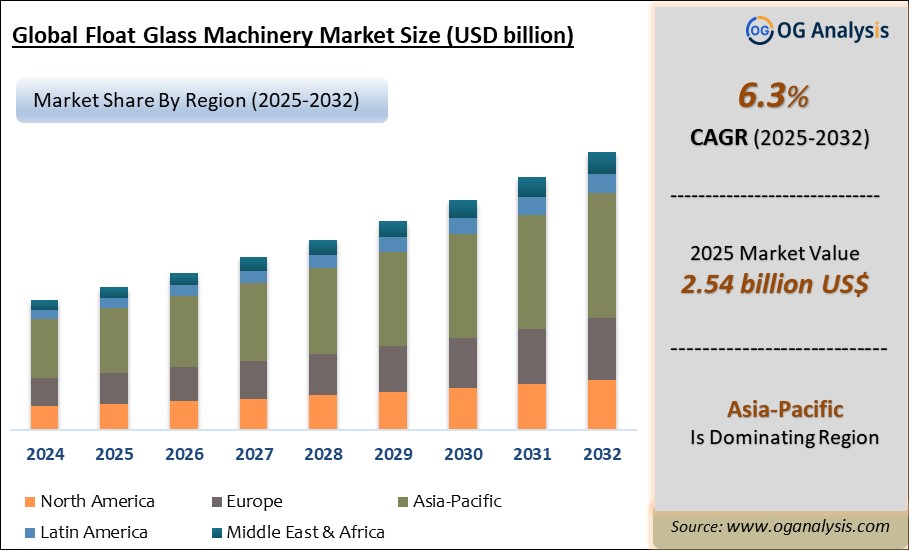

"The Float Glass Machinery Market Size is valued at $ 2.7 Billion in 2026. Worldwide sales of Float Glass Machinery Market are expected to grow at a significant CAGR of 6.3%, reaching $ 4.4 Billion by the end of the forecast period in 2032."

The Float Glass Machinery Market is a specialized segment of glass manufacturing equipment, industrial process machinery, flat glass production systems, thermal processing equipment, automation solutions, and material handling technologies, serving architectural glass, automotive glass, solar glass, display glass, appliance glass, mirror glass, interior glass, and specialty flat glass manufacturers. Float glass machinery includes raw material batching systems, melting furnaces, tin bath systems, annealing lehrs, cutting lines, inspection systems, edge grinding equipment, washing machines, coating systems, tempering furnaces, laminating lines, handling robots, conveyor systems, and process control equipment. These machines are designed to support continuous glass production with high optical quality, thickness uniformity, surface smoothness, dimensional accuracy, energy efficiency, and production reliability. The market is closely linked to construction activity, automotive production, solar photovoltaic glass demand, energy-efficient glazing, and modernization of aging float glass plants.

The market is gaining traction as glass manufacturers focus on higher productivity, lower energy consumption, improved yield, digitalized plant operations, and production of value-added glass products. Float glass machinery is increasingly engineered for larger sheet sizes, ultra-clear glass, coated glass, solar glass, low-emissivity glass, laminated safety glass, and advanced automotive glazing. Key trends include furnace energy optimization, oxygen-fuel combustion, heat recovery systems, automated defect inspection, AI-enabled process monitoring, robotic glass handling, precision cutting, smart plant control systems, and machinery designed for thinner, lighter, and high-performance glass products. Growth is supported by urban construction, green buildings, solar module manufacturing, vehicle glazing demand, infrastructure development, interior design trends, and replacement of older inefficient glass production lines. However, challenges include high capital investment, energy-intensive operations, complex installation, long project timelines, raw material and fuel cost volatility, skilled operator requirements, and cyclical demand from construction and automotive sectors. The competitive landscape includes glass machinery manufacturers, furnace engineering companies, flat glass technology providers, automation suppliers, coating equipment companies, inspection system providers, and turnkey glass plant solution providers.

Regional Analysis

North America Float Glass Machinery Market

North America Float Glass Machinery Market is supported by modernization of flat glass production lines, architectural glass demand, automotive glazing, solar glass interest, and investments in energy-efficient manufacturing. The United States remains the key regional market due to its large construction sector, automotive industry, renewable energy expansion, and advanced glass processing base. Demand is strong for furnace upgrades, automated inspection systems, cutting equipment, coating lines, tempering machinery, laminating equipment, and robotic handling systems. Glass producers in the region are increasingly focused on reducing energy consumption, improving production yield, meeting environmental compliance requirements, and producing higher-value coated and safety glass products. Opportunities are expanding in low-emissivity glass, solar-control glass, laminated architectural glass, electric vehicle glazing, and retrofit solutions for aging float lines. However, high capital costs, energy price volatility, skilled labor requirements, and cyclical construction activity remain key challenges for machinery suppliers.

Asia Pacific Float Glass Machinery Market

Asia Pacific Float Glass Machinery Market is the strongest and most dynamic regional market, driven by large-scale construction, infrastructure development, solar photovoltaic manufacturing, automotive production, and expanding flat glass capacity. China is the leading demand center due to its large glass manufacturing base, solar glass production, construction activity, and equipment manufacturing ecosystem. India, Japan, South Korea, Vietnam, Indonesia, Thailand, and Australia also contribute through architectural glass demand, automotive glazing, industrial development, and solar module supply chains. Demand is rising for float line equipment, high-capacity furnaces, tin bath systems, annealing lehrs, coating lines, automated cutting systems, quality inspection tools, and glass handling technologies. Regional manufacturers are investing in higher productivity, lower energy consumption, improved surface quality, and value-added glass production. Opportunities are especially strong in solar glass machinery, green building glass, coated glass, and plant modernization. Challenges include intense price competition, overcapacity risk in some countries, energy costs, environmental regulations, and uneven equipment quality across supplier tiers.

Europe Float Glass Machinery Market

Europe Float Glass Machinery Market is shaped by strict energy-efficiency goals, environmental regulations, advanced architectural glass demand, automotive glazing innovation, and strong emphasis on low-carbon manufacturing. Germany, France, Italy, the United Kingdom, Spain, Poland, Belgium, and the Netherlands are important markets due to established glass production, premium building materials, automotive manufacturing, and advanced machinery engineering capabilities. Demand is strong for energy-efficient furnaces, heat recovery systems, low-emission combustion technologies, coating equipment, digital process control, automated inspection systems, and retrofit solutions. European glass producers are focusing on decarbonization, circular manufacturing, high-performance glazing, low-emissivity glass, solar-control glass, laminated safety glass, and specialty flat glass products. Machinery suppliers benefit from demand for plant upgrades rather than only new capacity additions. However, high energy costs, strict compliance requirements, mature construction markets, and long investment cycles can affect project timing. Future opportunities will favor suppliers offering energy-saving technology, automation, digital monitoring, and advanced coating capabilities.

Middle East & Africa Float Glass Machinery Market

Middle East & Africa Float Glass Machinery Market is developing through construction activity, urban infrastructure, commercial real estate, solar energy projects, and industrial diversification. Gulf countries are important demand centers due to large-scale building projects, airports, hotels, commercial towers, smart cities, and solar power initiatives. Demand is focused on architectural glass processing equipment, coating lines, tempering systems, laminated glass machinery, cutting lines, and handling systems rather than extensive new float line capacity in every market. South Africa, Egypt, Saudi Arabia, the United Arab Emirates, and other emerging economies contribute through construction, automotive aftermarket glass, infrastructure projects, and local glass processing. Opportunities exist in energy-efficient glazing, solar glass processing, façade glass, safety glass, and regional manufacturing partnerships. However, the market faces challenges from import dependence, limited local float glass machinery production, high project costs, uneven industrial infrastructure, and volatility in construction investment. Suppliers with turnkey solutions, technical service, and durable machinery suited to harsh operating conditions are better positioned.

South & Central America Float Glass Machinery Market

South & Central America Float Glass Machinery Market is supported by construction, automotive production, infrastructure renovation, solar energy projects, and demand for architectural and safety glass. Brazil is the leading regional market due to its industrial base, construction activity, automotive sector, and flat glass processing capacity. Mexico, Argentina, Chile, Colombia, and Peru also contribute through building construction, façade glass demand, vehicle glazing, and infrastructure development. Demand is strongest for glass processing machinery, tempering lines, cutting systems, laminating equipment, washing machines, coating equipment, and modernization solutions for existing production and processing facilities. Opportunities are emerging in energy-efficient building glass, solar-control glazing, laminated safety glass, interior glass, and solar project-related glass processing. However, economic volatility, currency fluctuations, import costs, delayed construction projects, and limited local manufacturing of advanced float glass equipment can restrict faster adoption. Future growth will depend on construction recovery, industrial investment, renewable energy expansion, automotive production, and stronger regional service networks for machinery maintenance and upgrades.

Key Insights

- Construction and architectural glass demand is one of the strongest growth drivers for the Float Glass Machinery Market. Residential buildings, commercial towers, airports, hospitals, retail spaces, and infrastructure projects require clear glass, tinted glass, coated glass, laminated glass, and energy-efficient glazing, supporting investment in modern float glass production and processing equipment.

- Solar glass manufacturing is becoming an important demand contributor. Rising solar photovoltaic installation is increasing the need for high-transmission, low-iron, patterned, coated, and durable glass used in solar modules. This is encouraging machinery upgrades for precision melting, uniform thickness control, surface quality, coating capability, and high-volume continuous production.

- Automotive glass applications support steady equipment demand. Windshields, side windows, rear glass, sunroofs, panoramic roofs, and electric vehicle glazing require float glass with high optical clarity, safety performance, and consistency. Machinery suppliers benefit from demand for thinner, lighter, coated, and laminated glass used in modern vehicle designs.

- Energy efficiency is a major technology trend in float glass production. Melting furnaces and thermal processing systems consume significant energy, making fuel optimization, improved insulation, waste heat recovery, advanced combustion control, and electric or hybrid heating concepts important areas of equipment development and plant modernization.

- Automation and digital control are becoming critical buying factors. Glass manufacturers are adopting process control systems, online inspection, automated cutting, robotic loading, smart sensors, and predictive maintenance tools to improve yield, reduce defects, lower labor dependence, and maintain consistent product quality across continuous production lines.

- High-quality tin bath and annealing systems remain central to float glass performance. Tin bath stability determines surface smoothness and thickness uniformity, while annealing lehrs control internal stress and glass strength. Equipment precision in these stages is essential for producing architectural, automotive, solar, and specialty flat glass.

- Coating equipment is creating higher-value opportunities. Demand for low-emissivity glass, solar-control glass, anti-reflective glass, conductive coatings, and functional glass surfaces is increasing. This supports investment in magnetron sputtering coating lines, chemical vapor deposition systems, and integrated coating technologies for value-added glass manufacturing.

- Plant modernization is a key market opportunity. Many existing float glass lines require upgrades to improve energy efficiency, environmental compliance, automation, production capacity, and product flexibility. Retrofit projects involving furnaces, inspection systems, cutting lines, control software, and handling equipment provide recurring opportunities for machinery suppliers.

- Capital intensity remains a major restraint. Float glass plants require large investments, long installation periods, high energy supply, technical expertise, and continuous operating discipline. These factors can delay new projects, especially in regions with uncertain construction demand, volatile fuel costs, or limited industrial infrastructure.

- Future market growth will be shaped by green building demand, solar glass capacity expansion, electric vehicle glazing, smart glass technologies, energy-efficient furnaces, automation, advanced coatings, and replacement of older production lines. Companies offering turnkey plant engineering, energy-saving technologies, digital monitoring, precision machinery, and reliable after-sales service are expected to remain competitive.

Market Scope

| Parameter | Float Glass Machinery Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Application, By End User, By Technology, By Distribution Channel |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Float Glass Machinery Market Segmentation

By Product

- Cutting Machines

- Grinding Machines

- Coating Machines

By Application

- Construction

- Automotive

- Electronics

By End User

- Manufacturers

- Distributors

- Retailers

By Technology

- Automated

- Semi-Automated

By Distribution Channel

- Online

- Offline

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies

- Buhler Group

- LiSEC Group

- Hegla GmbH & Co. KG

- Bottero S.p.A.

- Bystronic Glass

- Glaston Corporation

- CMS Glass Machinery

- Grenzebach Maschinenbau GmbH

- HHH Equipment Resources

- Fushan Glass Machinery

- Ashton Industrial Sales Ltd.

- Fenzi Group

- Sedak GmbH & Co. KG

- Jiangsu Landglass Technology Co., Ltd.

- Optrion Corporation

Recent Developments

In July 2025, Zippe commissioned a batch plant extension at Nanjing Electric Glass in China. The project included an upgrade to the weighing systems and the addition of a dedicated transport line to support a new furnace, representing the third phase of a long-term expansion.

In July 2025, European companies, including Horn Glass Industries, Bottero, and Zippe, formed a partnership with NovaSklo to construct a new float glass plant in Ukraine. The €240 million investment is backed by the Ukrainian government and is expected to strengthen the regional float glass supply chain.

In July 2025, LiSEC introduced the LiTROS brand, a new product line offering semi-automated float glass machinery such as horizontal washers and cutting systems. The launch aims to support small to mid-sized manufacturers with affordable, scalable technology.

In April 2025, Grenzebach collaborated with Glass Futures to develop and install an energy-efficient annealing lehr system at a pilot float glass facility in the UK. The initiative is part of efforts to decarbonize glass manufacturing and enhance sustainability through advanced machinery.

In March 2025, LandGlass Technology unveiled its next-generation glass tempering furnace at an international trade exhibition. The equipment features improved thermal efficiency, faster cycle times, and integration capabilities for smart factory systems.

In February 2025, HORN Glass Industries announced the delivery of its first hybrid-fuel float glass furnace to a facility in India. The project focuses on reducing carbon emissions and energy costs while maintaining high-quality output.

In January 2025, Bottero launched a fully automated glass cutting and stacking system tailored for float glass applications. The system integrates AI-powered defect detection and optimizes production throughput.

In December 2024, Von Ardenne completed the installation of a large-scale magnetron sputtering coater for a float glass production line in Southeast Asia. This investment enhances the value-added glass segment, particularly for solar control applications.

In November 2024, Glaston Corporation expanded its float glass processing equipment manufacturing capacity in Finland to meet growing demand from the architectural and automotive sectors.

In October 2024, Tenon Clear Glass in the Middle East placed a large-scale order for customized float glass machinery from multiple European suppliers. The procurement supports the company's expansion into premium architectural glass production.

FAQ's

The Float Glass Machinery Market is estimated to reach USD 3.89 Billion by 2032.

The Global Float Glass Machinery Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.3% during the forecast period from 2026 to 2034.

The Global Float Glass Machinery Market is estimated to generate USD 2.7 Billion in revenue in 2026.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!