feb 2024 – Louis Dreyfus Company (LDC): Officially announced the Yorkton pea protein project, positioning it to supply taste-neutral, functional pea ingredients for dairy alternatives and high-protein nutrition. The announcement reflects continued vertical integration and regionalization of pea supply chains.

Jun 2023 – COSUCRA: Secured €45M to support expansion and modernization, including increased capacity for pea-based ingredients. The funding supports higher production capability and energy-transition upgrades for industrial pea processing.

FAQ's

The Global Dried Peas Market is estimated to generate USD 7.5 billion in revenue in 2026.

The Global Dried Peas Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 8.03% during the forecast period from 2026 to 2034.

The Dried Peas Market is estimated to reach USD 13.98 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!