"The Food Pathogen Testing Market is valued at $ 11 billion in 2026. Further, the market is expected to grow at a CAGR of 10% to reach $ 23.5 billion by 2034."

The Food Pathogen Testing Market is gaining strong importance as food manufacturers, processors, retailers, laboratories, and foodservice operators focus on preventing contamination, protecting consumers, and maintaining brand trust. Food pathogen testing is used to detect harmful microorganisms such as Salmonella, Listeria, E. coli, Campylobacter, norovirus, and other bacteria or viruses that can cause foodborne illness. Testing is widely applied across meat and poultry, seafood, dairy, bakery, ready-to-eat foods, fresh produce, beverages, ingredients, and processed food products. Demand is supported by stricter food safety requirements, growing packaged food consumption, increasing supply-chain complexity, and greater awareness of contamination risks. Preventive food safety frameworks are also encouraging companies to identify hazards earlier rather than respond only after outbreaks occur.

Market development is being shaped by faster testing technologies, automated sample preparation, PCR-based methods, immunoassays, biosensors, next-generation sequencing, and digital laboratory information systems. Food companies are adopting pathogen testing to verify sanitation programs, validate supplier quality, support product release decisions, and reduce recall risk. Ready-to-eat foods and refrigerated products require particular attention because certain pathogens can survive or grow under challenging storage conditions. Testing demand is also rising as companies expand environmental monitoring in processing plants, especially for persistent contamination risks. However, the market faces challenges related to testing cost, sample complexity, false results, skilled labor needs, turnaround time, and method validation. Overall, food pathogen testing is becoming a core part of modern food safety management, helping companies improve compliance, protect public health, and maintain confidence in increasingly complex food supply chains.

Regional Analysis

North America Food Pathogen Testing Market

North America is a mature market for food pathogen testing, supported by strict food safety regulations, advanced laboratory infrastructure, high packaged food consumption, and strong adoption of preventive food safety systems. The United States leads regional demand across meat, poultry, dairy, seafood, fresh produce, ready-to-eat foods, beverages, and processed food categories. Testing demand is strengthened by environmental monitoring programs, supplier verification, recall prevention, and rapid pathogen detection requirements. The FDA’s Food Safety Modernization Act emphasizes prevention of contamination across the food supply chain, supporting wider use of pathogen testing and monitoring systems.

Europe Food Pathogen Testing Market

Europe is a highly regulated market, driven by strong food safety standards, established public surveillance systems, and strict controls across food production, processing, and distribution. Germany, France, the UK, Italy, Spain, the Netherlands, and Nordic countries are important demand centers due to large food processing industries and advanced testing infrastructure. Demand is particularly strong for Salmonella, Listeria, Campylobacter, E. coli, and norovirus testing. EFSA and ECDC reported that Salmonella, norovirus, and Campylobacter were among the most common identified causes of foodborne outbreaks in the EU, reinforcing the need for continued pathogen monitoring.

Asia-Pacific Food Pathogen Testing Market

Asia-Pacific is a high-growth market for food pathogen testing, supported by expanding food processing, urbanization, rising packaged food demand, export-oriented production, and stronger food safety enforcement. China, India, Japan, South Korea, Australia, Thailand, Indonesia, and Vietnam are key markets where testing demand is increasing across meat, seafood, dairy, fresh produce, beverages, and ready meals. Growing foodborne disease concerns are encouraging investment in rapid testing, laboratory networks, and quality assurance systems. WHO notes that the South-East Asia Region carries a substantial foodborne disease burden, strengthening the need for improved surveillance and testing capacity.

Middle East & Africa Food Pathogen Testing Market

The Middle East & Africa market is developing steadily, supported by food import dependence, hospitality growth, packaged food demand, halal food assurance, and public health modernization. Gulf countries are strengthening food inspection, import testing, and laboratory-based quality control, while African markets are improving food safety systems through surveillance, standards, and public-sector initiatives. Demand is rising for pathogen testing in meat, dairy, poultry, seafood, beverages, fresh produce, and processed foods. The African Union’s move to establish a continental food safety agency with a food safety data hub and rapid alert system reflects increasing regional focus on food risk management.

South & Central America Food Pathogen Testing Market

South & Central America offers growing opportunities for food pathogen testing, led by Brazil, Mexico, Argentina, Chile, Colombia, Peru, and other export-oriented food producers. Demand is supported by meat, poultry, seafood, fruit, vegetable, dairy, beverage, and processed food exports, where compliance with international buyer requirements is essential. Domestic food safety programs, retail modernization, and rising consumer awareness are also encouraging broader testing adoption. PAHO’s food safety work focuses on strengthening food control systems across the Americas and Caribbean to prevent hazards along the food value chain and reduce foodborne illnesses.

Key Insights

- Food pathogen testing demand is supported by the growing need to prevent contamination before products reach consumers. Manufacturers use testing programs to strengthen food safety systems, reduce recall exposure, and protect brand reputation.

- Salmonella, Listeria, E. coli, Campylobacter, and norovirus remain major target pathogens in food safety testing. These organisms are closely monitored because they are frequently linked with foodborne illness and high-risk food categories.

- Ready-to-eat and refrigerated foods require strong pathogen monitoring. Products consumed without further cooking need strict testing, sanitation verification, and environmental controls to reduce consumer safety risks.

- Meat, poultry, seafood, dairy, and fresh produce remain important application areas for pathogen testing. These categories require careful monitoring due to biological risk, handling complexity, and contamination sensitivity.

- Environmental monitoring is becoming a major part of food pathogen control. Testing of surfaces, equipment, drains, and processing zones helps identify contamination sources before they affect finished products.

- Rapid testing technologies are gaining adoption as food companies seek faster release decisions. PCR, immunoassay, biosensor, and automated detection systems help reduce waiting time compared with traditional culture methods.

- Laboratory automation is improving testing consistency and productivity. Automated sample handling, data capture, and reporting help laboratories manage higher testing volumes with better traceability.

- Regulatory pressure continues to strengthen the role of pathogen testing. Preventive food safety systems encourage companies to identify, monitor, and control hazards throughout production and distribution.

- False results and method validation remain important market challenges. Food companies require reliable, validated, and matrix-compatible methods to avoid unnecessary recalls or missed contamination events.

- Future growth will depend on faster, more accurate, and more integrated testing platforms. Suppliers offering reliable detection, easy workflows, digital traceability, and strong technical support are likely to gain wider acceptance.

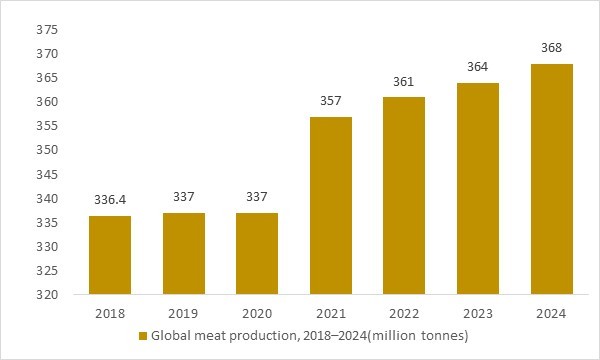

Global meat production, 2018–2024(million tonnes)

Figure: Global meat production has increased from roughly 336 million tonnes in 2018 to about 364 million tonnes in 2023 and is projected to approach 368 million tonnes in 2024e, reflecting a sustained rise in high-risk animal-origin food volumes. As more poultry, beef, pork and processed meats move through complex slaughter, cutting and further-processing chains, the number of microbiological control points and sampling events expands. OG Analysis estimates, based on international meat statistics, highlight how this growth in meat output underpins long-term demand for robust and scalable food pathogen testing solutions.

The food pathogen testing market continues to expand in line with rising global meat production, which increased from about 336 million tonnes in 2018 to nearly 364 million tonnes in 2023 and is projected to reach around 368 million tonnes in 2024e. As higher volumes of poultry, beef, pork and processed meats move through increasingly complex supply chains, processors face more critical control points requiring microbiological verification. Stricter regulatory frameworks and growing retailer quality expectations further elevate the need for rapid, reliable pathogen detection across slaughter, deboning, RTE, and export-oriented facilities. Together, these trends strengthen long-term demand for high-throughput pathogen testing technologies and automation solutions.

Market Scope

| Parameter | Food Pathogen Testing Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- E.coli

- Salmonella

- Listeria

- Other Pathogens

By Technology

- Traditional

- Rapid

- Immunoassay

- Convenience Based

- PCR

- Other Technologies

By Application

- Meat And Poultry

- Fruits And Vegetables

- Dairy

- Other Applications

By Sales Channel

- OEM

- Aftermarket

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Bureau Veritas SA

- Lloyd’s Register Quality Assurance Limited

- Intertek Group plc

- Asurequality Ltd.

- Genevac Ltd.

- Thermo Fisher Scientific Inc.

- Bio-Rad Laboratories Inc.

- Merck Co. & KGaA

- Neogen Corporation

- bioMerieux SA

- Agilent Technologies Inc.

- Qiagen NV

- Shimadzu Corporation

- SGS Société Générale de Surveillance SA

- Genetic Id Na Inc.

- RapidBio Systems Inc.

- Mérieux NutriSciences Corp.

- FoodChain ID Inc.

- Ring Biotechnology Co. Ltd.

- Genon Laboratories Ltd.

- PerkinElmer Inc.

- Randox Food Diagnostics Ltd.

- Omega Diagnostics Group plc

- Romer Labs Inc.

- Eurofins Scientific SE

- Charm Sciences Inc.

- Hygiena LLC

- MilliporeSigma

- Hardy Diagnostics

- Luminex Corporation

Recent Developments

June 2026: FDA initiated an outbreak investigation of Listeria monocytogenes linked to recalled soft ricotta/requeson cheese. The development reinforces demand for Listeria testing, environmental monitoring, sanitation verification, and rapid response systems in dairy and ready-to-eat food facilities.

May 2026: FDA listed recalls of food products associated with powdered milk from California Dairies Inc. due to potential Salmonella risk. This highlights the continued need for pathogen testing in dairy ingredients, dry powders, and multi-product downstream food supply chains.

April 2026: FDA and CDC concluded an investigation into an E. coli O157:H7 outbreak linked to RAW FARM-brand raw dairy products. FDA reported onsite inspections, sample collections, pathogen analysis, and whole-genome sequencing, showing the growing role of advanced molecular testing in outbreak traceability.

April 2026: FDA updated GenomeTrakr fast facts, identifying GenomeTrakr as a distributed laboratory network using whole-genome sequencing for pathogen identification. This supports wider adoption of genomic surveillance for foodborne pathogen detection, source tracking, and outbreak investigation.

March 2026: Tirumala Tirupati Devasthanams inaugurated a state-of-the-art food testing laboratory with FSSAI support. The lab includes advanced chemical and microbiological testing capabilities, electronic nose and tongue systems, and on-site analysis tools for food quality and safety monitoring.

February 2026: Haryana approved major upgrades to food and drug safety infrastructure, including mobile food testing laboratories, microbiology sections, modern equipment procurement, and additional state-level laboratory capacity. This reflects growing public-sector investment in faster and more accessible pathogen and microbial testing.

January 2026: USDA-FSIS issued Notice 08-26 on testing for non-Listeria monocytogenes Listeria species. The notice follows FSIS’ expanded laboratory approach that includes broader Listeria species testing in ready-to-eat food production environments.

December 2025: USDA-FSIS opened discussion on practical strategies to reduce Salmonella in poultry products after withdrawing its earlier proposed Salmonella framework. The agency continued focus on microbial monitoring, statistical process control, and final-product safety approaches, supporting long-term testing demand in poultry.

February 2025: Mérieux NutriSciences completed the acquisition of Bureau Veritas’ food testing activities in Japan, Morocco, Southeast Asia, and South Africa. The move expanded its global food safety, quality, and testing service footprint.

FAQ's

The Food Pathogen Testing Market is estimated to reach USD 23.5 billion by 2034.

The Global Food Pathogen Testing Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 10% during the forecast period from 2025 to 2034.

The Global Food Pathogen Testing Market is estimated to generate USD 11 billion in revenue in 2026.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!