"The Frozen Freeze Dried Pet Foods Market was valued at $90.52 billion in 2025 and is projected to reach $202 billion by 2034, growing at a CAGR of 9.33%."

The frozen freeze-dried pet foods market sits within the premium and super-premium segment of pet nutrition, combining raw-inspired positioning with the practicality of long shelf life and portion control. Freeze-drying removes moisture at low temperatures to preserve ingredient structure, aroma, and nutrient integrity, making it attractive for pet owners seeking minimally processed, high-protein diets. Product formats include complete-and-balanced freeze-dried meals, patties and nuggets, mixers and toppers used to enhance kibble, single-ingredient treats, and functional recipes targeting digestion, skin and coat, mobility, or weight management. Core end uses are dogs and cats, with demand concentrated in adult maintenance and life-stage nutrition, but also expanding into puppy/kitten formulas and veterinary-adjacent “limited ingredient” and sensitive-stomach offerings. Distribution is strongest through specialty pet retail, premium e-commerce, and select veterinary and boutique channels where education-driven selling supports trade-up behavior and repeat purchases.

Market momentum is driven by pet humanization, willingness to pay for perceived quality, and growing skepticism toward heavily processed diets. Key trends include “raw feeding made easy” messaging, higher transparency around sourcing and traceability, expanded use of novel proteins, organ meats, and functional inclusions such as probiotics, omega-rich ingredients, and superfoods, and cleaner labels with fewer fillers. Brands are also innovating in convenience, offering smaller bite formats, resealable packaging, and feeding guides that simplify hydration and reconstitution. Another major trend is regulatory and safety emphasis, pushing tighter microbial controls, validated kill steps, and robust quality assurance as raw-inspired products face higher scrutiny. Competitive dynamics include established premium pet food companies, specialist freeze-dried brands, and vertically integrated manufacturers; differentiation centers on ingredient quality, palatability, digestibility outcomes, nutritional completeness, safety systems, brand trust, and omnichannel reach. Looking ahead, the category is expected to broaden beyond niche enthusiasts as more owners adopt topper-plus-kibble routines and as brands balance premium positioning with improved affordability through scalable manufacturing and wider retail penetration.

Key Market Insights

-

Pet humanization and premiumization remain the structural growth driver (historic → current → future) Owners have steadily shifted from basic feeding to “family member” nutrition expectations. Today, purchasing decisions mirror human food trends like clean labels, high protein, and functional benefits. Freeze-dried fits this premium narrative by signaling minimal processing and quality ingredients. Future growth will be reinforced by wellness-oriented spending, especially for dogs and cats in urban households. Brand storytelling and trust remain central to trade-up behavior.

-

Freeze-drying technology advantage supports nutrient and palatability claims Unlike high-heat processes, freeze-drying preserves aroma and ingredient structure, supporting strong palatability in many recipes. Current success is linked to patties, nuggets, and morsels that rehydrate well and feel “fresh” to owners. Future product development will focus on improving texture, faster rehydration, and consistent batch performance. Processing control and moisture targets remain critical for shelf stability. Technical capability becomes a competitive differentiator, not just marketing.

-

Mixers, toppers, and “kibble complement” use cases are expanding fastest Historically, freeze-dried was positioned as a complete raw alternative for niche buyers. Today, many households use it as a topper to upgrade kibble without changing the whole diet. This broadens the addressable base and improves trial rates through smaller pack sizes. Future growth will likely be driven by hybrid feeding routines and subscription replenishment. Top-performing segments include toppers, meal mixers, and functional add-ins. Education on portioning and rehydration supports repeat purchase.

-

Protein differentiation and novel proteins shape premium shelf space Standard chicken and beef remain high-volume, but competition pushes brands toward limited-ingredient and novel proteins. Current offerings increasingly feature lamb, turkey, duck, venison, rabbit, and fish, often paired with organ meats for nutrient density. Future expansion may emphasize rotational feeding and allergy management positioning. Supply reliability and traceability of proteins become more important as portfolios widen. Palatability and stool quality remain key consumer-perceived performance indicators.

-

Functional nutrition and life-stage targeting deepen category maturity The market is moving from “raw-inspired” to “purpose-built” nutrition with functional benefits. Current launches emphasize digestion support, skin and coat, mobility, immune support, and weight management through targeted inclusions. Future innovation will refine condition-specific recipes and supplement-like topper concepts. Growth is supported by aging pet populations and owner focus on preventative health. Clear claims and visible ingredients drive perceived value.

-

Food safety scrutiny and quality systems influence brand trust and retailer acceptance Raw-inspired positioning raises heightened attention to pathogen control and manufacturing hygiene. Current market leaders invest in validated interventions, testing protocols, and supply chain controls to protect brand credibility. Future regulatory and retailer requirements are likely to tighten, increasing barriers for smaller or inconsistent producers. Transparent safety communication becomes part of the purchase decision. Recalls or safety incidents can rapidly shift consumer loyalty in this premium segment.

-

Cost and affordability shape how the category scales beyond early adopters Freeze-dried remains premium due to ingredient intensity and processing costs, historically limiting penetration. Current growth strategies include smaller trial packs, topper formats, and multi-buy promotions that lower entry barriers. Future scaling may rely on manufacturing efficiency, improved yields, and wider distribution without diluting quality perception. Brands that balance premium cues with practical feeding economics win mainstream households. Subscription and loyalty programs can soften price sensitivity.

-

E-commerce and specialty retail remain the core channels, with omnichannel expansion rising Specialty stores historically built the category through education and sampling. Today, e-commerce accelerates discovery, repeat ordering, and access to niche brands and protein varieties. Future growth will come from stronger omnichannel execution, including mass-premium placements and clinic-adjacent recommendations. Digital content, reviews, and feeding calculators influence conversion. Retail training and merchandising remain important to explain usage and justify price.

-

Packaging innovation supports freshness, convenience, and portion control Resealable pouches, single-serve packs, and multi-format assortments reduce waste and improve household adoption. Current buyers value easy storage, less mess, and clear feeding guides for rehydration. Future packaging will emphasize sustainability cues while protecting moisture barrier performance. Portionable nuggets and crumbles perform well for topper use. Packaging quality is tightly tied to perceived product quality in premium pet food.

-

Competitive landscape intensifies through consolidation and portfolio broadening The category began with specialist brands; today it attracts larger pet food players and vertically integrated manufacturers. Current competition centers on ingredient sourcing, formulation credibility, palatability, and safety systems, alongside marketing reach. Future differentiation will rely on scientific validation, consistent supply, and innovation cadence across proteins and functional claims. Partnerships with retailers and co-manufacturers shape capacity and availability. Brand trust, more than sheer assortment, becomes the key long-term moat.

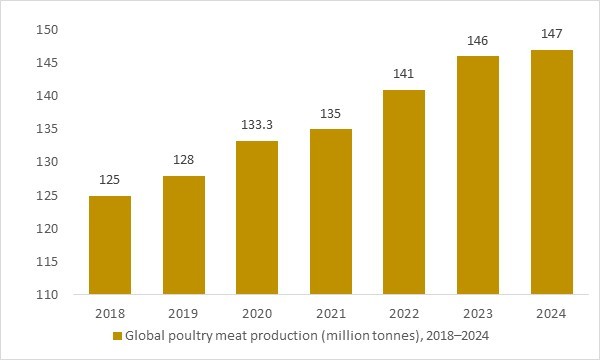

Global poultry meat production (million tonnes), 2018–2024

Figure:Global poultry meat production (million tonnes), 2018–2024 – a key raw material indicator for the global frozen and freeze dried pet foods market.

- Global poultry meat production has continuously expanded from 2018 to 2024, providing a solid raw-material foundation for the growth of the frozen and freeze dried pet foods market. As poultry remains the leading animal protein used in premium pet nutrition, this rising supply supports manufacturers in developing high-protein, minimally processed diets that appeal to pet owners seeking natural and nutritionally rich feeding options, ultimately driving positive market outlook and investment interest.

Regional Insights

North America

North America’s frozen freeze-dried pet foods market is propelled by strong pet ownership, premiumization in pet nutrition, and rising consumer focus on high-quality, minimally processed diets that support digestive health and longevity. Market dynamics emphasize clean label ingredients, high protein content, and nutrient retention achieved through freeze-drying, appealing to pet owners who treat pets as family members. Lucrative opportunities are strongest in online and direct-to-consumer channels, subscription models, and premium product lines targeting specific life stages or dietary sensitivities. Latest trends include expanded flavor and functional ingredient offerings, eco-friendly packaging, and collaboration with veterinarians and animal nutritionists to validate product claims. The outlook remains positive as demand for human-grade and specialist pet foods grows, with recent developments focused on expanded production capabilities, enhanced supply chain efficiencies, and stronger brand community engagement.

Asia Pacific

Asia Pacific is experiencing rapid growth in the frozen freeze-dried pet foods market due to rising pet ownership in urban centers, increasing disposable incomes, and growing awareness of pet health and wellness. Market dynamics prioritize affordable premiumization, localized flavors, and distribution through e-commerce platforms catering to younger, digitally active consumers. Lucrative opportunities lie in expanding middle-class demand, pet specialty retail growth, and crossover interest in human-grade pet nutrition trends. Trends include adoption of traditional and regional protein sources, branding aligned with holistic pet care, and partnerships with veterinary clinics to drive consumer confidence. The forecast remains robust as pet populations expand and premium niche categories gain traction, with recent developments centered on new product launches, strategic market entries by global players, and tailored nutrition solutions.

Europe

Europe’s frozen freeze-dried pet foods market is shaped by high pet care standards, mature retail infrastructure, and strong demand for sustainable and natural products. Market dynamics emphasize ingredient transparency, environmental certifications, and packaging sustainability, alongside performance attributes like digestibility and bioavailability. Lucrative opportunities are concentrated in organic and functional pet foods, specialized diets for aging pets, and differentiation through traceable protein sourcing. Latest trends include growth in eco-conscious formulations, reduced food waste messaging, and integration of novel nutrition concepts based on human food trends. The outlook is steady and innovation-driven as consumer expectations rise, with recent developments focusing on expanded product portfolios, enhanced quality assurances, and closer engagement with animal nutrition experts.

Middle East & Africa

Middle East & Africa’s frozen freeze-dried pet foods market is emerging, supported by increasing pet ownership, growth in premium pet care awareness, and expanding retail networks. Market dynamics emphasize affordability balanced with quality, accessibility through boutique pet stores and digital channels, and introduction of international brands. Lucrative opportunities exist in urban pet communities, expatriate markets, and premium segments seeking differentiated nutrition. Trends include rising social media influence on pet food preferences, gradual expansion of supply chains, and localized marketing strategies. The outlook improves as infrastructure and consumer confidence grow, with recent developments centered on new importer partnerships, targeted promotions, and increased availability of specialized pet nutrition.

South & Central America

South & Central America’s frozen freeze-dried pet foods market benefits from expanding middle-class pet ownership, evolving nutrition awareness, and growing interest in premium diet formats. Market dynamics highlight cost-performance balance, broadening availability through retail and online platforms, and inclusion of local ingredients adapted to regional tastes. Lucrative opportunities exist in subscription models, veterinary-endorsed products, and brand loyalty programs. Latest trends include increased pet influencer marketing, inclusion of functional supplements, and rollout of value-oriented premium product tiers. The outlook remains steadily positive as pet care spending grows, with recent developments focused on distribution expansion, educational campaigns on nutrition benefits, and strategic alliances with distributors and pet specialty retailers.

Report Scope

| Parameter | Frozen Freeze Dried Pet Foods Market Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Diagnostic Method, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Frozen Freeze Dried Pet Foods Market Segments Covered In The Report

By Product

- Frozen Pet Food

- Freeze-Dried Pet Food

By Source

- Synthetic

- Plant-Based

- Animal-Based

By Pet Type

- Dog

- Cat

- Fish

- Other Pet Types

By Distribution Channel

- Supermarkets Or Hypermarkets

- Specialty Pet Stores

- Online

- Other Distribution Channels

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Companies Covered

- Mars Inc.

- Merrick Pet Care

- Stella & Chewy's LLC

- WellPet

- Ziwi Peak

- Nature's Variety

- L Catterton

- Primal Pet Foods Inc.

- Nutro Co.

- Bravo Pet Foods

- Carnivore Meat Company LLC

- Deuerer

- Natura Pet Products Inc.

- NRG Dog Products

- Canvasback Pet Supplies

- Steve's Real Food

- Kelly & Company

- Grandma Lucy's

- Harmony House

- K9 Natural Ltd.

- Vital Essentials

Recent Industry Developments

-

Nov 2025 – Shepherd Boy Farms: Announced a $50M investment to build a new 100,000 sq. ft. production facility in Indiana to significantly expand output. The expansion is aimed at scaling freeze-dried pet food capacity and strengthening manufacturing resilience.

-

Oct 2025 – Foodynamics: Initiated a recall of select freeze-dried pet treats due to potential Salmonella contamination risk. The action intensified retailer and brand focus on pathogen controls, supplier audits, and finished-product testing in freeze-dried formats.

-

Aug 2025 – Glacial Freeze Dry: Announced the acquisition of Foodynamics, combining two freeze-dried co-manufacturing platforms. The deal is designed to expand contract manufacturing capacity and improve responsiveness for pet food and treat brands.

-

Aug 2025 – Formula Raw: Opened a new 15,000 sq. ft. manufacturing facility in Montreal to ramp production, with the company stating it can quadruple freeze-dried output. The upgrade supports broader distribution plans, including increased readiness for U.S. market expansion.

-

Mar 2025 – Nutriment (TNC): Continued consolidation in premium raw/frozen categories through acquisitions (raw pet food processors and natural treats), strengthening its production footprint and brand portfolio. The activity reflects scale-building as demand concentrates among larger multi-brand platforms.

-

2024–2025 – Multiple premium brands: Accelerated launches of limited-ingredient, novel-protein, and functional “raw topper” freeze-dried lines, targeting higher digestibility and “clean label” positioning. This product mix shift is increasingly paired with tighter claims substantiation and batch traceability expectations.

What You Receive

• Global Frozen Freeze Dried Pet Foods market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Frozen Freeze Dried Pet Foods.

• Frozen Freeze Dried Pet Foods market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Frozen Freeze Dried Pet Foods market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Frozen Freeze Dried Pet Foods market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Frozen Freeze Dried Pet Foods market, Frozen Freeze Dried Pet Foods supply chain analysis.

• Frozen Freeze Dried Pet Foods trade analysis, Frozen Freeze Dried Pet Foods market price analysis, Frozen Freeze Dried Pet Foods Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Frozen Freeze Dried Pet Foods market news and developments.

The Frozen Freeze Dried Pet Foods Market international scenario is well established in the report with separate chapters on North America Frozen Freeze Dried Pet Foods Market, Europe Frozen Freeze Dried Pet Foods Market, Asia-Pacific Frozen Freeze Dried Pet Foods Market, Middle East and Africa Frozen Freeze Dried Pet Foods Market, and South and Central America Frozen Freeze Dried Pet Foods Markets. These sections further fragment the regional Frozen Freeze Dried Pet Foods market by type, application, end-user, and country.

FAQ's

The Global Frozen Freeze Dried Pet Foods Market is estimated to generate USD 90.52 billion in revenue in 2025.

The Global Frozen Freeze Dried Pet Foods Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.33% during the forecast period from 2025 to 2034.

The Frozen Freeze Dried Pet Foods Market is estimated to reach USD 202 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!