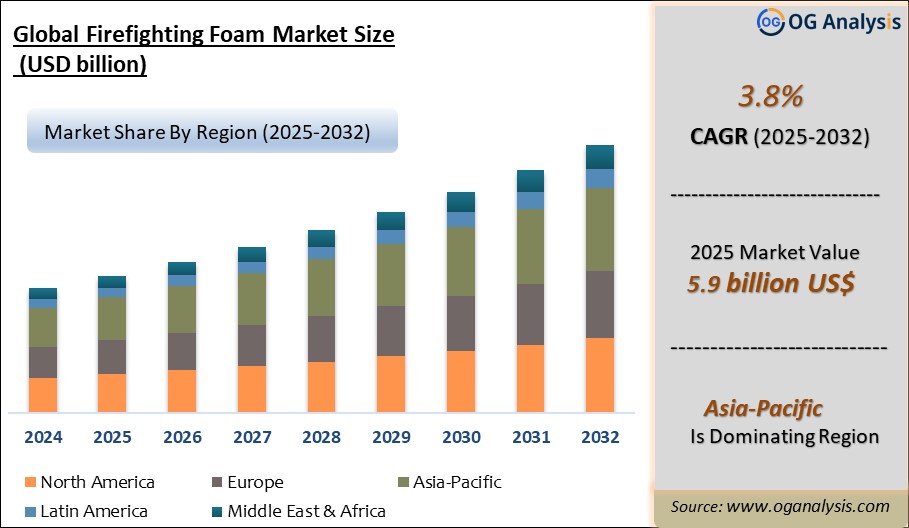

"The Firefighting Foam Market Size was valued at $ 6.1 billion in 2026. Worldwide sales of Firefighting Foam are expected to grow at a significant CAGR of 3.8%, reaching $ 8.4 billion by the end of the forecast period in 2034."

The Firefighting Foam Market is gaining importance as industrial facilities, airports, defense establishments, oil and gas sites, marine operations, chemical plants, and emergency response agencies focus on effective fire suppression for high-risk flammable liquid hazards. Firefighting foam is used to control, suppress, and prevent re-ignition by forming a protective blanket over burning fuels, separating oxygen from the fire surface, cooling the affected area, and reducing vapor release. Demand is supported by the need for rapid response in fuel fires, storage tank incidents, aircraft rescue operations, industrial spills, warehouse fires, and hazardous material emergencies. Foam concentrates are available in different types, including aqueous film-forming foam, alcohol-resistant foam, protein foam, fluoroprotein foam, synthetic foam, and fluorine-free foam.

Market development is being shaped by stricter environmental expectations, safety regulations, and growing transition toward fluorine-free firefighting foam solutions. Concerns over persistent chemicals in traditional fluorinated foams are encouraging end users to evaluate safer alternatives with lower environmental impact while maintaining suppression performance. Manufacturers are focusing on foam concentrates with improved burn-back resistance, faster knockdown, fuel compatibility, longer shelf life, and easier cleanup. Demand is also influenced by fire safety upgrades, industrial risk management, insurance requirements, and emergency preparedness planning. However, the market faces challenges from regulatory uncertainty, foam disposal costs, performance validation, equipment compatibility, and the need to replace legacy foam inventories. Overall, firefighting foam remains a critical fire protection solution, with future growth driven by safer formulations, compliance-led replacement demand, and performance-focused innovation.

Regional Analysis

North America Firefighting Foam Market

North America is a mature firefighting foam market, supported by strong demand from airports, oil and gas facilities, chemical plants, defense sites, marine operations, municipal fire departments, and industrial emergency response teams. The United States is seeing significant foam replacement activity as airports and high-risk facilities transition from legacy fluorinated foams toward fluorine-free alternatives. The FAA has prepared a transition plan for aircraft firefighting foam to support an orderly move toward fluorine-free foam for aviation fire safety applications. This shift is creating demand for foam testing, equipment flushing, storage tank replacement, training, and compliant disposal solutions.

Europe Firefighting Foam Market

Europe is a regulation-driven market, with strong demand from aviation, petrochemicals, refineries, marine terminals, manufacturing, utilities, and municipal fire services. The region is moving rapidly toward fluorine-free firefighting foam due to strict environmental controls on PFAS-containing products. The European Commission announced restrictions on PFAS in firefighting foams, with phased transition periods depending on application risk and operational requirements. This is accelerating replacement of legacy AFFF inventories and creating opportunities for approved fluorine-free foam systems, testing services, and foam management solutions.

Asia-Pacific Firefighting Foam Market

Asia-Pacific is a high-growth region for firefighting foam, supported by industrial expansion, petrochemical projects, ports, airports, manufacturing facilities, power plants, mining, and urban fire safety modernization. China, India, Japan, South Korea, Australia, and Southeast Asian countries are key demand centers due to large industrial bases and rising investment in fire protection infrastructure. Demand remains strong for AFFF, alcohol-resistant foam, and synthetic foam, while fluorine-free alternatives are gaining attention as multinational companies and regulators increase environmental scrutiny. Industrial users are prioritizing reliable knockdown, fuel compatibility, cost efficiency, and compliance with evolving fire safety standards.

Middle East & Africa Firefighting Foam Market

The Middle East & Africa market is supported by oil and gas production, refineries, petrochemical complexes, aviation infrastructure, ports, mining, defense facilities, and industrial fire protection systems. Gulf countries show stronger demand due to high concentration of hydrocarbon-related assets and large-scale industrial safety requirements. Firefighting foam is especially important for fuel storage tanks, process plants, offshore platforms, aircraft rescue, and marine terminals. Adoption of fluorine-free foam is gradually increasing, but buyers remain focused on proven performance, equipment compatibility, heat resistance, and reliability in high-risk fire scenarios.

South & Central America Firefighting Foam Market

South & Central America offers steady opportunities for firefighting foam, led by demand from oil and gas, mining, aviation, ports, chemicals, manufacturing, and municipal fire services. Brazil, Mexico, Chile, Argentina, Colombia, and Peru are important markets where foam is used for flammable liquid fire protection and emergency response. Growth is supported by industrial safety upgrades, airport modernization, and greater awareness of environmental risks linked to legacy foam use. However, adoption of advanced fluorine-free products may remain gradual due to budget constraints, import dependence, training needs, and uneven regulatory enforcement.

Trade Intelligence for firefighting foam market

| Global Chemical products and preparations n.e.s. Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 35,660 | 45,517 | 51,209 | 51,538 | 48,535 |

| China | 6,527 | 8,299 | 7,213 | 6,515 | 6,842 |

| United States of America | 4,302 | 4,215 | 6,300 | 7,856 | 6,245 |

| Germany | 2,446 | 2,901 | 2,983 | 2,843 | 2,829 |

| Hungary | 503 | 1,069 | 2,363 | 3,723 | 2,093 |

| Korea, Republic of | 1,713 | 1,886 | 1,819 | 1,694 | 1,698 |

| Source: OGAnalysis, International Trade Centre (ITC) | |||||

- China, United States of America, Germany, Hungary and Korea, Republic of are the top five countries importing 40.6% of global Chemical products and preparations n.e.s. in 2024

- Global Chemical products and preparations n.e.s. Imports increased by 36.1% between 2020 and 2024

- China accounts for 14.1% of global Chemical products and preparations n.e.s. trade in 2024

- United States of America accounts for 12.9% of global Chemical products and preparations n.e.s. trade in 2024

- Germany accounts for 5.8% of global Chemical products and preparations n.e.s. trade in 2024

| Global Chemical products and preparations n.e.s. Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

Key Insights

- Fluorine-free firefighting foam is gaining strong market attention due to environmental and regulatory concerns around traditional fluorinated foam. End users are increasingly evaluating alternatives that reduce persistence concerns while maintaining reliable fire suppression performance.

- Oil and gas, aviation, marine, chemical, and industrial facilities remain major application areas for firefighting foam. These sectors require fast knockdown, vapor suppression, and burn-back resistance for high-risk flammable liquid fires.

- Aqueous film-forming foam has historically been widely used for hydrocarbon fuel fires. However, environmental scrutiny is encouraging many organizations to transition toward next-generation foam chemistries.

- Alcohol-resistant foam is important for polar solvent and mixed-fuel fire risks. It is used where fuels such as alcohols, ketones, and oxygenated solvents can break down conventional foam blankets.

- Foam replacement programs are creating strong demand across industrial and public safety users. Organizations are reviewing legacy inventories, disposal practices, and equipment compatibility as regulations become stricter.

- Fire departments and emergency response teams require foam products that are easy to deploy under pressure. Storage stability, mixing behavior, nozzle compatibility, and rapid field performance are key purchasing factors.

- Environmental management is becoming a major product selection criterion. Buyers increasingly consider toxicity, biodegradability, persistence, runoff handling, and disposal requirements before adopting foam solutions.

- Training and operational readiness remain important for effective foam use. Proper proportioning, application technique, equipment maintenance, and scenario-based drills directly affect fire suppression outcomes.

- Product innovation is focused on balancing safety, sustainability, and suppression capability. Manufacturers are improving foam expansion, drainage time, fuel sealing, heat resistance, and compatibility with modern firefighting systems.

- Future market growth will depend on regulatory compliance, industrial safety investment, and confidence in fluorine-free performance. Suppliers offering tested, approved, and environmentally responsible foam solutions are likely to gain stronger positioning.

Report Scope

| Parameter | Firefighting Foam Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Material Type, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Aqueous Film Forming Foam (AFFF)

- Alcohol Resistant Aqueous Film Forming Foam (AR-AFFF)

- Protein Foam (PF)

- Synthetic Detergent Foam (Medium and High Expansion)

- Others (Class A foams, fluorine-free foams, and other environmentally safe foam)

By Material Type

- Surfactant

- Fluorosurfactant

- Perfluorooctanoic Acid (PFOA)

- Others (Fluorotelomers, Glycol and Gums)

By End User

- Oil & Gas

- Aviation

- Marine

- Mining

- Others (Heavy Industries, Pharmaceutical Industry, Utility Industry, Solvents & Coatings Industry, and Others)

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies

- BIO EX S.A.S.

- ANGUS FIRE

- National Foam

- Perimeter Solution

- DIC Corp.

- Johnson Controls

- Dafo Fomtec AB

- Fabrik Chemischer Praparate von Dr. Richard Sthamber GmbH & Co. KG

- Kerr Fire

- SFFECO GLOBAL

Recent Developments

June 2026: Tyco Fire Products agreed to a settlement with Wisconsin over PFAS contamination linked to legacy firefighting foam activities in the Marinette area. The case reinforces growing liability pressure on foam manufacturers and accelerates demand for safer fluorine-free alternatives.

May 2026: Australia filed a major lawsuit against 3M over PFAS contamination associated with firefighting foam use at defence sites. The development highlights rising government action on foam-related environmental cleanup, corporate accountability, and legacy AFFF replacement.

April 2026: MBS International Airport in Michigan awarded a PFAS decontamination contract to support transition from AFFF systems to fluorine-free firefighting foam. The project includes equipment cleanup, fluorine-free foam procurement, vehicle testing, and FAA readiness requirements.

March 2026: Perimeter Solutions announced that SOLBERG EVOLUTION 3% SFFF became the first Newtonian fluorine-free foam to earn FM approval. The approval strengthens the product’s positioning for aviation, hangar, sprinkler, and engineered fire suppression applications.

February 2026: Johnson Controls introduced NFF-331 3x3, a non-fluorinated foam solution for sprinkler systems under the Ansul, Chemguard, and Skum brands. The product is positioned as a biodegradable and PFAS-free alternative for Class B fire protection.

January 2026: New shipboard fire-extinguishing media rules came into force, prohibiting PFOS-containing firefighting foams under International Maritime Organization requirements. Foam manufacturers must provide PFOS-free declarations with details such as foam type, batch number, production period, and approval references.

October 2025: The European Commission restricted PFAS use in firefighting foams, with phased transition periods depending on application type and risk level. This is expected to drive large-scale replacement of PFAS-based foam inventories across municipal, portable, aviation, and industrial fire protection systems.

FAQ's

The Firefighting Foam Market is estimated to reach USD 7.7 billion by 2032.

The Global Firefighting Foam Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 3.8% during the forecast period from 2026 to 2032.

The Global Firefighting Foam Market is estimated to generate USD 6.1 billion in revenue in 2026.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!