"The Flexible 3D Printer Resin Market was valued at $416.7 million in 2025 and is projected to reach $1168 million by 2034, growing at a CAGR of 13.75%."

The Flexible 3D Printer Resin Market is growing steadily as additive manufacturing continues to evolve beyond prototyping into end-use parts and functional products. Flexible resins are widely used to produce rubber-like parts, soft-touch components, gaskets, and medical wearables due to their elasticity and resilience. These resins offer enhanced mechanical properties such as high elongation at break and excellent impact resistance, making them suitable for demanding applications across the consumer goods, automotive, dental, and healthcare industries. The market is supported by increased demand for functional prototyping and mass customization using SLA, DLP, and LCD-based resin printers, particularly among design engineers and hobbyists. As material formulation improves and costs become more accessible, adoption of flexible resins is expected to rise significantly.

In 2024, the Flexible 3D Printer Resin Market witnessed a wave of innovation in biocompatible and skin-safe materials, catering to growing demand in medical and dental sectors. Leading manufacturers launched resins with improved tear strength and elasticity for end-use wearables and orthopedic models. Several resin printer OEMs entered into partnerships with material science firms to co-develop proprietary flexible resins optimized for their hardware platforms. Additionally, the year saw rising adoption in the fashion accessories and consumer electronics sectors, where flexible components like phone cases, grips, and straps were produced at scale. Supply chains for photopolymers stabilized post-pandemic, allowing better pricing and inventory availability globally.

Looking ahead, 2025 is anticipated to bring advancements in recyclable and bio-based flexible 3D printing resins, aligning with sustainability trends across industries. The focus will shift toward high-performance elastomers that match thermoplastic urethane (TPU) properties, enabling broader industrial usage. Continuous innovation will likely lead to resins that require less post-processing and exhibit lower shrinkage, enhancing precision and part accuracy. Integration of AI-based slicing tools for optimizing flexible resin prints is expected to improve print success rates and reduce waste. As resin 3D printing becomes more affordable and user-friendly, a new wave of small businesses and creative professionals are expected to drive market expansion through decentralized production models.

Trade Intelligence Of Flexible 3D Printer Resin Market

| Global Saturated polyesters in primary forms Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 8,708 | 12,411 | 13,130 | 10,939 | 11,181 |

| China | 1,232 | 1,642 | 1,664 | 1,304 | 1,517 |

| Germany | 865 | 1,213 | 1,314 | 1,021 | 945 |

| United States of America | 456 | 644 | 818 | 586 | 699 |

| Belgium | 420 | 757 | 817 | 686 | 615 |

| Mexico | 313 | 429 | 504 | 494 | 516 |

|

| |||||

| Source: OGAnalysis | |||||

- China, Germany, United States of America, Belgium and Mexico are the top five countries importing 38.4% of global Saturated polyesters in primary forms in 2024

- China accounts for 13.6% of global Saturated polyesters in primary forms trade in 2024

- Germany accounts for 8.5% of global Saturated polyesters in primary forms trade in 2024

- United States of America accounts for 6.3% of global Saturated polyesters in primary forms trade in 2024

| Global Saturated polyesters in primary forms Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

Key Insights

- Flexible 3D printer resins evolved from early rubber-like photopolymers that were mainly used for concept models, and have since progressed to formulations capable of sustaining repeated flexing and functional testing. This historical shift from visual prototypes to performance-driven parts underpins current expectations for durability and repeatability in flexible resin applications.

- The market is closely linked to the installed base of desktop and industrial SLA and DLP systems, with flexible resins acting as an important complement to standard rigid, tough, and high-temperature materials. As hardware platforms improve in resolution and reliability, demand for specialized flexible resins that fully exploit these capabilities is increasing.

- Key end-use sectors include consumer electronics, where flexible resins are used to prototype buttons, housings, and over-molded features, and the medical and dental fields, where soft components, ergonomic grips, and device enclosures benefit from skin-friendly elasticity. Automotive and transportation applications rely on flexible resins for seals, vibration-damping components, and interior trim concepts in early development phases.

- A major trend is the emergence of resins that offer tunable softness, allowing users to select or blend formulations to achieve different elasticity levels for distinct use cases. This enables design teams to quickly iterate around feel, fit, and functional behavior without resorting to separate molding processes during early design stages.

- The drive toward production-grade additive manufacturing is encouraging suppliers to improve fatigue resistance, tear strength, and dimensional stability in flexible resins so that parts can withstand extended use or limited end-use deployment. Better performance under cyclic loading expands opportunities in tooling inserts, robotic grippers, and low-volume functional parts.

- User experience and workflow are critical differentiators, with market-leading flexible resins designed for predictable viscosity, stable storage, straightforward handling, and consistent curing behavior. Clear guidance on exposure settings, post-curing protocols, and support removal helps reduce failure rates and material waste in day-to-day operations.

- Environmental and safety considerations are gaining importance, prompting development of flexible resins with lower odor, reduced irritating components, and more favorable handling characteristics. Some suppliers are also exploring bio-derived raw materials and improved recyclability of waste resin to align with broader sustainability goals in manufacturing.

- The competitive landscape includes proprietary closed-material ecosystems, which emphasize validated performance and printer–material integration, and open-platform ecosystems, where independent resin manufacturers compete on price, niche performance attributes, and compatibility with multiple printers. This dual structure provides users with choice but also increases the importance of application-specific testing.

- Integration with multi-material and hybrid manufacturing workflows is a growing opportunity, as flexible resins are used alongside rigid and engineering-grade materials to create assemblies that more closely mimic final products. Designers can experiment with over-molded effects, living hinges, seals, and soft-touch regions in a single design cycle, shortening time-to-market.

- Looking ahead, the Flexible 3D Printer Resin Market is expected to benefit from ongoing expansion of additive manufacturing into small-batch and customized production, especially in medical devices, wearables, consumer products, and robotics. Suppliers that combine advanced polymer chemistry, strong application support, and alignment with evolving safety and sustainability expectations are likely to capture a disproportionate share of future growth.

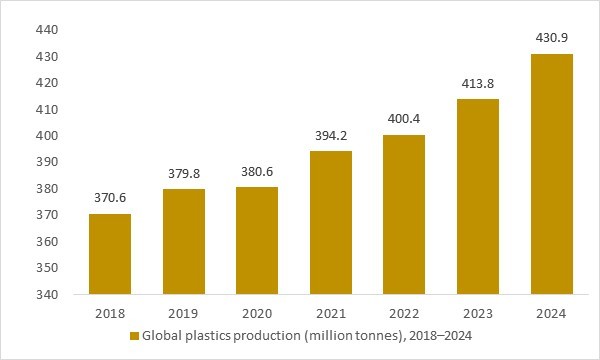

Global plastics production (million tonnes), 2018–2024

Figure: Global plastics production increased steadily between 2018 and 2024, expanding the overall polymer feedstock base available for specialty materials such as flexible 3D printer resins. The rising scale of plastics output supports investments in photopolymers and elastomeric resins used across automotive, consumer goods, medical devices and industrial prototyping.

- The flexible 3D printer resin market is built on an expanding polymer feedstock base. As illustrated in the figure below, global plastics production has grown consistently from 2018 to 2024. This structural increase in polymer output underpins long-term availability of monomers and oligomers used to formulate flexible photopolymer and elastomeric 3D printing resins.

Regional Insights

North America Flexible 3D Printer Resin Market

In North America, the flexible 3D printer resin market is driven by strong adoption of SLA/DLP technologies in product development, medical devices, dental labs, consumer electronics and industrial tooling. OEMs, service bureaus and in-house design teams increasingly rely on flexible and elastomeric resins for seals, gaskets, wearable components, overmold-like features and soft-touch ergonomics that cannot be replicated with rigid materials alone. A large installed base of professional desktop and benchtop printers, combined with growth in industrial systems, supports steady material consumption and experimentation with new flexible chemistries. Major chemical companies and printer OEMs are launching high-rebound elastomeric resins tailored for functional prototyping and low-volume end-use parts, emphasizing tear resistance, snap-back and stable performance after aging. Regulatory expectations around safety, emissions and workplace exposure also shape formulations, encouraging lower-odor, better-handled flexible resins suitable for office and lab environments.

Europe Flexible 3D Printer Resin Market

Europe represents a technologically advanced and regulation-intensive market for flexible 3D printer resins, with strong penetration in automotive, aerospace, industrial equipment, medical and dental applications. European users prioritize materials that combine elastomeric behavior with consistent mechanical properties, biocompatibility options and thorough documentation to meet stringent standards for medical and industrial use. Chemical majors and specialty suppliers in the region play a prominent role in photopolymer development, leveraging polymer science and application labs to create production-grade flexible resins. OEMs and service providers focus on validated material–printer workflows, including exposure settings, post-curing and long-term stability data, to support use in jigs, fixtures and functional components. As sustainability and worker safety gain emphasis, there is growing interest in lower-hazard formulations and clearer end-of-life guidance for flexible resins.

Asia-Pacific Flexible 3D Printer Resin Market

Asia-Pacific is a rapidly expanding hub for flexible 3D printer resins, underpinned by strong growth in consumer 3D printers, electronics manufacturing, automotive and emerging medical applications. China and other regional centers dominate entry-level and mid-range resin printer shipments, creating a large user base that experiments with flexible and “rubber-like” materials for consumer goods, wearables, functional gadgets and engineering prototypes. Local and international brands provide a wide range of flexible resins for LCD/MSLA and DLP systems, emphasizing affordability, printability and compatibility with popular open printers. Regional material developers such as Liqcreate and Siraya Tech focus on engineering-grade flexible and elastomeric resins for industrial users as well as prosumers, publishing best-practice guidelines for process optimization. As more high-value manufacturing moves toward additive, demand is expected to shift from hobby-centric use toward validated, application-specific flexible materials.

Report Scope

| Parameter | Flexible 3D Printer Resin Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Diagnostic Method, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Flexible 3D Printer Resin Market Segmentation

By Product

- Standard Resin

- High-Temperature Resin

- Biocompatible Resin

By Application

- Prototyping

- Tooling

- Production Parts

By End User

- Aerospace

- Automotive

- Healthcare

- Consumer Goods

By Technology

- SLA

- DLP

- FDM

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Formlabs

- Anycubic

- Photocentric Ltd

- Monocure 3D

- 3D Systems

- Elegoo

- Siraya Tech

- Protolabs

- Resione

- Phrozen

- EnvisionTEC

- Shenzhen eSUN Industrial Co., Ltd.

- XYZprinting

- Peopoly

- Nova3D

Recent Industry Developments

-

Jan 2026 – AmeraLabs: Summarized its 2025 product launches and highlighted FLX-300 elastomer resin as a key release aimed at durable, engineering-grade flexible parts. The update reinforces growing focus on long-lasting elasticity (reduced “hardening over time”) for functional applications.

-

Nov 2025 – Henkel (Loctite): Announced multiple new photopolymer materials to expand its industrial and medical resin portfolio showcased around Formnext. The releases reflect continued push toward production-grade performance and broader qualified material sets for professional resin printers.

-

Oct 2025 – AmeraLabs: Introduced FLX-300, positioned as an elastic resin designed to stay flexible over time for durable elastomer-like components. The product targets applications such as gaskets, vibration dampers, and parts requiring repeated compression and rebound.

-

Dec 2024 – Raise3D (DF2 ecosystem): Expanded its DF2 resin lineup with additional high-performance materials, including Forward AM Ultracur3D® EL 4000, a flexible elastomeric resin validated for industrial DLP workflows. The move strengthens “qualified materials” availability for flexible part production on platform ecosystems.

-

Oct 2024 – Formlabs: Announced Form 4L and introduced a Developer Platform, expanding openness and workflow control for advanced users. This improves access to broader material experimentation—including specialized flexible/elastomer resin development—through stronger software and integration tools.

-

Aug 2024 – Formlabs: Released Open Material Mode (OMM) for Form 4 via a PreForm update, enabling use of third-party 405 nm resins with editable print settings. This materially expands the addressable flexible-resin landscape by reducing dependence on closed material catalogs.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Flexible 3D Printer Resin market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Flexible 3D Printer Resin market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Flexible 3D Printer Resin market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Flexible 3D Printer Resin business prospects by region, key countries, and top companies' information to channel their investments.

FAQ's

The Global Flexible 3D Printer Resin Market is estimated to generate USD 416.7 million in revenue in 2025.

The Global Flexible 3D Printer Resin Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 13.75% during the forecast period from 2025 to 2034.

The Flexible 3D Printer Resin Market is estimated to reach USD 1168 million by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!