"The Forklift Truck Market was valued at $ 62.3 billion in 2025 and is projected to reach $ 132.7 billion by 2034, growing at a CAGR of 8.8%."

Forklift Truck Market Overview

The Forklift Truck Market is witnessing steady growth, driven by increasing demand for efficient material handling solutions across industries such as logistics, manufacturing, construction, and retail. Forklift trucks play a vital role in warehouse operations, distribution centers, and industrial facilities, ensuring seamless movement of goods and improving operational efficiency. The growing emphasis on automation, supply chain optimization, and e-commerce expansion has further accelerated the adoption of advanced forklift technologies. The shift towards electric and hydrogen-powered forklifts is gaining momentum, as companies seek sustainable and cost-effective alternatives to traditional internal combustion (IC) engine forklifts. Additionally, the integration of smart technologies such as IoT connectivity, telematics, and AI-driven fleet management systems is enhancing productivity, safety, and predictive maintenance. With continuous investments in warehouse automation and infrastructure development, the market is poised for long-term expansion.

The Forklift Truck Market has seen significant developments, particularly in electrification and automation. The rising adoption of electric forklifts is being fueled by stricter emissions regulations and corporate sustainability goals, pushing manufacturers to expand their electric vehicle (EV) lineup with improved battery efficiency and faster charging capabilities. The demand for autonomous and semi-autonomous forklifts has also surged, especially in large-scale warehouses and fulfillment centers, where robotics and AI-driven navigation systems are enhancing efficiency. Additionally, the growing popularity of lithium-ion battery-powered forklifts has led to a shift away from lead-acid batteries, as companies prioritize longer battery life and lower maintenance costs. The construction and manufacturing sectors have also contributed to market growth, with increased investments in infrastructure projects driving demand for heavy-duty forklifts. However, supply chain disruptions, rising raw material costs, and semiconductor shortages have posed challenges, impacting production timelines and equipment availability.

The Forklift Truck Market is expected to witness further advancements in automation, energy efficiency, and fleet management technologies. The development of hydrogen fuel cell forklifts is projected to gain traction, offering a zero-emission alternative with faster refueling times compared to battery-electric models. AI-driven predictive maintenance and IoT-enabled real-time monitoring will continue to shape the market, allowing businesses to optimize fleet utilization and reduce operational downtime. Additionally, the adoption of collaborative robotics in material handling will enhance workplace safety and efficiency, as companies integrate automated guided vehicles (AGVs) with traditional forklifts. The expansion of smart warehouses and last-mile logistics hubs will further drive the need for agile and connected forklift solutions. Emerging markets in Asia-Pacific and Latin America are set to become key growth areas, fueled by rapid industrialization, urbanization, and investments in logistics infrastructure. With continuous innovation and regulatory support for cleaner and smarter forklift technologies, the industry is poised for dynamic transformation in the years ahead.

Key Insights_ Forklift Truck Market

-

Electric forklifts are experiencing rapid growth as companies shift toward zero-emission fleets. These vehicles offer lower operating costs, reduced maintenance needs, and quieter operation, making them ideal for indoor environments such as warehouses, retail distribution centers, and food processing facilities.

-

Automation is reshaping forklift operations with the introduction of autonomous forklifts and AGVs capable of navigating warehouse environments without human intervention. These machines enhance safety, reduce labor dependency, and improve inventory handling accuracy in high-throughput logistics hubs.

-

Lithium-ion battery technology is gaining momentum in the forklift segment due to its fast-charging capabilities, longer lifecycle, and minimal maintenance. It enables greater operational uptime and supports multi-shift operations without the need for frequent battery replacements.

-

The demand for forklifts with advanced telematics is growing, allowing fleet managers to track performance metrics, conduct predictive maintenance, and optimize equipment usage. These features contribute to lower downtime and greater efficiency in complex supply chain environments.

-

Rough terrain forklifts are in high demand in construction, mining, and agriculture due to their ability to operate in challenging outdoor environments. These machines are designed for high load capacity, stability, and mobility over uneven or rugged terrain.

-

The rise of cold chain logistics and pharmaceutical warehousing has increased the need for forklifts capable of operating in temperature-controlled environments. Manufacturers are offering models with corrosion-resistant components and high-efficiency thermal insulation features.

-

Asia Pacific continues to lead forklift production and consumption, driven by the expansion of manufacturing hubs, infrastructure development, and rising intra-regional trade. Local manufacturers are scaling production with cost-effective models tailored to domestic and export markets.

-

Warehouse automation trends are pushing demand for compact, narrow-aisle forklifts that maximize vertical storage and navigate tight spaces efficiently. These models are ideal for e-commerce and retail warehousing where SKU density is high.

-

Government subsidies and regulatory support for clean energy adoption are encouraging businesses to replace internal combustion forklifts with electric alternatives. Incentives include tax credits, fleet modernization grants, and emissions-related regulatory exemptions.

-

Manufacturers are focusing on ergonomic design improvements, including enhanced visibility, intuitive controls, and vibration-dampening operator cabins. These upgrades aim to reduce operator fatigue, improve safety, and boost productivity during long working shifts.

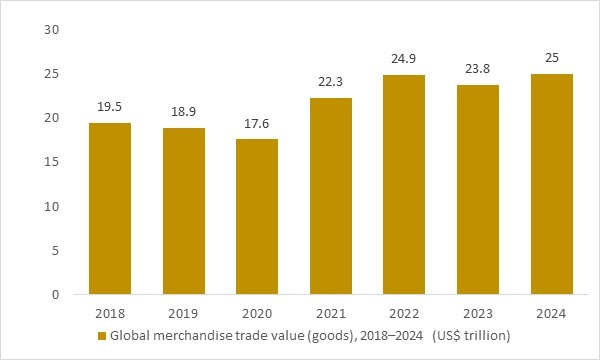

Global merchandise trade value (goods), 2018–2024 (US$ trillion)

Figure: Global merchandise trade value for goods has grown from roughly US$ 19–20 trillion in 2018 to around US$ 25 trillion by 2024, despite the temporary disruption in 2020. This resilient expansion in cross-border goods flows increases throughput at ports, warehouses and distribution centers worldwide. OG Analysis estimates, derived from leading international trade statistics, underline how sustained trade activity directly drives forklift truck utilisation, fleet renewal and new investments across global logistics networks.Global merchandise trade value (goods), 2018–2024. Rising trade volumes underpin logistics and warehouse activity that drives the global forklift truck market.

- Global merchandise trade value has shown a resilient upward trajectory from 2018 to 2024, reinforcing the scale and intensity of global logistics operations. As goods movement expands, warehouses, ports, and distribution centers face higher throughput, directly increasing demand for efficient material-handling equipment. This sustained trade activity underpins growth opportunities in the global forklift truck market, driving fleet expansion, modernization, and adoption of advanced electric and automation-ready models.

Market Scope

| Parameter | Forklift Truck Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Application, By End User and By Technology |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Forklift Truck Market Segmentation

By Product Type

- Counterbalance

- Warehouse

By Technology

- Electric Power

- Internal Combustion Engine

By Class

- Class I

- Class II

- Class III

- Class IV

- Class V

By End-User

- Retail and Wholesale

- Logistics

- Automotive

- Food Industry

- Other End Users

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Major Companies Analysed

Anhui HELI Co. Ltd., Crown Equipment Corporation, Godrej & Boyce Mfg. Co. Ltd., Hangcha Group Co. Ltd., Hyster-Yale Materials Handling Inc., Jungheinrich AG, Kion Group AG, Komatsu Ltd., Mitsubishi Logisnext Co. Ltd., Toyota Industries Corporation, Clark Material Handling Company, Combilift Ltd, Doosan Industrial Vehicle, EP Equipment, Hyundai Heavy Industries Co. Ltd, Lift Technologies Inc, Linde Material Handling, Lonking Machinery Co. Ltd., The Raymond Corporation, UniCarriers Americas Corporation., Manitou Group, Tailift Group, LiuGong Machinery Corporation, Lonking Holdings Limited, EP Equipment Co. Ltd., Hubtex Maschinenbau GmbH & Co. KG, Hangzhou UN Forklift Co. Ltd., Paletrans Equipamentos Ltda

Recent Developments

- July 2025 – Hyster‑Yale announced a strategic business realignment that consolidates its battery and charger programs, aiming to launch its HydroCharge™ mobile charging platform and accelerate sales of battery and fuel‑cell electric port equipment in the second half of 2025.

- May 2025 – Mitsubishi Logisnext Americas expanded its Houston manufacturing campus with a 73,500‑square‑foot electrification fabrication building to enhance production of its electric Class I and II forklifts, improving capacity and efficiency.

- April 2025 – Toyota Material Handling Europe partnered with Plug Power and STEF to deploy hydrogen fuel cell–ready forklifts and a green hydrogen infrastructure across STEF’s cold‑storage facilities in France and Spain, supporting its Moving Green climate initiative.

- March 2025 – Bobcat unveiled an array of new lithium‑ion battery systems and a new series of 3‑wheel counterbalance forklifts at LogiMAT 2025, introducing upgraded warehouse equipment with improved energy efficiency and fast charging.

- March 2025 – At Spring 2025 launches, Toyota introduced integrated mid‑ and large‑electric pneumatic forklifts with built‑in lithium‑ion batteries, alongside an enhanced Core Electric Forklift model offering greater runtime, ergonomics, and customization.

- January 2025 – Toyota Material Handling integrated with The Raymond Corporation to form Toyota Material Handling North America, consolidating operations under one leadership while maintaining both brand identities to better serve customers.

FAQ's

The Global Forklift Truck Market is estimated to generate USD 62.3 billion in revenue in 2025.

The Global Forklift Truck Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 8.77% during the forecast period from 2025 to 2034.

The Forklift Truck Market is estimated to reach USD 132.7 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!