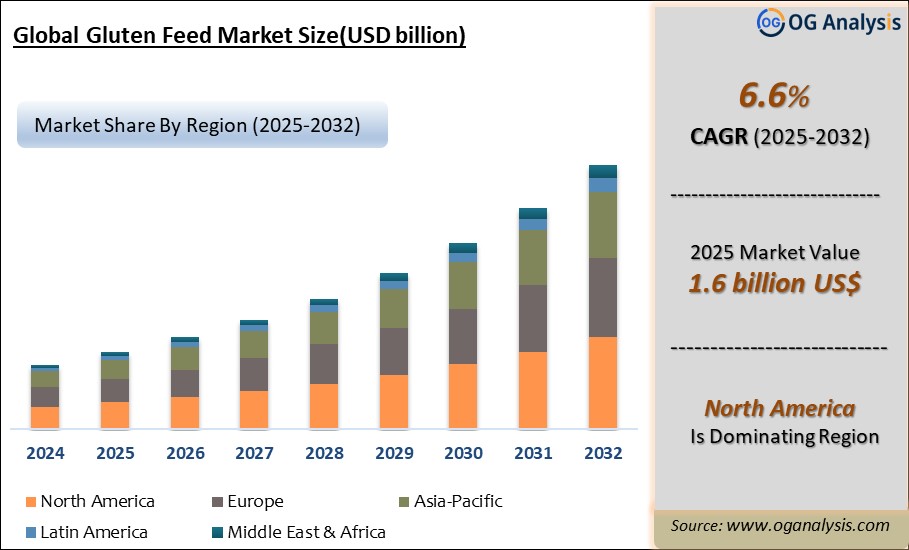

"Global Gluten Feed Market is valued at USD 1.6 billion in 2025. Further, the market is expected to grow at a CAGR of 6.6% to reach USD 2.8 billion by 2034."

The gluten feed market is witnessing steady growth as it serves as an effective, protein-rich livestock feed derived mainly as a by-product from corn wet milling processes. It contains moderate protein and high fiber content, making it suitable for dairy cattle, beef cattle, swine, and poultry. Growing demand for cost-effective and nutrient-rich animal feed, especially in North America, Europe, and emerging Asian markets, is driving the adoption of gluten feed. Furthermore, with corn processing industries expanding and livestock production intensifying globally, manufacturers are strengthening distribution networks and strategic partnerships to ensure consistent feed supply and price competitiveness in the market.

The market is also benefiting from increasing focus on enhancing feed efficiency, animal weight gain, and milk yield through balanced rations containing gluten feed. However, competition from alternative feed products such as corn gluten meal and DDGS, alongside volatility in corn prices, poses challenges to market growth. Leading players are investing in production optimization, tailored product blends, and expansion into Asian markets to tap the rising feed demand. Sustainability considerations in livestock feed formulations and supply chains are also influencing product development and marketing strategies to align with global protein security and climate goals.

By Source:

The largest segment is the Corn segment. Corn-based gluten feed dominates the market as it is widely produced as a by-product of corn wet milling, offering high availability, cost-effectiveness, and balanced nutritional profiles that meet the protein and energy requirements of cattle and other livestock efficiently.

By Nature:

The fastest growing segment is the Organic segment. Growth is driven by rising consumer demand for organic meat and dairy products, encouraging livestock producers to include organic-certified feed ingredients such as organic gluten feed in rations to comply with organic livestock farming standards and premium market positioning.

Key Insights

- Gluten feed demand is increasing due to its affordability and balanced nutrient profile, making it a popular choice for beef and dairy cattle feed formulations in North America and Europe, supporting feedlot profitability and dairy productivity.

- Asia Pacific is emerging as a significant growth region for gluten feed, driven by the rising livestock population, feed manufacturing expansions, and demand for cost-effective protein feed ingredients for intensive farming systems.

- Leading manufacturers are strengthening partnerships with feed millers, distributors, and livestock integrators to expand market access, enhance service networks, and ensure competitive pricing amidst feed cost pressures.

- Volatility in corn prices affects gluten feed production costs, impacting feed manufacturers’ margins and pricing strategies, prompting companies to focus on production efficiency and raw material sourcing optimization.

- The dairy segment remains a major consumer of gluten feed due to its high fiber and digestible protein content, improving rumen health and milk yield when included in balanced rations.

- Innovation in blended feed products combining gluten feed with other energy and protein sources is gaining traction to address nutrient variability and optimize feed conversion ratios across livestock categories.

- Environmental sustainability considerations are shaping feed formulation strategies, with gluten feed serving as an upcycled by-product, contributing to resource efficiency and circular economy goals in agriculture.

- Export opportunities are expanding for major producers in the US and Europe due to growing demand in Southeast Asia and Latin America, supported by trade facilitation and rising livestock feed imports.

- Gluten feed’s market competitiveness is challenged by alternative feed products such as corn gluten meal, soybean meal, and DDGS, requiring strategic pricing, quality consistency, and value communication to sustain demand.

- Key players in the market include Archer Daniels Midland, Cargill, Ingredion, Tate & Lyle, and Roquette, focusing on expanding production capacities, developing customized feed solutions, and strengthening international market footprints.

Reort Scope

| Parameter | Detail |

|---|---|

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Source, By Nature, By Application |

| Countries Covered | North America (USA, Canada, Mexico) Europe (Germany, UK, France, Spain, Italy, Rest of Europe) Asia-Pacific (China, India, Japan, Australia, Rest of APAC) The Middle East and Africa (Middle East, Africa) South and Central America (Brazil, Argentina, Rest of SCA) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10 % free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Datafile |

Market Segmentation

By Source

- Wheat

- Corn

- Barley

- Rye

- Maize

- Other Sources

By Nature

- Organic

- Conventional

By Application

- Swine

- Poultry

- Cattle

- Aquaculture

- Equine

- Pet Animals

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Ingredion Incorporated

- Archer Daniels Midland Company

- Cargill Incorporated

- Tate & Lyle plc

- Bunge Ltd.

- Grain Processing Corporation

- The Roquette Group

- Tereos Syral

- Commodity Specialists Company

- Agrana Group

- Nutreco N.V.

- Amy’s Kitchen Inc.

- Bob’s Red Mill Natural Foods

- Agrium Inc.

- Charoen Pokphand Group Co. Ltd.

- JBT Corporation

- Markel Food Group

- Felleskjøpet Rogaland Agder

- Parrheim Foods

- Puris Foods

- Erica Record LLC

- Emsland Group

- Louis Dreyfus Company B.V.

- Conagra grain processing LLC

- Associated British foods plc

- Sunrise Commodities Limited

- CHS inc.

- Agrisol

- Glanbia plc

- United Cooperative Grain Growers

What You Receive

• Global Gluten Feed market size and growth projections (CAGR), 2024- 2034• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Gluten Feed.

• Gluten Feed market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Gluten Feed market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Gluten Feed market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Gluten Feed market, Gluten Feed supply chain analysis.

• Gluten Feed trade analysis, Gluten Feed market price analysis, Gluten Feed Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Gluten Feed market news and developments.

The Gluten Feed Market international scenario is well established in the report with separate chapters on North America Gluten Feed Market, Europe Gluten Feed Market, Asia-Pacific Gluten Feed Market, Middle East and Africa Gluten Feed Market, and South and Central America Gluten Feed Markets. These sections further fragment the regional Gluten Feed market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways1. The report provides 2024 Gluten Feed market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Gluten Feed market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Gluten Feed market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Gluten Feed business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Gluten Feed Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Gluten Feed Pricing and Margins Across the Supply Chain, Gluten Feed Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Gluten Feed market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

FAQ's

The Global Gluten Feed Market is estimated to generate USD 1.6 billion in revenue in 2025.

The Global Gluten Feed Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.6% during the forecast period from 2025 to 2034.

The Gluten Feed Market is estimated to reach USD 2.8 billion by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!