"The Food Grade Alcohol Market is valued at $ 7.7 billion in 2025. Further, the market is expected to grow at a CAGR of 4.6% to reach $ 11.5 billion by 2034."

Food Grade Alcohol Market Overview

The Food Grade Alcohol Market is expanding rapidly due to its wide-ranging applications in the food and beverage, pharmaceutical, and personal care industries. Food-grade alcohol, including ethanol and isopropyl alcohol, is a crucial ingredient in food preservation, flavor extraction, and beverage production. It is extensively used in the manufacturing of alcoholic beverages, confectionery, extracts, and food colorants, making it a highly sought-after commodity. Increasing demand for premium alcoholic beverages and the rising adoption of ethanol-based sanitizers and preservatives are key growth drivers. Moreover, the clean-label movement and consumer preference for natural ingredients are pushing manufacturers to incorporate food-grade alcohol in organic extracts and herbal formulations. With stringent food safety regulations and the growing popularity of bio-based ethanol, the market is shifting toward sustainable production processes. As emerging economies witness rapid urbanization and increasing disposable incomes, the demand for food-grade alcohol in the beverage and food processing sectors is expected to surge.

In 2024, the Food Grade Alcohol Market is witnessing a surge in demand driven by innovations in beverage production and clean-label food manufacturing. The premiumization trend in alcoholic beverages, including craft spirits, organic liquors, and low-calorie alcoholic drinks, is boosting the need for high-quality food-grade alcohol. The expansion of the functional food and nutraceutical sectors is further driving growth, as food-grade ethanol is widely used in herbal extracts and pharmaceutical applications. Additionally, regulatory policies surrounding the use of synthetic preservatives are leading food manufacturers to adopt ethanol as a natural preservative. The rise of e-commerce and direct-to-consumer models in the beverage industry is increasing alcohol sales, creating lucrative opportunities for suppliers. However, fluctuating raw material prices, particularly for sugarcane and corn-based ethanol, remain a concern for market players. Companies are also facing growing scrutiny over carbon emissions from alcohol production, prompting increased investments in green and sustainable fermentation technologies.

Looking ahead to 2025 and beyond, the Food Grade Alcohol Market is expected to see a strong focus on sustainability, regulatory compliance, and product innovation. As consumer awareness of environmental concerns grows, manufacturers will adopt carbon-neutral and bio-based ethanol production processes. Governments are also likely to introduce stricter regulations on alcohol purity and safety, prompting the development of advanced filtration and distillation technologies. The demand for low-alcohol and alcohol-free beverages is set to increase, driving innovation in food-grade alcohol alternatives and fermentation techniques. Additionally, the use of ethanol in plant-based food products and alternative proteins is anticipated to rise, further expanding its market applications. Asia-Pacific is expected to witness significant growth, driven by the rapid expansion of the beverage and pharmaceutical industries, while North America and Europe will continue focusing on premium and organic alcohol products. As supply chains evolve, investments in localized production and raw material sourcing will become a priority for key industry players.

Key Trends in the Food Grade Alcohol Market

-

Strong linkage to beverage and spirits demand underpins historic growth

Historically, food-grade alcohol consumption has been driven by spirits, wine fortification and ready-to-drink beverages. Rising incomes and urbanization in emerging markets have expanded premium spirits and cocktail culture. This keeps beverage-grade ethanol as the backbone segment, even as diversification into non-beverage uses accelerates. -

Neutral grain spirit and molasses-based alcohol dominate product mix

Neutral grain spirit (NGS) from maize, wheat and other cereals remains a core feedstock for spirits, liqueurs and flavor carriers. In several regions, molasses-based alcohol from sugarcane continues to be critical due to abundant cane resources and cost advantages. The balance between grain-based and molasses-based routes is shaped by crop yields, price volatility and regional agricultural policy. -

Expanding role of food-grade alcohol as a solvent and carrier in F&B

Food-grade ethanol is widely used as a solvent for flavors, colors, botanical extracts and essential oils. Growth of clean-label, natural flavors and plant-based extracts is expanding demand for high-purity alcohol with low impurity profiles. This application benefits from the rising sophistication of processed foods, bakery products, confectionery and beverages that rely on complex flavor systems. -

Rising demand from confectionery, bakery and culinary applications

Alcohol is used for fortification, preservation and flavor enhancement in chocolates, truffles, desserts, fillings, and specialty bakery items. Premiumization in confectionery, seasonal products and gourmet bakery concepts supports higher use of alcohol-containing fillings and flavor carriers. Foodservice and QSR chains are also adopting more alcohol-based sauces, glazes and dessert formats. -

Surging use in non-alcoholic and low-alcohol beverage formulations

Ironically, the rise of non-alcoholic beers, wines and mocktails supports the food-grade alcohol market as ethanol is used in dealcoholization processes and as a flavor extraction medium. Low-alcohol and ready-to-drink formulations often rely on precise alcohol levels for mouthfeel and stability. This drives demand for consistent, high-quality alcohol with tight control on impurities and sensory profile. -

Shift toward higher purity grades and stringent quality standards

End-users increasingly demand pharma- or extra-neutral-grade qualities even in food applications to minimize off-notes and contaminants. Compliance with food safety, allergen, and residual solvent regulations is pushing producers to invest in advanced distillation, rectification and filtration technologies. Suppliers that can consistently meet global standards (USP, FCC, EU specs) gain advantage in multinational contracts. -

Feedstock diversification and sustainability positioning gain importance

Maize, wheat, sugarcane and cassava remain the primary feedstocks, but there is growing interest in non-GMO and sustainably sourced grains. Producers are emphasizing lower carbon footprints, energy-efficient distilleries and circular use of by-products such as DDGS and vinasse. Sustainability credentials help suppliers align with beverage majors and food brands with ambitious ESG and climate targets. -

Capacity expansion and integration with fuel ethanol impact market dynamics

In many regions, food-grade and fuel-grade alcohol share production infrastructure, with flexible plants shifting between grades depending on price signals. Expansion of fuel ethanol mandates can tighten supply or influence allocation toward higher-margin food and beverage contracts. Strategic integration and flexible production planning are thus key to managing volatility and ensuring reliable supply to food customers. -

Regulatory, taxation and labeling frameworks shape regional demand

Excise duties, labeling rules for alcohol-containing foods, and restrictions on marketing alcoholic products directly affect consumption patterns. Stricter controls on high-strength beverages can push innovation into flavored, lower-ABV and RTD segments rather than volume decline. Food-grade alcohol producers must navigate varying national standards and documentation requirements to serve multinational clients. -

Future growth anchored in premium, functional and experiential products

Looking ahead, growth is driven less by bulk commodity volume and more by value-added applications—premium spirits, craft and flavored products, functional beverages, and sophisticated food formulations. Producers that offer tailored specifications, consistent supply, strong quality documentation and sustainability narratives will be best positioned to capture long-term, higher-margin opportunities in the global food-grade alcohol market.

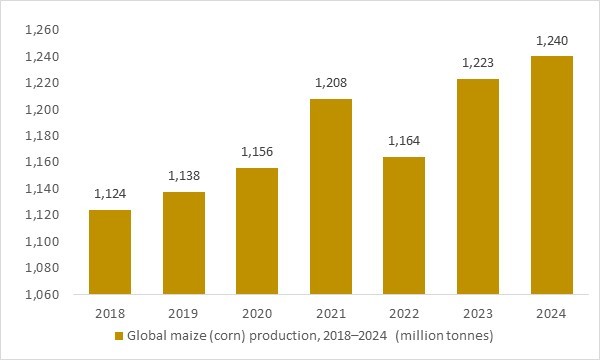

Global maize (corn) production, 2018–2024 (million tonnes)

Figure: Global maize (corn) production increased from about 1.12 billion tonnes in 2018 to a record level above 1.22 billion tonnes by 2023, with further growth expected in 2024. As maize is a key starch feedstock for grain-based neutral spirit and food-grade ethanol, this abundant and expanding supply base underpins long-term growth in the food-grade alcohol market, supporting spirits, RTD beverages, flavours, vinegar and pharmaceutical solvents. OG Analysis estimates, aligned with international crop and coarse-grain outlooks, highlight how upstream maize trends support capacity utilisation in food-grade alcohol distilleries.

Global maize production – a key starch feedstock for food-grade ethanol and neutral spirits – increased from about 1.12 billion tonnes in 2018 to a record level above 1.22 billion tonnes by 2023, with output projected around 1.24 billion tonnes in 2024. FAO and USDA data show that maize is the world’s largest grain crop and a major source of fermentable carbohydrates for high-purity alcohol used in spirits, RTD drinks, flavour and fragrance bases, vinegar, and pharmaceutical and personal-care solvents. The combination of abundant maize supply and rising yields lowers the risk of feedstock shortages and helps stabilise production economics for food-grade alcohol distilleries. This expanding maize base therefore underpins long-term growth in the food-grade alcohol market, especially in regions where grain-based neutral spirit dominates over molasses-based alcohol.

Report Scope

| Parameter | Food Grade Alcohol Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Product

- Ethanol

- Polyols

By Source

- Sugarcane And Molasses

- Fruits

- Grains

By Function

- Coatings

- Preservatives

- Flavoring

- Other Functions

By Application

- Spirits

- Vinegar

- Extracts

- Cosmetics

- Pharmaceutical

- Industrial Application

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- MGP Ingredients inc.

- Cargill Incorporated

- Archer Daniels Midland Co.

- Cristalco SAS

- Grain Processing Corporation

- Wilmar International Ltd.

- Malindra Group.

- MOLINDO Group

- Extractohol

- Pure Alcohol Solutions

- Ethimex Ltd.

- Roquette Freres SA

- Glacial Grain Spirits LLC

- INGREDION Inc.

- Fonterra Co-Operative Group Ltd.

- Ethanolsa Pty Ltd.

- Bartow Ethanol of Florida L.C.

- Greenfield Global Inc.

- Bartlett Grain Company

- United Ethanol LLC

- Pacific Ethanol Inc.

- Valero Energy Corporation

- Flint Hills Resources

- Green Plains Inc.

- The Andersons Inc.

- White Energy

- Big River Resources LLC

- Southwest Iowa Renewable Energy LLC

- Marquis Energy LLC

- ICM Inc. .

FAQ's

The Global Food Grade Alcohol Market is estimated to generate USD 7.7 billion in revenue in 2025.

The Global Food Grade Alcohol Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.6% during the forecast period from 2025 to 2034.

The Food Grade Alcohol Market is estimated to reach USD 11.5 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!