"The Hollow Glass Beads Market Size is valued at $1.82 Billion in 2025. Worldwide sales of Hollow Glass Beads Market are expected to grow at a significant CAGR of 4.1%, reaching $2.41 Billion by the end of the forecast period in 2032."

The Hollow Glass Beads Market has emerged as a versatile and rapidly expanding segment across multiple industries, thanks to the unique properties of these lightweight, high-strength microspheres. Hollow glass beads are widely utilized for their low density, thermal insulation, and chemical stability, making them a go-to additive in construction materials, automotive components, paints and coatings, and even aerospace composites. Their spherical shape offers improved flow and reduced viscosity in formulations, translating to cost-effective material usage and enhanced mechanical properties. As sustainability gains ground, hollow glass beads are increasingly being viewed as a solution to reduce the overall weight of end products, contributing to lower emissions and fuel consumption, especially in transportation and infrastructure applications.

Looking ahead, the market is positioned for steady advancement as industries prioritize material innovation, energy efficiency, and lightweighting. In 2025 and beyond, the demand for hollow glass beads is expected to grow in tandem with trends in green construction, electric vehicles, and advanced composites manufacturing. Developments in surface treatment and functional coatings are enhancing their compatibility with polymers, adhesives, and resins. Moreover, the focus on circular economy and eco-design is pushing manufacturers to optimize bead production processes for minimal environmental impact. The Asia-Pacific region, with its strong industrial output and growing R&D ecosystem, is expected to be a key growth hub. As regulations tighten and performance standards rise, companies are investing in proprietary bead technologies and strategic partnerships to expand their reach in specialized applications such as deepwater drilling, military-grade coatings, and next-gen consumer electronics.

Trade Intelligence Hollow Glass Beads Market

| Global Glass microspheres <= 1 mm in diameter , Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 363.9 | 430.9 | 444.5 | 447.4 | 439.0 |

| China | 48.3 | 62.3 | 51.9 | 46.2 | 53.4 |

| South Korea | 33.1 | 40.3 | 37.3 | 35.4 | 45.1 |

| United States of America | 36.6 | 27.1 | 30.0 | 31.6 | 30.7 |

| Germany | 29.3 | 35.1 | 33.0 | 35.9 | 27.7 |

| United Kingdom | 18.5 | 27.6 | 31.0 | 31.2 | 26.1 |

| Source: OGAnalysis, International Trade Centre (ITC) | |||||

- China , South Korea, United States of America , Germany and United Kingdom are the top five countries importing 41.7% of global Glass microspheres <= 1 mm in diameter in 2024

- Global Glass microspheres <= 1 mm in diameter Imports increased by 20.6% between 2020 and 2024

- China accounts for 12.2% of global Glass microspheres <= 1 mm in diameter trade in 2024

- South Korea accounts for 10.3% of global Glass microspheres <= 1 mm in diameter trade in 2024

- United States of America accounts for 7% of global Glass microspheres <= 1 mm in diameter trade in 2024

| Global Glass microspheres <= 1 mm in diameter Export Prices, USD/Ton, 2020-24 |

| |

| Source: OGAnalysis, International Trade Centre (ITC) |

Key Insights

- Historically, hollow glass beads evolved from simple fillers into high-performance functional additives as manufacturing processes improved shell strength, uniformity, and size control. This evolution transformed them from specialty curiosities into mainstream ingredients in weight-sensitive composites and coatings.

- Lightweighting is the single most important driver, as hollow glass beads reduce part density without requiring major redesigns or capital changes. They allow formulators to cut weight in automotive, marine, and industrial components while maintaining acceptable mechanical properties and surface quality.

- In thermoset and thermoplastic composites, hollow glass beads help reduce resin usage, shrinkage, and warpage, improving dimensional stability and machinability. When combined with fibers or other fillers, they enable hybrid formulations that balance stiffness, toughness, weight, and cost for structural and semi-structural parts.

- Building and construction applications benefit from the thermal and acoustic insulation properties of hollow glass beads, which can be incorporated into plasters, grouts, sealants, and insulating panels. This supports stricter building codes and energy-efficiency targets without significantly increasing installation complexity.

- In coatings, adhesives, and sealants, hollow glass beads are used to lower density, control viscosity, and improve sandability and texture. They enable high-build, low-sag formulations and can improve hiding power and durability when properly dispersed and surface-treated.

- Oil and gas and other industrial fluids use hollow glass beads to tailor density and rheology in drilling, completion, and insulation applications. The beads offer stability and chemical resistance under challenging conditions, supporting safer and more controlled operations in demanding environments.

- Advances in high-strength and ultra-high-strength bead technology expand use into higher-pressure processes such as injection molding and extrusion. These grades withstand processing stresses that previously limited hollow glass beads to lower-pressure or hand-layup systems, opening new opportunities in mass-production environments.

- Surface treatment and functionalization are increasingly important, with silane and other coating technologies used to enhance bonding to specific resin chemistries. Tailored interfaces help preserve mechanical properties, improve moisture resistance, and maintain long-term performance in harsh service conditions.

- Sustainability and lifecycle considerations favor hollow glass beads because they can reduce overall material consumption, lower transport-related emissions through weight savings, and improve thermal efficiency. Producers are also exploring lower-impact manufacturing and recycling strategies to align with customer sustainability goals.

- Looking ahead, continued expansion of lightweight composites, electric vehicles, advanced insulation systems, and high-performance coatings is expected to support robust demand for hollow glass beads. Suppliers that combine reliable supply, strong application engineering, and ongoing innovation in strength, functionality, and sustainability will be best positioned to capture long-term market growth.

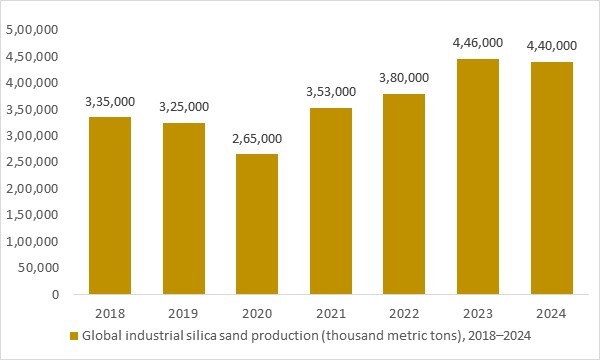

Global industrial silica sand production (thousand metric tons), 2018–2024

Figure:Global industrial silica sand production (thousand metric tons), 2018–2024 – industrial silica sand is the core feedstock for glass manufacturing and a key upstream driver for the hollow glass beads market.

- Global industrial silica sand production has expanded steadily from 2018 to 2024, reflecting stronger upstream availability of high-purity silica used in glass manufacturing. This trend supports rising hollow glass bead output, enabling their wider adoption in lightweight composites, performance coatings, plastics, and construction materials. The sustained growth in silica supply reinforces long-term market stability and underpins the scalability of hollow glass bead applications across industries.

Regional Analysis

North America Hollow Glass Beads Market

In North America, the PFA (polyfluoroalkoxy) welding film market is supported by a strong installed base of high-performance process industries, including chemical processing, semiconductor, aerospace, and advanced composites. PFA welding films are used as hot-melt adhesive layers and bondable interlayers for PTFE-coated glass fabrics, corrosion-resistant linings, high-temperature insulation, and release films in composite lay-up. Equipment builders and fabricators value PFA welding films for their combination of high continuous-use temperature, chemical inertness, weldability, and transparency, enabling reliable bonding without liquid adhesives. Growth is further supported by ongoing investment in semiconductor capacity, battery and fuel-cell plants, and aerospace composite facilities, all of which use fluoropolymer films in critical components and tooling. At the same time, tightening state-level and federal scrutiny of PFAS (“forever chemicals”) is pushing users and suppliers to improve emissions control, documentation, and end-of-life strategies, rather than immediately abandoning fluoropolymer films that are considered mission-critical.

Europe Hollow Glass Beads Market

In Europe, demand for PFA welding films is closely linked to advanced manufacturing in chemicals, pharmaceuticals, automotive, aerospace, and renewable energy equipment. PFA films are used as weldable liners, release films, and bonding media in composite structures and corrosion-resistant components operating in harsh thermal and chemical environments. European producers and converters are among the leading global suppliers of fluoropolymer films, offering extruded and welding-grade PFA films tailored for bonding PTFE fabrics, process belts, and engineered parts. However, the region is also at the forefront of PFAS regulatory initiatives, including REACH-based universal PFAS restriction proposals and specific caps on PFAS emissions, which drive investment in cleaner manufacturing technologies, traceability, and potential long-term substitution strategies. For the foreseeable future, exemptions for critical uses in semiconductors, aerospace, and other strategic sectors are expected to sustain PFA welding film demand, but under much stricter environmental performance requirements.

Asia-Pacific Hollow Glass Beads Market

Asia-Pacific is the manufacturing growth engine for PFA welding films, underpinned by rapid expansion in electronics, semiconductors, chemical processing, solar energy, and high-end industrial equipment. Major fluoropolymer producers and converters in Japan, China, and other regional hubs offer PFA films for welding, thermoforming, and bonding, supplying local and export markets with a wide range of thicknesses and widths. PFA welding films are widely used in corrosion-resistant linings, composite release films for aerospace and wind blades, and high-purity fluid handling in chip fabs and battery plants, where their thermal stability and chemical resistance are essential. Regional governments’ focus on localizing advanced materials supply chains also supports investment in fluoropolymer film capacity. At the same time, emerging PFAS regulations in countries such as Japan, along with export-market requirements, are pushing Asian producers to enhance emissions control, product stewardship, and documentation, but overall demand for PFA welding films remains on an upward trajectory.

Report Scope

| Parameter | Hollow Glass Beads Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Diagnostic Method, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Hollow Glass Beads Market Segmentation

By Product

- Microspheres

- Nanospheres

By Application

- Aerospace

- Automotive

- Construction

- Industrial Coatings

By End User

- Manufacturers

- Contractors

- Distributors

By Technology

- Traditional Manufacturing

- Advanced Manufacturing

By Distribution Channel

- Online

- Offline

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Top 15 Companies in the Hollow Glass Beads Market

- 3M Company

- Trelleborg AB

- Cospheric LLC

- PQ Corporation

- Silibeads (Sigmund Lindner GmbH)

- Nippon Electric Glass Co., Ltd.

- Kuzeyboru Company

- Potters Industries LLC

- Matsumoto Yushi-Seiyaku Co., Ltd.

- Syntactic Foam Corporation

- Chase Corporation

- CenoStar Corporation

- Mo-Sci Corporation

- Sinosteel Maanshan New Material Technology Co., Ltd.

- Xingtai Ruike Chemical Co., Ltd.

Recent Developments

- Nov 2025 – Macquarie Asset Management (consortium) / Potters Industries: A Macquarie Asset Management-led consortium agreed to acquire Potters Industries, a major producer of glass microspheres and beads. The deal signals continued strategic interest in specialty glass bead platforms tied to infrastructure and industrial end uses.

- Jan 2025 – Brenntag Specialties / 3M: Brenntag’s exclusive distribution arrangement for 3M Glass Bubbles was expanded from the UK into France and Iberia (effective from January 2025). The move is aimed at improving regional availability for coatings, plastics, and construction formulations using hollow glass microspheres.

- Dec 2024 – Brenntag Specialties / 3M: Brenntag and 3M announced the expansion of their distribution cooperation for 3M Glass Bubbles into additional European markets. The announcement reflects rising customer pull for lightweighting fillers and performance additives across industrial materials.

- October 2024 Revitri announced the development of a pilot facility to produce lightweight hollow glass beads using recycled glass feedstock, aiming to enhance sustainable materials supply.

FAQ's

The Global Hollow Glass Beads Market is estimated to generate USD 1.82 Billion in revenue in 2025.

The Global Hollow Glass Beads Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.1% during the forecast period from 2025 to 2032.

The Hollow Glass Beads Market is estimated to reach USD 2.41 Billion by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!