"The Food Grade Antifoaming Agents Market was valued at $ 729.2 million in 2026 and is projected to reach $ 1076.6 million by 2034, growing at a CAGR of 5.72%."

The Food Grade Antifoaming Agents Market is gaining steady traction as food and beverage manufacturers focus on improving processing efficiency, product consistency, and operational control. Food grade antifoaming agents are used to prevent or reduce unwanted foam formation during production, mixing, fermentation, boiling, filling, packaging, and cleaning operations. These additives are widely used across beverages, dairy products, bakery and confectionery, edible oils, processed foods, sugar processing, sauces, soups, starch processing, and fermentation-based applications. Demand is supported by the need to maintain smooth production flow, reduce overflow losses, improve equipment utilization, and ensure consistent product texture and appearance.

Market growth is also driven by rising demand for processed foods, clean-label formulations, plant-based food production, and large-scale beverage processing. Manufacturers are focusing on silicone-based, oil-based, water-based, and bio-based antifoaming solutions that comply with food safety standards and perform effectively under different processing conditions. Product development is increasingly centered on low-dosage performance, thermal stability, easy dispersion, regulatory compliance, and minimal impact on taste, aroma, or product quality. However, the market faces challenges related to strict food additive regulations, formulation compatibility, consumer preference for natural ingredients, and the need for application-specific performance testing. Overall, food grade antifoaming agents are becoming essential processing aids for improving productivity, reducing waste, and supporting consistent quality in modern food manufacturing.

Key Insights

- Demand for food grade antifoaming agents is supported by the need to control foam during food and beverage processing. These agents help prevent overflow, product loss, contamination risk, and production interruptions.

- Beverage manufacturing remains a key application area for antifoaming agents. They are used during juice processing, soft drink production, brewing, fermentation, bottling, and cleaning operations to maintain smooth processing.

- Dairy and fermented food applications are creating steady opportunities for food grade antifoaming solutions. Foam control is important during milk processing, yogurt production, cheese making, fermentation, and whey processing.

- Silicone-based antifoaming agents are widely used due to strong foam control efficiency and low dosage requirements. Their performance makes them suitable for high-speed and high-temperature food processing operations.

- Natural and bio-based antifoaming agents are gaining attention as food manufacturers respond to clean-label trends. Plant oils, fatty acid derivatives, and other natural alternatives are being evaluated for safer and consumer-friendly formulations.

- Processed food manufacturers are adopting antifoaming agents to improve production efficiency and product consistency. These additives support smoother mixing, cooking, filling, and packaging operations across multiple food categories.

- Regulatory compliance is a critical factor in product selection. Food manufacturers require antifoaming agents that meet food safety standards, approved additive limits, and application-specific documentation.

- Compatibility with end-product quality remains highly important. Antifoaming agents must not negatively affect taste, odor, appearance, mouthfeel, texture, or shelf stability of finished food products.

- Automation and high-speed food processing are increasing the need for reliable foam-control solutions. Efficient antifoaming agents help manufacturers maintain continuous production and reduce downtime.

- Future growth will depend on innovation in clean-label, low-residue, and application-specific formulations. Suppliers that offer safe, effective, and regulatory-compliant products are likely to gain stronger market acceptance.

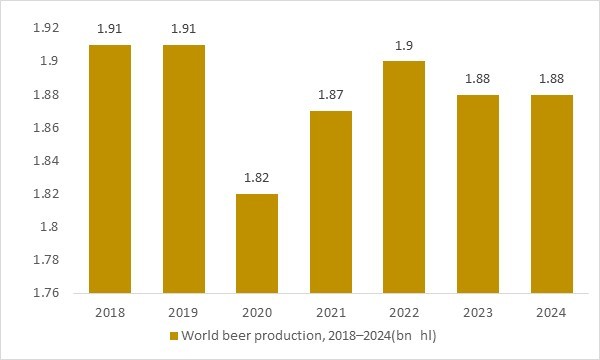

World beer production, 2018–2024(bn hl)

Figure: World beer production has remained in a high and relatively stable range of around 1.8–1.9 billion hectoliters between 2018 and 2024, creating a large, continuous fermentation base where food-grade antifoaming agents are essential for foam control. Breweries rely on silicone- and vegetable-oil-based defoamers during wort boiling, fermentation and filling to prevent overfoaming, avoid product losses and protect equipment hygiene. OG Analysis estimates based on global beer statistics highlight how sustained beer output underpins recurring demand for high-performance food-grade antifoaming agents in beverage processing.

- production, where foam control is critical during wort boiling, fermentation and packaging. Between 2018 and 2024, world beer output remained in a narrow band of 1.82–1.91 billion hectoliters, with a COVID-driven dip in 2020 followed by recovery across 2021–2022 and stabilisation around 1.88 billion hectoliters in 2023–2024. This sustained fermentation volume keeps breweries reliant on silicone- and vegetable-oil-based defoamers to avoid overfoaming, tank losses and hygiene issues. As craft, premium and specialty beers grow, the complexity and intensity of foam management increase, reinforcing long-term demand for high-performance food grade antifoaming agents.

Regional Analysis

North America Food Grade Antifoaming Agents Market

North America is a mature market for food grade antifoaming agents, supported by large-scale beverage, dairy, bakery, confectionery, edible oil, sugar processing, and processed food manufacturing. The United States leads demand due to advanced food processing infrastructure, strong packaged food consumption, and high adoption of automated production lines where foam control is critical. Manufacturers prioritize antifoaming agents that support processing efficiency while meeting strict food safety and additive-use requirements. In the U.S., defoaming agents are permitted for food processing under defined regulatory conditions, making compliance, documentation, and approved-use limits important purchasing factors.

Europe Food Grade Antifoaming Agents Market

Europe is a regulation-driven market where demand is supported by beverage processing, dairy production, bakery, sugar, starch, sauces, soups, and convenience food manufacturing. Germany, France, the UK, Italy, Spain, and the Netherlands are key demand centers due to their strong food processing and ingredient industries. Food manufacturers are increasingly focusing on clean-label, low-residue, and application-specific antifoaming solutions that do not affect taste, texture, aroma, or product appearance. EU food additive rules require additives to be authorized, assessed for safety, technologically justified, and listed with specific conditions of use, making regulatory approval a central factor for suppliers.

Asia-Pacific Food Grade Antifoaming Agents Market

Asia-Pacific is expected to remain a high-growth region for food grade antifoaming agents, supported by expanding processed food production, beverage manufacturing, dairy processing, fermentation industries, edible oil refining, and sugar processing. China, India, Japan, South Korea, Indonesia, Thailand, and Vietnam are key markets due to rising urban consumption, growing packaged food demand, and rapid expansion of food manufacturing capacity. Demand is strong for cost-efficient and high-performance silicone-based, oil-based, and water-based antifoaming agents. Local producers are also focusing on products suitable for high-temperature processing, high-speed filling, and large-scale beverage and food operations.

Middle East & Africa Food Grade Antifoaming Agents Market

The Middle East & Africa market is developing steadily, supported by packaged food growth, dairy processing, beverage production, edible oil refining, sugar processing, and rising investment in local food manufacturing. Gulf countries are expanding food processing capacity to improve food security and reduce import dependence, while South Africa, Egypt, and other African markets show demand from dairy, beverages, bakery, and processed food sectors. Non-alcoholic beverage production is also gaining attention in the Middle East, supporting foam-control needs in beverage processing and filling operations. However, fragmented regulations, price sensitivity, and limited high-end processing infrastructure can restrict faster adoption.

South & Central America Food Grade Antifoaming Agents Market

South & Central America offers steady opportunities for food grade antifoaming agents, supported by beverage, sugar, edible oil, dairy, bakery, confectionery, and processed food industries. Brazil, Mexico, Argentina, Chile, Colombia, and Peru are key markets due to their food manufacturing base and growing demand for packaged foods and drinks. Antifoaming agents are widely relevant in sugar processing, fermentation, juice production, sauces, dairy operations, and cooking applications where foam can reduce production efficiency. Growth is supported by modernization of food processing plants, but price competition, raw material dependency, and regulatory variation across countries remain key challenges.

Report Scope

| Parameter | Food Grade Antifoaming Agents Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Food Grade Antifoaming Agents Market Segmentation

By Product

- Silicone-based

- Non-silicone-based

By Application

- Beverages

- Dairy Products

- Baked Goods

- Confectionery

By End User

- Food Manufacturers

- Beverages Industry

- Bakery and Confectionery Industry

By Technology

- Chemical Synthesis

- Natural Extraction

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Dow Inc.

- BASF SE

- Evonik Industries AG

- Wacker Chemie AG

- Momentive Performance Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

- Ingredion Incorporated

- ADM (Archer Daniels Midland Company)

- AB Specialty Silicones

- Elkem ASA

- Ashland Inc.

- Kemira Oyj

- PCC Group

- Siltech Corporation

- Nuscience Group

Recent Developments

July 2025 – A leading ingredients supplier launched a silicone-free, plant-based antifoaming agent tailored for clean-label food production, targeting processors in the bakery, beverage, and dairy sectors seeking natural alternatives.

April 2025 – A global chemical firm introduced an advanced food-grade antifoam emulsion with improved compatibility for high-protein and acidic systems, facilitating smoother processing in health-focused beverage lines.

March 2025 – A specialty food ingredient innovator unveiled a multifunctional defoamer combining antifoaming and emulsifying properties, aimed at simplifying production in bakery and sauce applications.

January 2025 – A niche additives provider expanded its food-grade antifoaming lineup with modular formulations optimized for high-shear industrial equipment and clean-in-place systems to boost hygiene and operational efficiency.

FAQ's

The Global Food Grade Antifoaming Agents Market is estimated to generate USD 729.2 million in revenue in 2026.

The Global Food Grade Antifoaming Agents Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.72% during the forecast period from 2026 to 2034.

The Food Grade Antifoaming Agents Market is estimated to reach USD 1076.6 million by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!